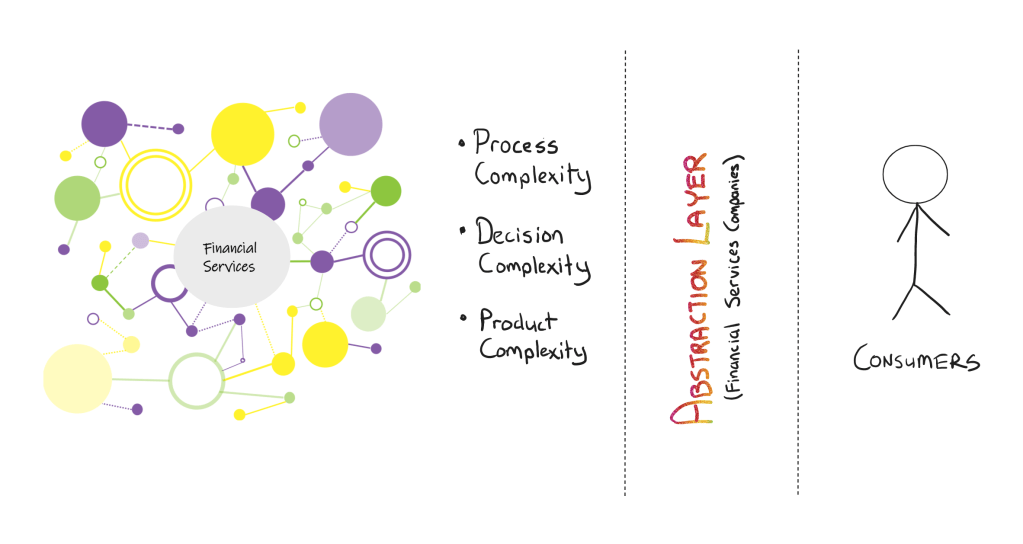

Most consumer-facing financial services firms (from banks to wealth management companies to insurance agents) perform the same service for their clientele. They compete primarily on this service day-after-day, it is heavily embedded in their corporate strategy decks and product roadmaps, and it sits quietly as the primary activity for frontline staff (tellers, financial advisors, and insurance agents). This service is not a product, it is not a transaction-type, and it is not advice: it is all of the above. Most financial services firms today are the consumer-facing abstraction layer that removes all the complexity of interacting with the financial system and turns it into a simple set of products and services.

