Have you ever smashed a TV with a baseball bat…? Yeah, me neither. But thousands of people have in the safety of a controlled environment known as a ‘rage room’.

Every single day, a collection of frustrated executives, divorcees and whoever else requires a little cathartic release pay money to go destroy some objects and knock down some walls with nothing but their bare hands and a few supplied tools.

Of course, this is not a post about rage rooms… but it is about knocking down walls.

In front of every potential customer you want to convince to use your product sits a wall of switching costs.

For some industries, especially those that are relatively new on the scene, the wall of switching costs is quite low. People can change providers with relative ease thanks to low levels of product commitment, low friction processes, or low financial switching costs.

But for other industries, typically those that are more mature like the financial services industry, the wall of switching costs that sit in front of a potential customer can be enormous. Case and point, when was the last time you switched your primary chequing account? If you’re anything like me, the answer is almost never. I have maintained the same chequing account that I’ve had since I first opened it up with my mother at my side when I was twelve years old. Sometimes I see an advertisement offering a $300 welcome bonus or a free iPad and get tempted to open a new one. But then I remember how much of a pain it will be to change where my paycheque gets deposited… and change all of my pre-authorized debits set-up to automatically pay my bills… and resave my online VISA debit payment details… and add all my contacts back to my peer-to-peer (Interac) payment options… and then I think about the laborious process of actually opening another account, getting KYC’d, moving all of my funds over, getting familiar with a new interface, paying the account closure fee… you get the point.

This describes the wall of switching costs that sit in front of a typical checking account customer. Suddenly that free iPad doesn’t look so enticing.

Why Switching Costs Matter

Switching costs influence our decisions everyday. On one hand, they add some stability to our lives, keeping us from hopping from provider to provider. On the other hand, they create inertia, holding us back from something that is potentially better.

Understanding switching costs is key to understanding how to compete in almost all markets/industries today. For anyone aiming to grow or acquire new customers in a mature business, switching costs are the invisible force that hold market share numbers steady.

Breaking Down the Components

So, if switching costs are so important, what are they exactly?

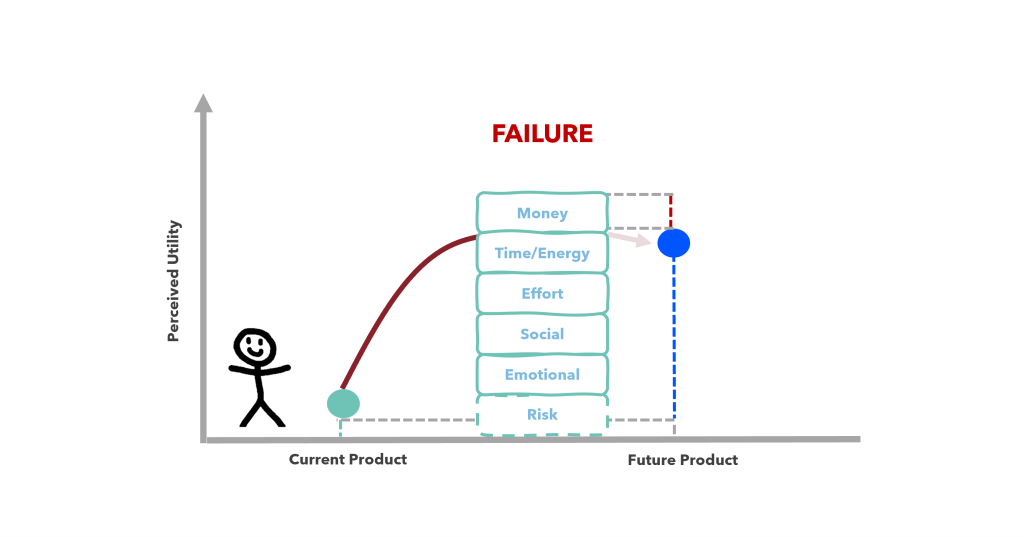

- Money: The most obvious and explicit costs to switching providers are any monetary costs required to do so. There is a $25 account closure fee to shut down my checking account at my existing financial institution. That is an obvious, explicit and quantifiable cost to make a change. Simple to evaluate.

