For years, fintech has pushed the narrative that the existing financial stack is inefficient, built for an analog paper-based age with entrenched business models that have significant room to modernize.

An assumed by-product of this inefficiency was increased costs for financial services customers. The higher the layers of people, intermediaries and batch processes were stacked, the greater the share of consumer surplus that was captured by the industry.

This narrative extended across almost every vertical and was an investable theme for most venture firms putting capital to work in fintech:

Online Lending—The thesis here was simple: online origination has much lower costs than branch-based origination. The savings can be passed on to customers in the form of lower rates. Companies like Lending Club, for example, claimed that they “operated fully online with no branch infrastructure, and use technology to lower cost and deliver an amazing experience. We pass the cost savings to borrowers in the form of lower rates.”

Neobanks—In addition to the elimination of pesky transaction fees, Neobanks purported to offer their customers higher interest rates on their savings deposits. They were able to share more NIM with the customer because they had eliminated certain costly elements of the traditional banking stack (specifically, the bank branch network). EQ Bank, for example, states this plainly in their marketing materials: At EQ Bank, no branches = more savings.

Robo-advisors—Building a simply constructed index-based portfolio and removing a key distribution intermediary (a financial advisor) from the value chain allowed early robo-advice firms to flex as a more efficient and lower-cost alternative to traditional financial advice.

DeFi—In crypto, most of the on-chain world exists to eliminate intermediaries (or insert new automated versions). Decentralized Exchanges (DEXs), for example, create a lot of value with very few resources. While occasionally exceeding Coinbase’s daily trading volume for certain asset pairs, Uniswap (a leading DEX) manages to do so with a headcount of under 100 employees. Contrast that with the ~4,000+ that work at Coinbase or the tens of thousands that keep the lights on across the traditional equity trading infrastructure.

In general, taking costs out of the stack has provided a win for the customers of these businesses in the form of lower prices, higher returns and/or more streamlined services. However, most have yet to become the dominant business model in their respective fields. Why is that?