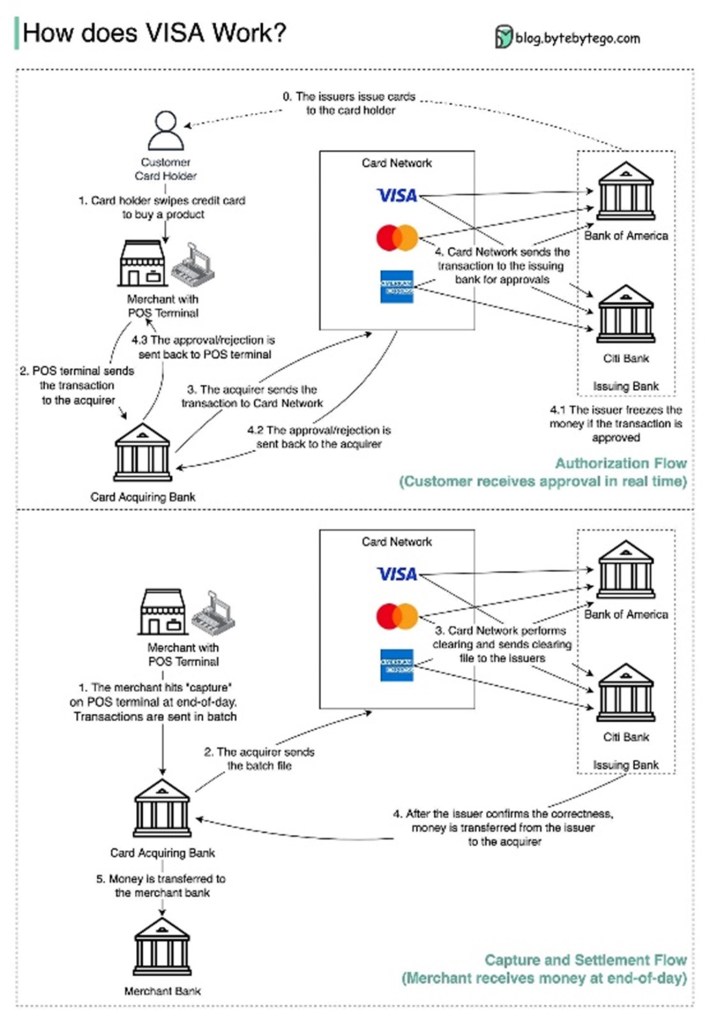

The modern financial system is insanely complicated, much more than most people know. That is because the companies of today have done rather well at hiding that complexity. But, if you take the simple [and overused] example of buying a coffee at the local Starbucks with your credit card, there is a mountain of processes and parties involved in first authorizing and approving the transaction, then settling the funds.

All of this complexity is to simply get funds from your bank account into the merchant’s bank account, and on the surface, this complexity is hidden from view, making your Starbucks purchase experience quick and delightful.

The card issuer, in this case, is the interface for the consumer that abstracts away the complexity of interacting with the system, which involves dealing with acquirers, card networks, technology (POS terminal) providers, and the merchant’s bank. They provide a valuable service to their customers, not only in the function of facilitating their transaction, but in being the trusted party that removes complexity from their lives.

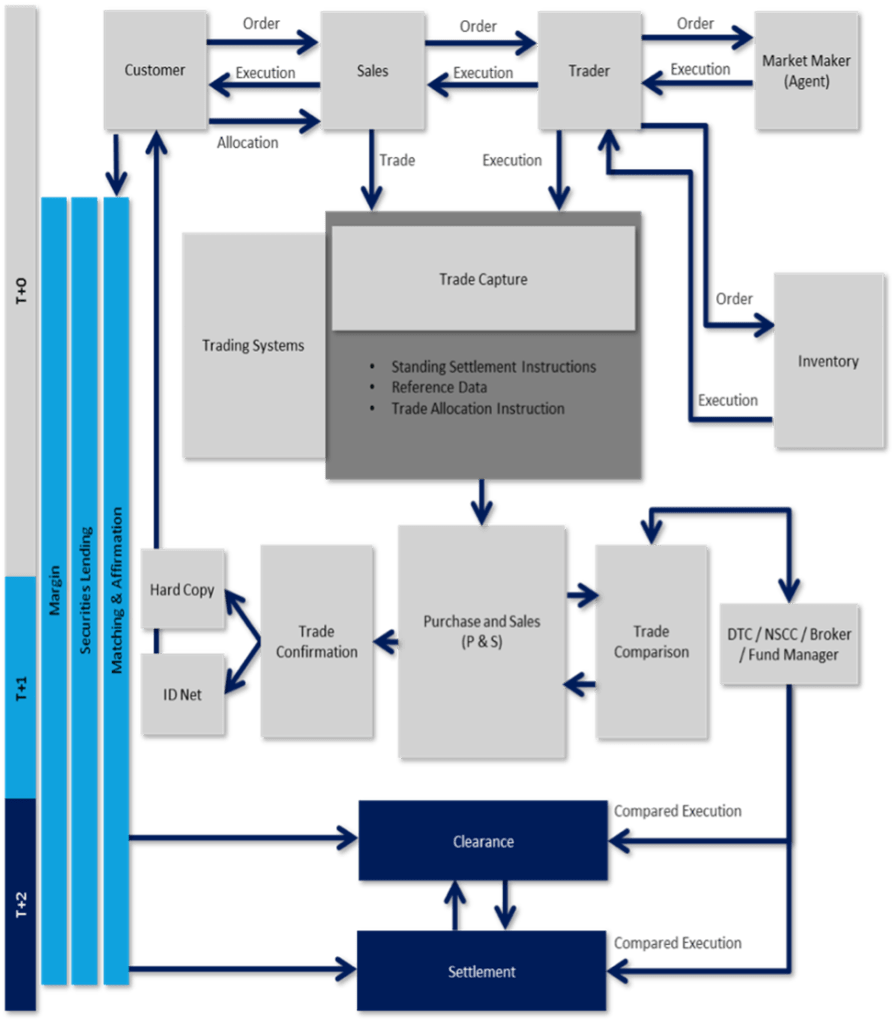

If the credit card example did not convince you of the web of interconnected providers that exist, here is a fun one to show you the complexity that sits behind facilitating and settling a securities transaction.

