Crypto is LOUD.

Headlines, trials, frauds, scams, degens, lambos, WAGMI, million dollar jpegs, maxis… the last wave of crypto was brash and ‘in your face’. Every industry headline seems to come with an exclamation point next to it!

That’s a feature, not a bug.

Early days-crypto was on a mission to replace money itself and the financial system that was built upon it. To take on such a massive societal change—to get people to trust an entirely new form of money—a powerful narrative was required, the first chapter of which was written in the 2008 bitcoin whitepaper.

To spread that story, crypto needed marketing. Bitcoin was arguably one of the most successful brands in history to grow through purely organic means. Satoshi didn’t have an advertising budget (not that Google or Facebook would let him/her/them advertise anyway), but what he/she/they did have was a powerful incentive structure. Whether mining or HODLing, those who joined the crypto tribe would now have a vested monetary interest in seeing it succeed, and what better way to get people to spread a narrative than to provide a monetary incentive for them to do so.

As much as speculative excesses and frenzies can help fuel real innovation, mass adoption of those innovations often does not occur until after the frenzy has faded.

Yes, crypto is loud. But in contrast to the above, I believe the next wave of crypto adoption will be the opposite.

In fact, I think mainstream crypto adoption will be rather QUIET.

People will be ‘using’ crypto products and rails without knowing they are crypto products and rails.

There are two trends driving this belief:

- Culture Crypto: something fundamentally new for the consumer

- Institutional DeFi: leaning on price sensitive intermediaries for adoption

Let’s unpack them both.

Culture Crypto: Something Fundamentally NEW for the Consumer

“The institutions are here, just not the ones we expected”

Shout out to Colleen Sullivan at Brevan Howard for that quote which points to the driver for crypto’s next wave of adoption. The institutions she is talking about are not banks or broker-dealers or institutional investors. Although, they are all here too. She is talking about major technology and consumer brands like Nike, Starbucks, Reddit, Instagram and Shopify.

What are these institutions up to? Well, let’s skim through some examples.

Nike: The company made $185.3M last year on Web3 products after purchasing digital design studio Rtfkt and has now launched Dot Swoosh, a new Web3 platform and ecosystem where people can buy, show off and trade phygital (the most cringy buzzword out there!) and virtual products; unlock access to events; and co-create product ideas.

Starbucks: Described aptly in Fintech Brainfood as a combination of Pokemon GO and an Amex Platinum Card, Starbucks recently launched Odyssey as their next generation rewards program. Odyssey will allow users to collect both Points as well as NFTs that will open access to new benefits and exclusive experiences.

Reddit: For years, Reddit has allowed users to customize their own personal avatars. In the summer of 2022, the company launched Collectible Avatars, which were limited-edition avatars made by independent artists, in partnership with Reddit, that provide owners with unique benefits on the Reddit platform. These collectibles were minted as NFTs through the Polygon blockchain. The project has more than 4.25 million total unique wallets to date.

