It is hard to choose a financial advisor!

~44% of financial advice relationships today start from a referral.

Most people have trouble evaluating a financial advisory practice from the outside, so instead of spending hours scouring the internet and checking references, many people outsource the decision of whether or not a financial advisor is ‘good’ to someone they trust who already uses their services.

This decision carries a lot of weight. Not only does a high degree of information asymmetry exist in typical financial advice relationship, but good advice and quality portfolio construction can have a meaningful impact on a family’s financial outcomes. By selecting a financial advisor, you are selecting a quarterback for your financial life. Someone who you can outsource your decision-making to and sleep peacefully knowing that a professionally trained and regulated practitioner is responsible for your money. Trust is imperative in this relationship.

But what if you chose poorly? This question seems to haunt people who have multiple financial advice relationships. The phrase ‘don’t put all of your eggs in one basket’ applies here. People diversify horizontally to avoid the risk that their financial advisor might underperform or do something that is not in their best interest. Instead of delegating decision-making to one person, they spread this task out over many.

Stacks of Discretion

The multiple-financial advisor situation, while more common than you would think, is not how the average individual operates. Most people have a primary financial advice relationship, one person whose advice (or discretionary decision-making) we rely on to manage our hard-earned money… at least that is how it seems.

In reality, we all have multiple people whose decisions can materially impact our portfolios. While the multiple-financial advice relationship person diversifies their decision-making horizontally, most of the financial services industry today exists to diversify decision-making vertically. The financial advisor relies on the fund manager who relies on the management teams of the individual companies they invest in to make optimal capital allocation decisions. There are stacks of discretionary decision-making that comprise everyone’s portfolios.

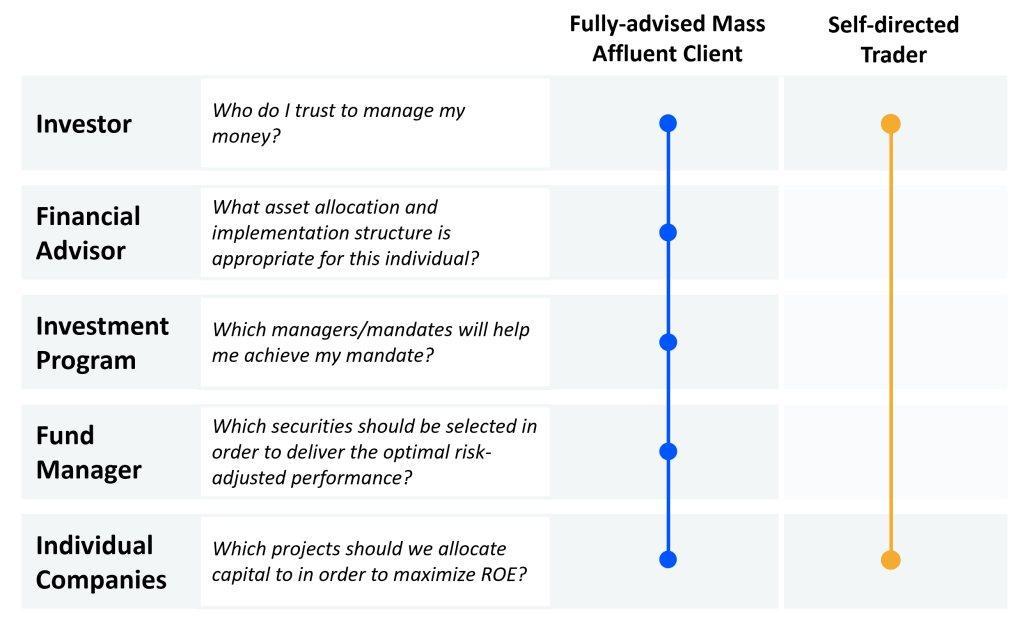

How many capital allocation decisions are in your investment products? Well, let’s take the example of a mass affluent individual who has a typical relationship with a planning-focused financial advisor.

At each level of the stack, decision-making takes place and each time someone makes a decision, a different path can result.

- Investor: Who do I trust to manage my money? Which aspect of my finances requires their expertise? What level of discretionary decision-making do I want to give them (check-in with me before executing any transaction, or complete and full discretion to make decisions on my behalf)?

- Financial Advisor: What asset allocation is appropriate for this individual? What structure is most effective to implement the selected asset allocation (advisor managed portfolio, separately managed account, investment fund, etc.)? Which fund managers should I rely on to make security selection decisions?

- Fund Wrap Program (Fund-of-funds): Which investment fund managers/mandates will help me achieve my mandate?

- Investment Fund Manager: Which securities should be selected in order to deliver the optimal risk-adjusted performance while staying within the bounds of the investment fund’s mandate?

- Individual Companies: Which projects should we allocate capital/resources to in order to help the company maximize its return on equity?