What do you mean by Abstraction?

When referring to the idea of abstracting away the complexity of interacting with the financial system, I’m referring to hiding all of these processes and parties from the consumer. When you’re on Robinhood, buying a stock is like hitting the ‘Easy’ button. Click, and it works! None of that messiness shown in the diagram above to hold you back.

By definition, an abstraction is just a general concept or idea, rather than something concrete or specific. In computer science, abstraction has a similar definition. It is a simplified version of something technical, such as a function or an object in a program. The goal of “abstracting” data is to reduce complexity by removing unnecessary information.

In financial services, there are three types of abstractions:

- Reducing process complexity: hiding the messy (and often archaic) systems that support the facilitation, clearing and settlement of most financial transactions today. This was the point made in the two examples above.

- Reducing decision complexity: reducing or hiding the complexity of overwhelming choice. For example, there are 5,000+ individual mutual funds in Canada and tens of thousands of individual fund codes. For the average consumer to construct a portfolio with the best products for their situation, some of the complexity has to be abstracted away. In cases with heterogenous product characteristics or where personalization is required, it is often advice that helps reduce complexity. In cases with homogenous product characteristics, this is typically done by simplifying the shelf and reducing the number of options available.

- Reducing product complexity: reducing or avoiding information asymmetry. This comes down to the ability for the consumer to comprehend the impact a product will have on their intended outcomes. With a mortgage, a simple example is the industry staple: a 5-year fixed-rate mortgage. The term is five years, the payments are the same dollar amount and at the same interval over those five years, and the principal will be reduced by a known amount over that period. It is easy to comprehend. A 5-year variable rate mortgage with fixed payments gets a little bit more difficult. Here, the term will be consistent, the principal reduction will fluctuate, and the payments will be the same. Even more complex is the standard open 5-year variable rate mortgage where the term is consistent, the principal reduction fluctuates AND the payments fluctuate. The impact on the outcome becomes harder to know with any certainty. Multiply these choices by adding in other variables like conventional vs insured, amortization length, etc. and the outcome predictability starts to become overwhelming. As a result, product complexity and the ability to understand how it will impact consumer outcomes creates opportunities for abstraction.

In more practical terms, this means to compete or create more effective financial products, a financial institution could:

- Ensure process complexity is buried in the background and experiences move as seamlessly as possible (keep this in mind the next time your loan application takes 5 days to approve and another 5 days to process and another 5 days to fund)

- Ensure decision complexity is easily navigated. Sometimes this is a simple reminder not to overwhelm with choice (please don’t serve me up a list of 5,000 mutual funds to choose from, I’m much more likely to select a default option in this case), and other times this is ensuring the right point-of-decision advice is made available to the client.

- Ensure product complexity does not have a steep learning curve to get to the best outcome: Make it easy for a consumer to understand how a product can solve their job-to-be-done, because if done well, it is much easier to select and hire.

So it is starting to become clear that abstracting complexity is a major value creator for financial services firms today, and when abstraction is done well, it can be an important competitive lever. But the opposite can also be true. Bad abstractions can create more issues than they solve, even with the best of intentions.

Bad Abstractions

Complexity in a product or service is not necessarily a bad thing. It typically means a company is stretching to create a more advanced service to meet a customer need or expanding to create a more specific solution for a niche segment. This is typically how progress takes place: complexity precedes simplicity.

But in a mature industry where most of the financial services functions/products have been commoditized, stretching the product/feature set and expanding the target audience can hold back a product from reaching its expected potential. Two examples of where this can happen: innovation efforts and the addition of new features over time.

Innovation: Innovation is much needed in the financial services world. But as previously mentioned, when an industry has reached maturity and its products/services have become commoditized, innovation requires some outside the box thinking. The challenge in financial services is that it is a highly regulated space with low customer turnover: both ingredients for keeping innovation at bay. For innovative products/services that are trialed, added complexity is typically the path.