A Broken Flywheel

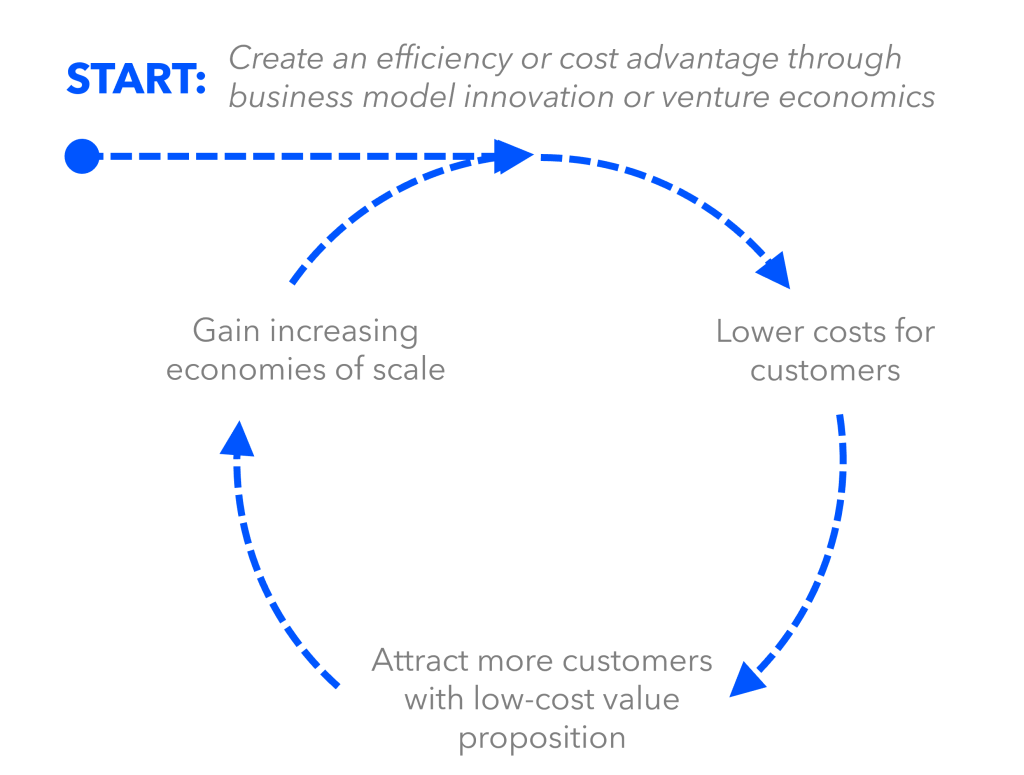

Pursuing a cost-leader strategy is typically reserved for companies with economies of scale where the marginal cost per unit of production falls as the level of output increases.

This was likely the end game for many of the fintech scenarios above. To get there, however, required a cost-efficiency flywheel to take hold.

A company could start out with some sort of cost or efficiency advantage that came about as the result of business model innovation (eg. lending direct-to-consumer without a branch network) or that could be supported through venture capital. That initial advantage could snowball if the company was able to lower the cost of its product relative to its closest competitors and attract new customers with their low-cost value proposition. The more customers attracted, the more economies of scale takes hold which gives the company room to continue to lower costs for customers even further. Hence, the flywheel effect.

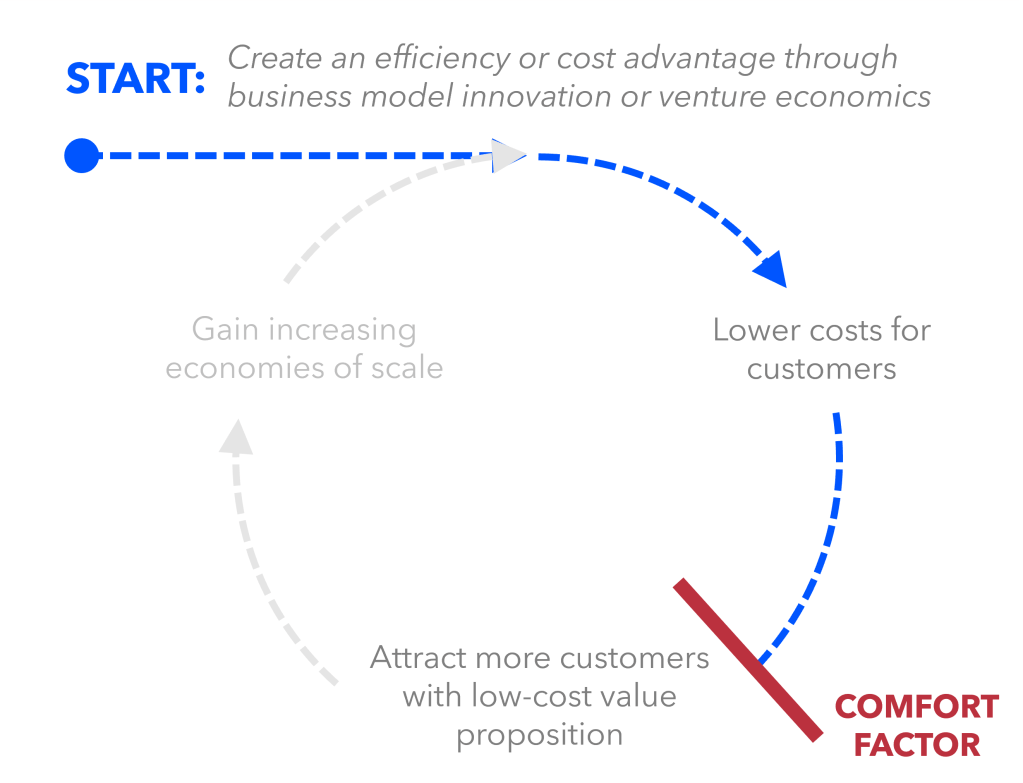

In most financial services, however, there is one key area where this flywheel effect breaks down and it is due to something we can call the “comfort factor”.