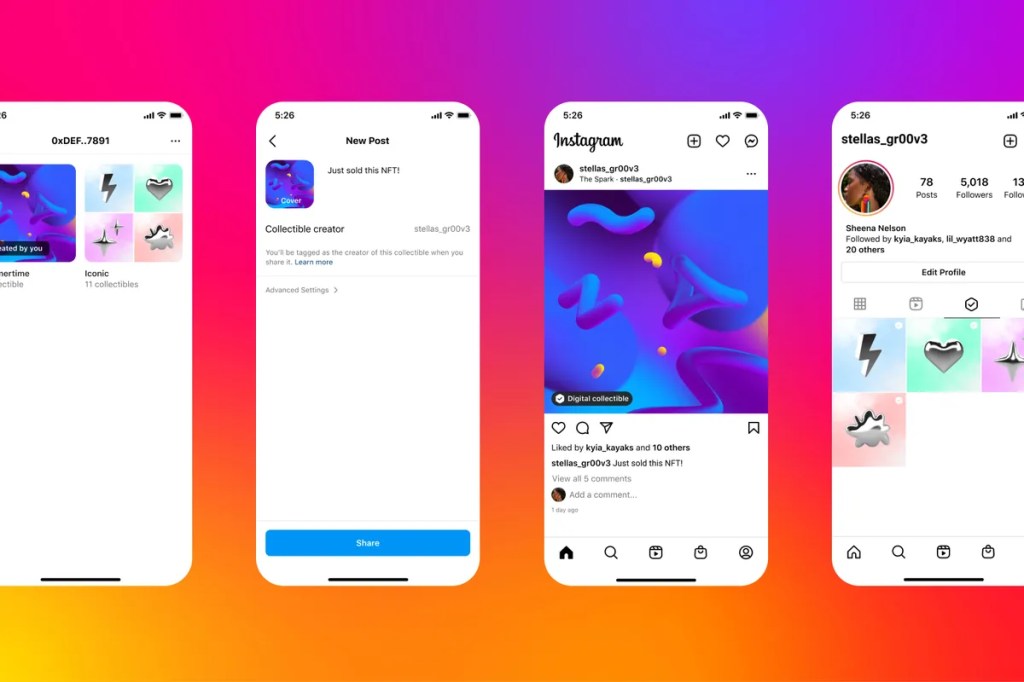

Instagram: Like Reddit, Instagram is also leveraging the Polygon blockchain to be able to allow creators to make their own digital collectibles on Instagram and sell them to fans, both on and off the platform. Users can also showcase digital collectibles more prominently, at least those held on the Ethereum, Polygon, Flow and Solana blockchains. This has become a serious business opportunity for Meta, with Deutsche Bank analysts estimating that the NFT marketplace on Instagram could drive up to $8 billion in net annual revenue.

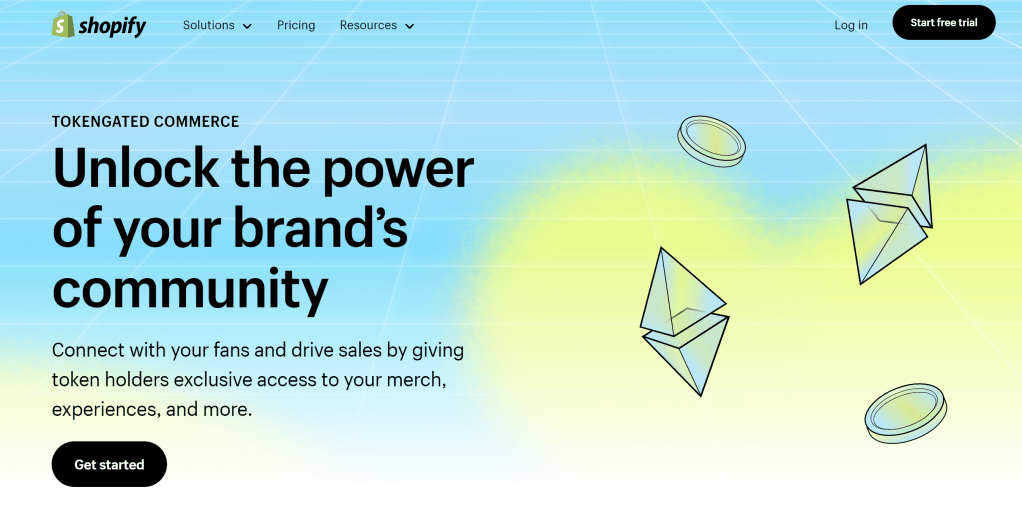

Shopify: The global ecommerce platform has added a new tool in their merchants’ toolkits: the ability to create community around their products. Through the concept of token-gated commerce, Shopify merchants are able to mint and sell NFTs with the objective of gating certain features of their online stores to create exclusive and tailored experiences for customers.

If those examples were not enough, here is a non-exhaustive list of other large consumer brands and some of their exploratory crypto initiatives (credit to Marc Baumann for pulling this together):