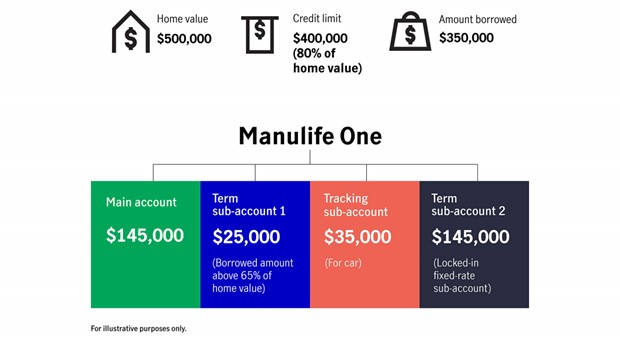

We referred above to the burden of comprehending a 5-year fixed mortgage vs a 5-year variable mortgage. Now, as another example, try to wrap your head around this mortgage product from Manulife. Manulife One is an all-in-one mortgage that combines a mortgage with deposits and other debt products to help you save on interest costs. It is certainly innovative and benefits the right customer in the right situation… but wow is it hard to understand what those benefits are and in which situations they apply.

This is an example of innovation coming at the expense of simplicity. Even though there are themes of simplicity ringing through the all-in-one aspect—and for the consumer that knows how to navigate the terms Manulife One is very beneficial—there is challenges in both communicating that value and getting the product to the people that could best use it. [To be fair, Manulife One is no longer the new kid on the block and has been around for many years and has started to abstract some complexity over that time].

Time warping: Time warping refers to the idea that given a core product, the addition of new features over time will layer on more and more complexity rather than reduce it. Companies don’t want to sit still, they want to make changes, compete and innovate. So they start with a successful product, and then they layer on more and more features and versions over time, until it becomes difficult or overwhelming to understand. Addition is viewed as progress, and people are typically rewarded for addition, not necessarily for subtraction. That does not abstract away complexity, it adds it.

For example, let’s look at what you can get if you take the latest offer to open a chequing account at Scotiabank.

First, let’s applaud Scotiabank for offering so much value to their customers. There is a lot to take advantage of in here. But it is a good example of adding complexity at the expense of getting the right product to the right customer. There are discounts for every service under the sun, some that are likely to be used (everyone has a credit card, right), and some that likely never will (I don’t know many heavy safety deposit box users). As a consumer, the question to ask is: do I understand the benefit I’m getting in signing up for the account and will this get me closer to the outcome I’m looking for, or does this overwhelm me with sticker value that appears good on the surface, but are things that I won’t actually need or use. This also makes comparing this service to others in the market extremely difficult, a benefit to the company and not the customer.

Seth Godin puts this well when talking about feature creep:

• Adding another feature is cheap compared to the benefits it offers to new users or existing ones.

• Once a feature is added, it is almost never removed.

• When enough features are added, the system breaks down and fails.

This isn’t just software [or banking]. It’s the menu at the diner. It’s the buttons on the dashboard of a car. It’s the variety of choices parents are offered of which dates summer camp starts or ends. Anything where a lot of hard work can be slightly improved simply by adding an innocuous option. At one point, Yahoo had 183 links on their home page. Google, which had two, ultimately grabbed all of their search traffic.

The Abstraction Opportunity for Traditional Financial Services Firms

There are clear examples of good abstraction and bad abstraction in the industry today, but how can this be turned into a competitive lever? It can be done by asking a simple question in product development:

Where is there financial complexity in people’s lives and how can we help abstract that away?

Where is the messiness of the financial system’s processes overexposed to the consumer? Where is there friction between the decision/product and the intended outcome? Each of these can form a check on developing and launching new features, products and services.

Simplicity can be a competitive advantage if it enhances the comprehensibility of the value a firm provides. A few more helpful principles to keep in mind when thinking through customer-facing decisions:

- Simple consists only of what’s necessary for users and the business to meet their needs.

- Simple is designed to feel familiar and intuitive to users.

- Simple offers users the shortest and easiest route to meet their needs.

Outside the credit card example off the top, a couple other examples of doing this well are Plaid and Wealthsimple.

Plaid (or most API-first fintech companies): API-first businesses like Twilio or Stripe, as Packy McCormick puts it, essentially abstract away the complexity of a whole best-in-class company, giving clients the full output of a highly-focused org… When a company chooses to plug in a third-party API, it’s essentially deciding to hire that entire company to handle a whole function within its business. Imagine copying in some code and getting the Collison brothers to run your Finance team.