The Comfort Factor

The comfort factor is another word for the powerful force of ‘inertia’ that holds the status quo in financial services. It has three primary components:

1/ Switching costs: The wall of switching costs in front of customers is quite high in the industry. Money, time, energy, and emotional costs all stack on top of each other to create a tall hurdle for customer acquisition efforts to clear. Pair that with a degree of uncertainty about the outcome produced by the product being switched to and you have a recipe for inertia.

2/ Brand affinity: Like it or not, brands are more than transactional entities to us. In fact, we develop relationships with brands much like we do with friends. Research has also shown that we tend to see our friends as extensions of our own personal identities, which is why we root for them to succeed. So when we develop a similar type of relationship with a brand, we root for its success. Similarly, attachment to a brand can also categorize us into tribes that wrap around the brand itself. The human need for belonging drives our tribal instincts… and once you become part of a tribe, you typically do not want to leave. Both of these factors combine to create a psychological recipe for inertia.

3/ Pricing opacity: Financial services verticals have varying relationships with price sensitivity. When it comes to transactional products like mortgages or fixed-term deposits, price is almost all that matters. But when it comes to relationship-based products, price sensitivity tends to be quite low. Case and point, in Canada in 2017, new disclosure-focused regulations called the Client Relationship Model II (CRM2) took effect to, among other things, make the price people were paying for financial advice more transparent. The industry exhibited a degree of worry for most of the pre-implementation period that clearer pricing would mean some friction among consumers who would fail to realize they were paying their advisor $1,000 to manage their $100k portfolio. But when the curtain was lifted and the disclosures rolled out, not much happened. People already generally knew about the prices they were paying or chose to view it as the normal cost of doing business. With few people changing financial advisors (or banks for that matter) strictly because of price, it adds to the inertia present in the industry.

Outside of the three factors above, there’s also the general feeling of: if it ain’t broke, why fix it? The functions that deposit, lending, investment and insurance products serve has not changed for decades—only the customer experiences around them have. If those experiences tend to be “good enough”, then there is little reason to make a switch.

(Of course, “good enough” is not something that we should be aiming for as an industry – but I’ll save that rant for another day).

In short, people are comfortable with their current providers and this “comfort factor” acts as a built-in braking system for the industry’s cost-efficiency flywheel. It prevents customers from being overly cost-sensitive and thereby prevents companies from successfully attracting new customers with a low-cost value proposition.

But What About Vanguard (or Other Low-cost Leaders)?

Of course, there are counterpoints to make here. The most likely one being: what about Vanguard, or other firms like it, that have succeeded largely through a cost leadership position.

Index investing took off over the past two decades with Vanguard leading much of the charge. Looking at the chart below, it appears index funds have been eating the lunch of their actively managed counterparts.

In the case of Vanguard and the index providers though, the low-cost value proposition is not working as well on consumers as it is on their financial advisors. The slow steady switch into passive products has taken hold as advisors have shifted their general value proposition from investment fund manager selectors (ie. mutual fund distributors) to becoming portfolio builders themselves. As more advisors have taken it upon themselves to construct client portfolios from scratch, low-cost index products have tended to be their building blocks. In the process, this gave advisors a strong selling point: bring your actively managed mutual fund assets over to me and I’ll save you ‘50+’ basis points on MERs by moving you into a ‘personalized portfolio’. Of course, many of these folks were also RIAs and fiduciaries, so creating the best portfolio for the best price was also a part of acting in the client’s best interest.

When it comes to Vanguard, the price sensitivity that led to their success came mostly from the intermediary, not the consumer.