- Adidas https://lnkd.in/e6YAa3fv

- Balmain https://lnkd.in/eb8aSvzc

- BMW https://lnkd.in/eqa3x2Pe

- Budweiser (AB InBev) https://nft.budweiser.com/

- Burberry https://lnkd.in/ewshTs5x

- Cartier https://nftcartier.online/

- Disney https://lnkd.in/efAHFSRs

- Dolce & Gabbana https://lnkd.in/embgKiNj

- GAP https://nft.gap.com/

- Givenchy (LVMH) https://nft.givenchy.com/

- Gucci (Kering) https://lnkd.in/estudKCw

- Hello Kitty https://lnkd.in/ey44MMjF

- Hennessey (LVMH) https://lnkd.in/evFSq_zf

- Hublot (LVMH) https://lnkd.in/eAJ-DhHD

- IWC https://nft.iwc.com

- Jacob & Co. https://jacobandco.com/nft

- L’Oréal https://lnkd.in/egFnCZfD

- Lacoste https://undw3.lacoste.com/

- Lamborghini https://lnkd.in/eq2dTM_Z

- Mastercard https://lnkd.in/ezmBT4-Q

- McDonalds https://lnkd.in/eTg4c5cZ

- McLaren https://nft.mclaren.com/

- NBA https://nbatopshot.com/

- Netflix https://lnkd.in/ebNqRUga

- NFL https://nflallday.com/

- Panerai https://lnkd.in/eMxcpdgV

- Pepsi https://lnkd.in/e2gq4geM

- Porsche (VW Group) https://nft.porsche.com

- Prada https://lnkd.in/euK6iqKy

- Puma https://lnkd.in/ez7GhnyM

- Red Bull https://lnkd.in/eWM7Urkt

- Rimowa https://lnkd.in/eCQNGzm3

- Skoda (VW Group) https://lnkd.in/eFVFJRQ8

- Tag Heuer https://lnkd.in/eAv-6ZpN

- Tiffany & Co https://nft.tiffany.com

- Time Magazine https://nft.time.com/

- Timex https://lnkd.in/evFYmwxb

- Visa https://lnkd.in/epPYXn5z

- Yves Saint Laurent https://lnkd.in/e567h8eu

Let’s call most of this what it is: experimentation. But these experiments are doing something important. They are readying the infrastructure required to execute Web3 programs at scale. More importantly, they are readying consumers to accept crypto as part of the background of their everyday experiences.

- Bought a new time piece from a luxury watch maker? Make sure to hold on to the NFT you received alongside for authentication when it is time to re-sell it.

- Want to support your favorite fashion influencer (or financial blogger)? Make sure you have their token or NFT to show that you are part of their community.

- Looking for exclusive access or benefits from your favorite brands? Well those might soon be delivered in the form of a token or collectible that can open up that access.

The NFT path is slowly following one that looks similar to the evolution of Finance Crypto.

Much like the first NFT craze around profile pictures (PFPs like CryptoPunks and Bored Apes), the first iteration of Finance Crypto was also a simple collectible: Bitcoin, whose primary use case came to be ‘digital gold’.

Then came the next evolution which saw Finance Crypto start to replicate traditional financial functions after the birth of Ethereum and the excitement born around trading and digital payments. Similarly, the next rush around NFTs appears to fit with tokenizing real world assets. Starting with luxury items like watches and handbags, the ‘phygital’ (cringing again) trend seems to be invading other areas of commerce.

Finally, much like how utility has sprung forward from the DeFi ecosystem and protocols in Finance Crypto, NFTs seem to have evolved toward carrying some form of utility as well (eg. the benefits unlocked by Starbucks’ Odyssey or Shopify’s Tokengated Commerce). This final step starts to bridge the gap between crypto as a collectible, speculative item, or novelty toward something that fits into the broader economy. Tying an NFT to some form of real world utility will also likely help tamp down the speculative nature of the asset, given that the real world benefit likely has a better basis for valuation than do collectibles or non-utility bearing digital assets.

Across all of these initiatives, millions of wallets are being created and people are slowly but surely getting used to operating in the crypto environment. Do most Redditors know they have a digital wallet that holds their assets on the Polygon blockchain? Probably not, but that is the point. Consumer brand in the front, crypto in the back.

Culture Crypto’s contribution to adoption is to get wallets into the hands of millions of people without them realizing it, which would be one giant [and quiet] step forward for the ecosystem.

BONUS FACTOR: Usability Enhancements

As an aside, another key ingredient to the success of bringing crypto to the average consumer is to simplify the user experience for non-Web3 native individuals.

Managing private keys, sending assets to alphanumeric addresses, minimizing gas fees and understanding cross-chain dynamics is a lot to wrap your head around and comes with a high degree of uncertainty for first time users. That said, the crypto industry certainly understands that it has a usability problem, which is currently being tackled at all levels from the protocols themselves to the apps built on top.