- Time/Energy/Effort: The additional effort that is required to be expended to switch is also a powerful form of switching cost that is also relatively easy to evaluate (just look at the thought process that goes into evaluating the steps to change a primary checking account). There is often room for error in judgement here, either underestimating (wow, that was easy!) or overestimating (ugh, why did I start this process) the required effort.

- Social/Emotional: Social switching costs are a little more difficult to evaluate. These are costs that derive from the impact making the change will have on your relationships with others. Sometimes this cost is zero, other times, it may be significant, like telling your financial advisor who is a family friend of 20 years that you’re moving your money to someone new. This treads into the territory of emotional switching costs, which are the most challenging to identify. The intangible yet unwavering affinity you have for a specific brand, for example, weighs as a switching cost when evaluating whether or not to make a change.

- Risk: The perception of risk is also a potential switching cost that may not be present in all situations. But, if there is a degree of uncertainty about the outcome produced by the product being switched to, then risk may factor into the decision-making.

The Simple Rule of Switching Costs

Any company that has come up against slow customer turnover and long average customer lifetimes knows how frustrating competition can be. That’s why understanding the wall of switching costs that sit in front of any potential customers is a useful exercise. Building on the wall analogy, we can draw out a simple rule for evaluating how to compete:

The Simple Rule of Switching Costs: To Make a Switch, the Utility of a Product Must Be Greater than the Sum of the Existing Product’s Utility Plus Its Switching Costs.

In other words, the perceived net benefit that a potential customer will get from switching to a product needs to be greater than the wall of switching costs in front of them. If the customer sees something that is miles better on the other side of the wall, they are going to make the jump to get over it!

However, if the wall of switching costs proves to be too high, the change will be rejected.

There can also be situations where switching is not motivated by what’s on the other side of the wall, but rather will be motivated by the negative utility of the product the customer has today. If a customer is so frustrated with their current situation, there’s almost no wall of switching costs high enough to hold them back from jumping over.

The Simple Rule of Switching Costs gives us a formula for how to compete. There are three options:

- Knock Down Walls: reduce switching costs

- Build Up the Product: create more value

- Find Negative Utility: identify negative utility situations

What follows is an examination of each through the lens of an example: competing for wealth management customers.

A Wealth Management Example

Clients of financial advisors have mountainous switching cost walls to climb.

First, there are monetary costs to moving money to a new wealth management firm. These are often called ‘account closure fees’ or ‘transfer out’ fees and they can range from $0 to $250. There may also be hidden costs in the form of back-end sales commissions, or difficult to measure costs like the opportunity cost of funds in motion. There are also potential tax implications, if any taxable events are triggered along the way in moving the funds from A to B.

Second, there are significant time/energy costs. Clients must go through the onboarding and KYC process of the new advisor (often done in-person), handle the administrative burden and paperwork to set in motion fund transfers, and set-up and get acquainted with new technology systems.

Third, and perhaps most significant, are the social and emotional costs of ‘breaking up’ with your old financial advisor. Advice relationships are based on trust that is built over years of interaction and familiarity. Throwing this out the window to switch providers can be awkward at best and heart wrenching at worst.

There is also a degree of risk present in that no one can ever be certain of the outcomes produced by their advisor until they have been a client for an extended period of time. Moving money to a new advisor is always a leap of faith.

In total, combining these four elements, the mountain of switching costs in the financial advice business is sky high. Add to that, the fact that the wealth management industry is a mature business with little green space and you have the recipe for a market full of inertia.

Breaking that inertia is what every industry participant wants to do. The simple rule of switching costs and the three options it offers provide potential paths for those participants to take.