API-first companies have emerged all over the financial ecosystem to help build the data infrastructure layer of the industry. This is another very good example of hiding a large amount of process complexity from both consumers and the companies using the APIs. Plaid, probably the most well-known, abstracts away the complexity of accessing [permissioned] consumer financial transaction data (and of course, has extended the business well beyond just transaction data). The same can be said for payroll data API-first companies like Argyle and Finch, or credit data API companies like BloomCredit, or insurance data API companies like Canopy Connect.

Wealthsimple: Inherent in their name, one of the first things you come across on the company’s homepage is “Investing made simple. No paperwork, no account minimums, no trust fund required”. Each product is intuitive, each customer touchpoint is purposeful, and product decisions appear to be made with intentionality around keeping customer outcomes front and center. That is abstraction at its best, when it is built into the ethos of the company itself.

The Abstraction Opportunity in Crypto

Complexity is generally not a barrier for the early adopter of any product or technology. They are motivated more by chasing the novelty or status of the ‘new thing’. To those who fall into this camp, complexity does not seem like a problem. In fact, it can be part of the fun of trying something new or can add to the status game by keeping others out.

For crypto early adopters, complexity does not seem like a problem. But for the next wave of users, the lack of an abstraction layer becomes a major barrier to adoption.

Yes, Coinbase has simplified entry-level purchase and storage. FTX has an amazing platform for those who are looking for a more advanced experience. Metamask has made major advancements on the Ethereum wallet-front, a torch that Rainbow now looks to carry. ‘Removal of complexity’ is certainly gaining some momentum in crypto.

But is it as easy as interacting with the banking system today? For the average consumer, the answer is likely to be no. Adding a browser extension, writing down seed phrases, buying a ENS domain, and going through the KYC process of an exchange to purchase some ETH is a complicated process, especially to simply start interacting with crypto for the first time.

The opportunity for abstraction is the same as it is in the traditional financial services world:

Where is there financial complexity in people’s lives and how can we help abstract that away? In the case of crypto, the most ground to be gained is likely around reducing the amount of ‘process complexity’ present in the system today.

A couple firms that are doing this well:

Abra: Abra is a financial services and technology company that operates an all-in-one, custodial cryptocurrency wallet and exchange. They have recently taken that a step further by launching Abra Bank, a U.S. state-chartered institution and, potentially, the first fully regulated depository institution for cryptocurrency in the United States. Their mission, as interpreted by me, is to abstract away the process complexity inherent in crypto wallets to make interacting with cryptoassets as seamless of an experience as buying a Starbucks coffee with a credit card. People have already developed familiarity and habitual behavior in how they interact with the traditional financial system. Why not bring that familiarity into a crypto experience. There is an opportunity to own the process abstraction layer in crypto. It is still up for grabs and will be heavily competed over in the years ahead.

Limit Break: Limit Break is [at the time of writing] still in stealth mode according to their website. But, after raising $200 million to build web3-native multiplayer online games, some of their ideas have been made public. One that abstracts away the decision complexity of getting started in crypto is the company’s ‘free-to-own’ approach (an evolution of the free-to-play business model that now dominates the gaming industry), which will give users in-game NFTs for free rather than using them as an opportunity to raise money in a sale. This simplifies the choice to interact with the web3 ecosystem [there is no cost] and it also flips on its head the typical first experience someone has trying to buy their first NFT: setting up a wallet, finding an exchange to buy some ETH or SOL, sending those funds to their wallet, then using those funds to buy an NFT on another platform. Here, the complexity is gone since the user starts with a free NFT: set-up a wallet, receive the NFT, done!

Never Stop Abstracting

You might be sick of hearing that word by now (a-b-s-t-r-a-c-t-i-o-n has been typed out 30+ times in this piece), but the power in reducing complexity is a significant opportunity in financial services. It can also work against a firm [and their customers] if it is not deliberately considered as part of product development and/or experience management. So the final word on this is: never stop abstracting… or at least, make sure you stay away from producing a bad abstraction.

One response to “Abstracting Away Complexity: The Underappreciated Service in Financial Services”

[…] ecosystem is successful in improving usability for its non-technical users, it will come from abstracting away the complexity of interacting with crypto infrastructure and hiding the technical complexity behind familiar user […]

LikeLike