Multi-party computation (MPC) and account abstraction (AA) are two fundamental advances that will help alleviate some of the prohibitive demands placed on those opting for self custody (see this great explainer from Ria Bhutoria). There are direct to consumer companies like The Easy Company raising money (in a very tough capital markets environment) to build out the ‘consumer layer’ of Web3 through a digital wallet UX that is simple to navigate for non-technical customers. Companies like Conduit are working on improving crypto ramps (the way users get into and out of DeFi) making them easier, faster, cheaper, hidden, and embedded in other experiences.

If the crypto ecosystem is successful in improving usability for its non-technical users, it will come from abstracting away the complexity of interacting with crypto infrastructure and hiding the technical complexity behind familiar user interfaces.

Institutional DeFi: Leaning on Price Sensitive Intermediaries for Adoption

Speaking of technical complexity that is hidden behind familiar user interfaces, that is also how the traditional financial system is structured today. The challenge with the existing system is that it was built at a time when paper-based analog architectures were still the dominant form factor, only now they have a digital layer sitting overtop. To be certain, our financial system’s infrastructure is in serious need of some TLC and innovation.

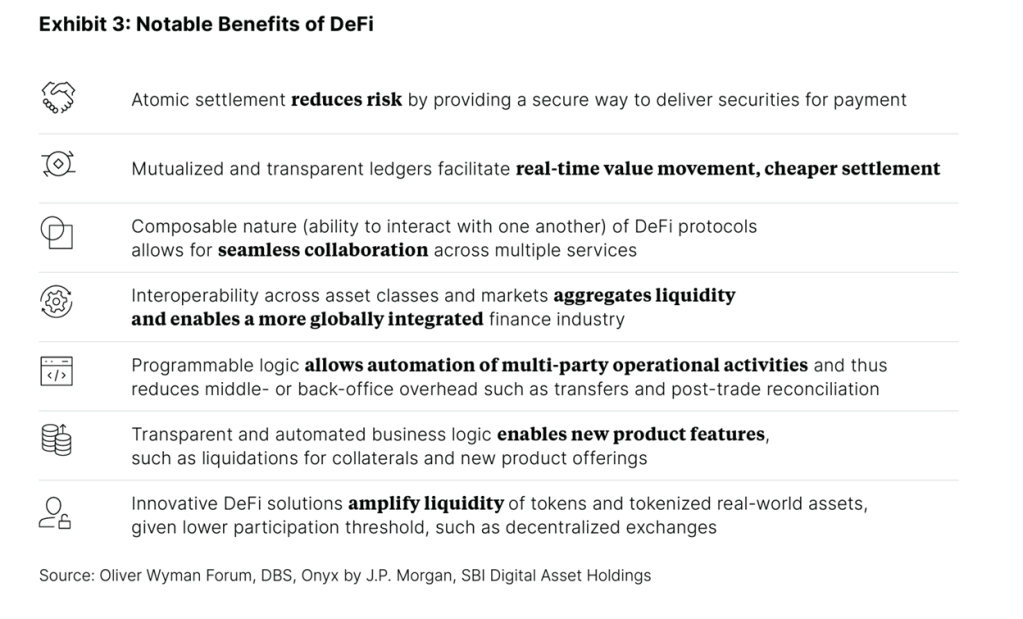

DeFi has always appeared to be a perfect sandbox for financial infrastructure innovation. ‘Money legos’ as they are known, are individual composable primitives that now extend across almost every vertical of the financial services industry: exchange venues, payment rails (stablecoins), derivatives, lending, insurance, asset management… it’s all there. Outside of the value proposition innovation that has produced some never before seen financial products (eg. flash loans, perps, overcollateralized stablecoins, etc.), cost and efficiency is the general throughline that creates some incredible value for DeFi users. Fees tend to be low, or non-existent, and transaction execution and settlement typically takes place in seconds. While it still has a long way to go to reach ‘maturity’, the infrastructure that has been developed in the DeFi world has now become too attractive for traditional financial institutions to ignore.

What is beginning to take place is experimentation by large established financial institutions to determine ways to incorporate DeFi primitives into traditional financial infrastructure. The stand out example of this was a recent exploratory project (Project Guardian) put on by the Monetary Authority of Singapore along with DBS, J.P. Morgan, and SBI Digital Asset Holdings. The four organizations carried out a pilot program that involved two use cases: transactions involving foreign exchange with tokenized deposits and separate transactions involving government bonds. In each case, the transactions were executed on a public blockchain network (Polygon), using digital identity solutions (W3C Verifiable Credentials) and logic adapted from existing DeFi protocols (Aave).