1-Knocking Down Switching Cost Walls: How to Break Through

The first option is the most fun. It involves going back to the rage room, finding the right tool, and smashing apart the wall of switching costs.

In most cases, ‘incentives’ are the tool(s) used to knock down the wall. To wield the incentive tool effectively, each of the component pieces (money, time/effort, social/emotional factors) of the wall must be studied carefully. What we are looking for are its strongest points. We want to find the pieces of the wall that are ‘weight bearing’ so when we knock them down, the rest of the wall crumbles with it.

In the wealth management example, monetary costs are non-load bearing. I can offer to cover ‘transfer out’ fees for clients that switch, but it likely will not be enough. I can offer discounts on my services (say 20 basis points off my 100 basis point fee), but those benefits are often too challenging to quantify. Even offering potential clients a monetary incentive on top (say $1000 for bringing over your $250k+ portfolio) often will not work either.

The pillar holding everything up is often the emotional connection to the previous financial advisor. If that bond is strong, it will be challenge to acquire the new user, even if your value proposition is much better. So efforts must focus on weakening that bond. But since we are not out to destroy relationships and reputations (there’s no room for savagery in financial advice), there must be another approach to take.

One path is to ignore the switching cost in the short-term completely and offer to take on only the ‘new money’ of the potential client. They save and allocate $20k per year to their current advisor—that becomes the target. The old relationship can stay intact while the new firm gets a foot in the door $20k at a time to demonstrate how much stronger its value proposition is. Perhaps more importantly, it gives the new advisor the chance to start building a personal connection that is stronger than the one with their old advisor. That’s why winning over new financial advice clients often involves a strong ground game and the ability to win relationships one by one. Whoever thought personal relationship building was going to fade in importance in an increasingly digital world clearly has not worked in the wealth management industry.

2-Building Up the Product: Creating Value and Generate Activation Energy

If personal relationship building is not the company’s strong suit, then perhaps the second path of building up the product/value proposition is the more attractive option. If the grass is always greener on the other side of the wall, then the objective here is to make your grass as green and as shiny as possible.

If most of the prospective client pool is with advisors that only handle investments, then double down on the insurance, tax and financial planning elements of the business. If the prospect pool consists of Millennials, show them an aptitude for socially responsible investing, crypto, first-time home buying, and whatever else will differentiate the value proposition in the eyes of that segment.

Building up the value is important, but it is meaningless without generating awareness and communicating that value to prospects. How a product is marketed is almost as important as the product that is delivered. Being deliberate about creating the necessary activation energy is imperative to overcoming switching costs when following this path.

3-Mining Negative Utility: Find Unhappy Campers

The final option is to focus on the current side of the wall. There are situations where prospective clients may be unhappy with their current providers but have yet to make a change. These are situations with negative utility, which makes it much easier for a new product to standout in their eyes.

Volatile markets often create a lot of unhappy campers in the wealth management industry, even though it is often not the fault of the advisor themselves. No one with a sufficiently diversified portfolio will be able to dodge volatility in all market environments. This is why customer turnover rates tend to skyrocket when market crash. While not ideal, this is an incredibly opportunistic time when the wall of switching costs is much easier to overcome for wealth management firms who are seeking new clients. This window, however, often does not stay open for long.

Summing Up

Switching costs are everywhere. They are always present, but typically hide in plain sight.

Slow moving industries can often be blamed on switching costs—stable customer bases and static market shares too. Because they have so much influence over our economic decisions and are the backbone of inertia in our lives, a deliberate analysis to better understand what the wall of switching costs looks like can go a long way in getting a leg up on the competition.

Also, like the rage room, once you are handed that incentive bat, it’s a lot of fun to start knocking down some walls!

One response to “Knocking Down The Wall of Switching Costs: Acquiring Customers in Mature Industries”

[…] Switching costs: The wall of switching costs in front of customers is quite high in the industry. Money, time, energy, and emotional costs all […]

LikeLike