The Customer Base is an Asset and a Position of Power

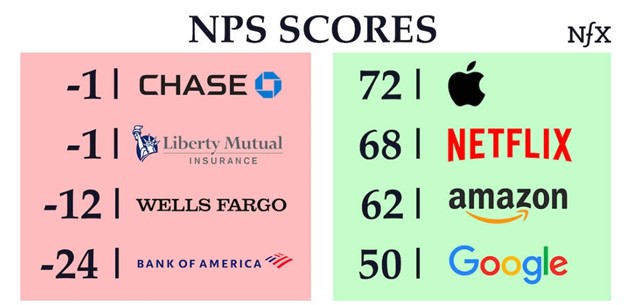

One more fact to keep in mind: Banks tend to have low NPS scores relative to other industries.

People still don’t switch.

It’s that pesky comfort factor. On top of producing industry inertia, the comfort factor also produces some interesting dynamics. The most important of which is that it elevates the value of existing customer relationships.

In fact, while hard to quantify on a balance sheet, I’d argue that the existing customer base is the most valuable asset financial services companies hold. It also gives them a strategic position with economic power.

In his book 7 Powers, Hamilton Helmer defines ‘power’ in business as a benefit plus a barrier. That is, the company is able to create something ‘better’ than what is currently offered and has some way of protecting that benefit from the spectre of competition.

When it comes to the value of a customer base, that ‘power’ exists on a continuum. On one side, there are transactional businesses where the customer must be re-acquired each transaction (eg. clothing and apparel). The value of the existing customer base here is relatively low since the business has to start higher up the marketing funnel before each interaction.

On the other side, there are relationship-based businesses where there is some sort of ongoing interaction model with the customer (eg. family doctors). Existing customer bases are extremely valuable assets in these types of industries, where average customer lifetimes are high and customer churn rates are low.

Most industries and businesses fall somewhere in between. The competitive financial services categories (banking, wealth management) tend to fall more on the relationship-based side. As a result, in those domains, the existing customer base is an incredibly valuable asset.

Two Generic Strategies, One Path to Progress

So, if the comfort factor blocks the efficiency feedback loop from turning, and customer bases are relatively static, then what strategy will work for firms looking to breakthrough in the industry.

Back to Strategy 101, Michael Porter defined his three generic strategies around two competitive advantages: low cost or differentiation.

Those two choices give you the answer… to get ahead, you must DIFFERENTIATE. You must do something different.

But what qualifies as different? Differentiation in financial services is not easy. As mentioned already, the function and form factor of most financial services has not changed for many years. Look at the market and you’ll likely see a lot of strategic beta out there. While there are multiple thought pieces that could come out of this topic alone, we’ll save them for another day (or read Strategic Alpha, Strategic Beta: Winning by Escaping the Obvious for more).

Don’t Solve the Wrong Problem

The conclusion here is that cost-leadership is NOT necessarily a great strategy for relationship-based retail financial services thanks to the ‘comfort factor’ and the inertia it produces. While likely value-creating for the customer, cost/efficiency benefits may not be enough of a hook to generate the activation energy needed to switch providers.

I hate to pick on individual articles, but there was a piece published in Venture Beat last week that crowned stablecoins as the future of ecommerce payments.

In a not-too-distant future, stablecoins can become the primary means for both online and in-person transactions… With digital assets, users seamlessly connect their wallets to their browsers and can pay instantly with the available funds. Integrating digital asset payment options will make purchases a seamless extension of the online shopping experience.

I don’t know about you, but my online shopping experiences are pretty seamless already today. Is the marginal improvement that stablecoins might provide one day enough of a benefit to overcome the comfort factor that surround today’s online payment options (namely, credit cards and digital wallets)?

Efficiency can help, but often, it is not adequate on its own.

If cost is not a material customer problem to begin with, then perhaps putting effort/time/resources into a low-cost approach is solving the wrong problem.

One response to “The Comfort Factor: Why Cost Leadership is a Not a Practical Strategy in Retail Financial Services”

[…] the last Paper & Blocks post, The Comfort Factor: Why Cost Leadership is a Not a Viable Strategy in Retail Financial Services, the conclusion was that consumers will not switch financial service providers simply for a […]

LikeLike