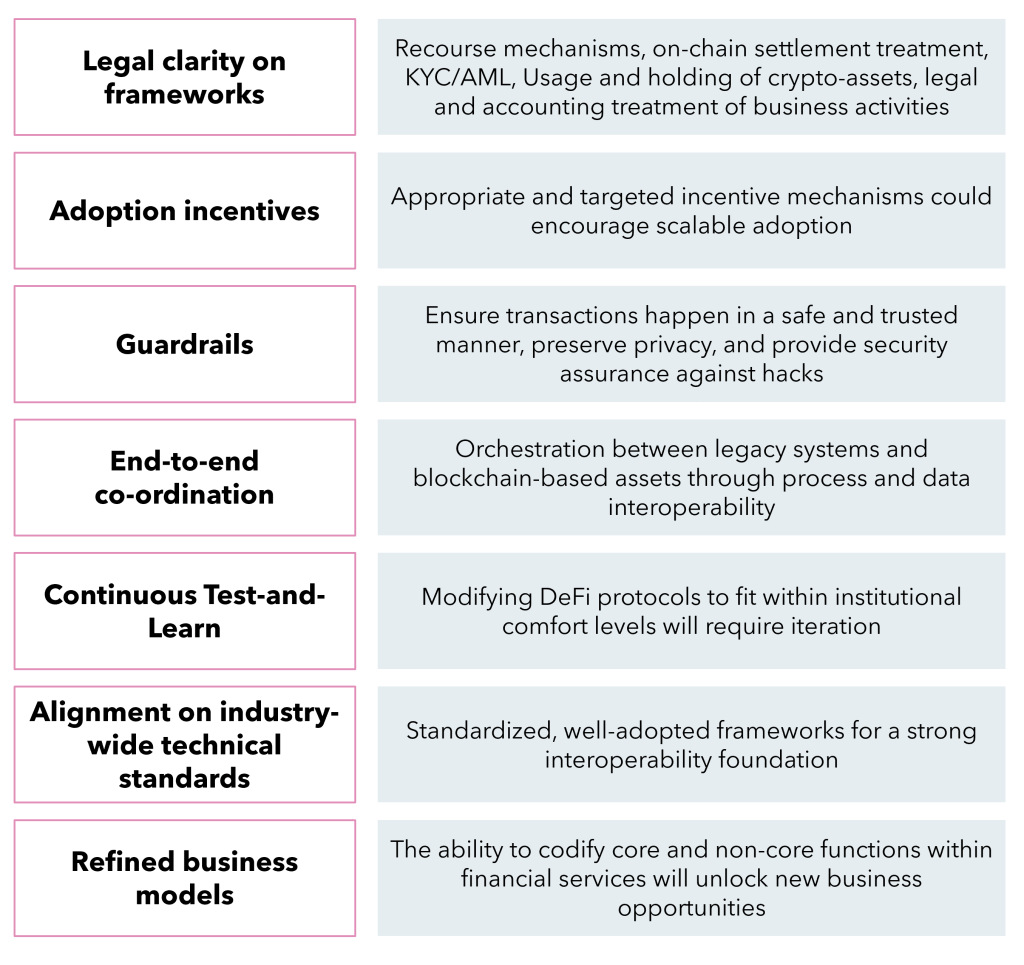

This was no small feat. The fact that some of the world’s largest financial institutions were playing around in the DeFi innovation sandbox and proved that a workable arrangement was possible is major validation for the DeFi community. The organizations also acknowledged that there is a long road ahead for this type of pilot program to be put into production. Advancements around AML/KYC risk controls, data privacy, cybersecurity, governance and conduct models, recourse mechanisms, as well as additional legal clarity around smart contract-based business activity will all be required to turn DeFi dreams into reality.

The MAS also shared their learnings from the project in a 50+ page whitepaper (link here). They are summarized below:

The paper also highlighted some key areas of potential for Institutional DeFi. Those included: commercial/investment banks, exchanges, brokers, dealers, centralized clearing entities, custodians, technology vendors, and data providers.