The example used was the most ‘heavily’ advised option with five layers in the decision-making stack. But not everyone opts for that model of financial advice. On the other end of the spectrum, some people want to retain the discretion to make their own financial decisions and even build their own portfolios from scratch. Their stack would be greatly simplified, consolidating decisions from further down into the Investor layer:

- Investor: What asset allocation is appropriate for me? What structure is most effective to implement the selected asset allocation (funds or direct security selection)? Which securities should be selected in order to deliver optimal risk-adjusted performance?

- Individual Companies: Which projects should we allocate capital/resources to in order to help the company maximize its return on equity?

Between the self-directed and heavily-advised investors exists an entire middle ground of options.

The Optimal Stack is a Balancing Act

The choice of how many decision-makers to include in how your money is managed requires some trade-offs. Two of the most important are the alpha-cost trade off and the diversification-conviction trade off.

Trade-off #1: Alpha Generating Opportunities for Cost

When it comes to the stack of discretion, each layer is being paid a fee for their decision-making services. In general, the more a decision-maker is pursuing the goal of generating above-average risk-adjusted returns, the higher the cost will be. For example: advisors with particular specializations or expertise tend to be able to justify a higher fee than those who are generalists; fund managers with active mandates tend to be more costly than managers with passive mandates; and, companies pursuing aggressive growth strategies tend to be more expensive (on an earnings/revenue multiple basis) than mature businesses with steady recurring cashflows.

Trade-off #2: Diversification for Conviction

Some investors frame success as the ability to achieve their financial goals. Other investors have more profit-driven motives and frame their success around their ability to maximize their investment returns. As another rule of thumb, the greater the number of layers in the stack of discretion, the lower conviction the portfolio will be. Each decision-making layer adds an element of diversification to the portfolio. The advisor’s choice to use a fund-of-funds or directly select securities themselves will likely produce starkly different outcomes in a person’s investment exposures. If the investor aims to pursue a specific investment objective or thesis, they will typically need to be selective about the number of layers in the stack.

Guidance on Navigating Stacks of Discretion

Trade offs can be found across almost all decisions related to one’s investments. In fact, decision-making is the essence of capital allocation itself, so it is worth understanding whose decisions ultimately have an influence over how your money is managed. To offer some general guidance:

Personalization: Every investor is different, so is every financial advisor or investment fund manager. Given that people have varied investment theses, financial objectives, risk tolerances, and willingness to delegate decision-making to others, there is no single stack that works best. Each person must pick the stack that fits best with their own personal circumstances and understand the trade-offs they are making when they add or remove a decision-making layer.

Decision-making dilution: The more decisions that are made within someone’s investment portfolio, the more likely those decisions might act to cancel each other out. At the top of the stack, a decision’s influence on investment outcomes can become diluted as more decision-makers are added to the pile. Moreover, those with multiple financial advisors or multiple investment fund managers may end up with competing investment exposures or a lower/higher than wanted degree of diversification. By understanding and evaluating the stack, redundant or counterproductive decision-making can be uncovered.

Stacks of fees: In general, the greater the number of layers, the greater the number of intermediaries and the greater the number of fees. That does not necessarily mean the stack will be ‘high cost’, but it is worth considering at each layer if the fee is worth the decision-making service provided.

Counterparty risk: The taller and wider the stack, the greater the number of decisions. Each decision made introduces a small but varied chance of error, randomness, or in rare cases, malicious actions. It is wise to vet each decision-maker in the stack, but also consider the non-zero chance of something going awry and whether or not adding additional decision-makers will increase those odds.

A Note on Crypto

This last consideration is incredibly important in the crypto arena today. While different from the investment advice example used to illustrate the concept, each intermediary layer added between your crypto access point and your coins introduces a higher level of counterparty risk to your portfolio. At Celsius, for example, the company was given decision-making authority over customer assets. That authority was used to trade customer assets and put deposits into risky, untested investments.

Probably the most egregious example took place late last year at FTX who took the deposits of trusting investors and used them to cover up trading losses at sister company Almaeda Research. This was particularly precarious since most investors would have made the assumption that FTX and its principals should have had ZERO discretion over their funds (and anything other than that would constitute fraud). Unfortunately, that turned out not to be the case.

In a different vertical, most DeFi degens should also consider the ‘stack’ they create while executing trades or farming for yield. The beauty of DeFi protocols is that they spell out how they make decisions in code, so there is little counterparty risk from that perspective. The bigger risk in the DeFi stack is the technical, smart contract and cybersecurity risk present in each layer. For someone who has chained together multiple protocols to execute a strategy, their stack is only as strong as its weakest link. The greater the number of layers, the greater the chance of something going wrong.

Conclusion

Another way to describe the stack of discretion present in financial services is simply as the industry’s value chain. This string of decisions demonstrates the beauty of how the financial system executes on its primary function: optimizing the allocation of capital from net savers to net spenders through effective and functioning capital markets.

Each layer of the stack exists in service of delivering value to the end customer. Unfortunately, people differ significantly in the way they define value [ie meeting financial goals versus maximizing financial returns], so the optimal stack of discretion will vary from person to person.

Despite this variability, it is worth considering the breadth and depth of your stack. After all, you probably want to know who is making decisions about your money.