The applicability of Institutional DeFi is broad. As noted, there is now a well-functioning DeFi primitive (money lego) for most of the major existing financial services out there (with some notable exceptions, like unsecured lending). It is not out of the realm of possibilities that piece by piece, the existing financial rails begin to migrate over to their more efficient crypto counterparts. Of course, this will only make sense in certain cases, but should crypto infrastructure (public blockchains in particular) start to become more integrated into the existing financial system, more and more people will be using a blockchain-secured service without ever knowing it.

In this case, it will be traditional financial brand in the front, crypto in the back.

Crypto Inception

In the last Paper & Blocks post, The Comfort Factor: Why Cost Leadership is a Not a Viable Strategy in Retail Financial Services, the conclusion was that consumers will not switch financial service providers simply for a low-cost value proposition, but they will make the switch for differentiation. That is what NFTs and ‘culture crypto’ provide: something new for the consumer that does not require any switching at all because there is nothing there to switch from.

On the other side of the ledger, the piece also concluded that unlike consumers, institutions and intermediaries will jump at the chance to leverage a more efficient system if it means being able to position that efficiency as a low-cost benefit to their end customers. That is what Institutional DeFi provides: adoption of new technology simply because it is better infrastructure.

Of course, the louder side of crypto will continue to grow as well. Centralized exchanges, consumer DeFi, PFP communities, and the rest of the ecosystem will likely move through their boom-and-bust cycles right on queue.

But what is important to consider is these more subtle elements (culture crypto and institutional defi) are both net new from prior cycles and they differ substantially from the speculative excesses that came before.

They put the ‘crypto’ element further in the background: consumer or financial brand in the front, crypto in the back.

They don’t flex on the web3/NFT terminology.

They don’t encourage speculative frenzies.

Instead, utility will be put front and center.

This type of adoption is quiet… but it is incredibly powerful.

It is adoption by inception.

2 responses to “Crypto Inception: A Theory of Mainstream Adoption from NFTs to Institutional DeFi”

[…] In 2023, Bernard Arnault, founder of luxury powerhouse LVMH became the richest man in the world with a net worth of $211 billion. His empire of luxury goods was built, in-part, on the premise that people are willing to pay a premium for certain products that signal to the world something about them. Namely, that they are wealthy and have a certain ‘status’. But people do more than just signal their desired perceived traits through their economic activity. They may also signal things like who they aspire to be (a child wearing their favorite player’s baseball jersey) or what communities or groups they are affiliated with (driving a Prius or bearing a cross on a necklace). As is also the case with collectibles, thanks to the unique one-of-ones that can now be created online, digital goods have also become signaling items. People can purchase an NBA Top Shot NFT to rep their favorite team or support their favorite player; they can acquire a creator NFT to show their appreciation for their art; or they can even trade for a PFP to gain exclusive access to a new community of people brought together by their shared interest in the project. Even a wallet full of fungible Dogecoin says something about you that you might (or might not) want to flaunt. Social signaling is now a core use case for crypto and it will continue to grow as big brands like LVMH who make their living off of signaling in the real world realize there is opportunity to do so in the digital realm as well. “The institutions are here, just not the ones we expected”. […]

LikeLike

[…] In 2023, Bernard Arnault, founder of luxury powerhouse LVMH became the richest man in the world with a net worth of $211 billion. His empire of luxury goods was built, in-part, on the premise that people are willing to pay a premium for certain products that signal to the world something about them. Namely, that they are wealthy and have a certain ‘status’. But people do more than just signal their desired perceived traits through their economic activity. They may also signal things like who they aspire to be (a child wearing their favorite player’s baseball jersey) or what communities or groups they are affiliated with (driving a Prius or bearing a cross on a necklace). As is also the case with collectibles, thanks to the unique one-of-ones that can now be created online, digital goods have also become signaling items. People can purchase an NBA Top Shot NFT to rep their favorite team or support their favorite player; they can acquire a creator NFT to show their appreciation for their art; or they can even trade for a PFP to gain exclusive access to a new community of people brought together by their shared interest in the project. Even a wallet full of fungible Dogecoin says something about you that you might (or might not) want to flaunt. Social signaling is now a core use case for crypto and it will continue to grow as big brands like LVMH who make their living off of signaling in the real world realize there is opportunity to do so in the digital realm as well. “The institutions are here, just not the ones we expected”. […]

LikeLike