Quick question: what is your credit score?

Can you answer this on the spot? If so, my guess is that you are one of the millions of people who have accessed and tracked their credit scores for free through forward-thinking services like CreditKarma and Borrowell. Their work has made it possible for anyone to better understand how credit works and how to improve their personal circumstances. As Peter Drucker says, “if you can’t measure it, you can’t manage it” and that is particularly true for credit.

Yet, credit scores and credit reports have been available directly from the credit bureaus for many years prior to the emergence of the companies above. Pick-up a phone, call the bureau, pay a fee and get access to your information. Easy. So why didn’t more people do that?

The problem was, credit scores and credit reports were not very legible.

Legibility is the quality of being easily accessed, read, deciphered or understood. Enhancing legibility means improving one or more of those characteristics. CreditKarma and Borrowell not only made credit scores easier to read and access, they have made them easier to interpret and understand.

Not only is my credit score now at my fingertips for free, so are the tools to help me understand how it is calculated, how my actions impact those calculations, and what I can do to improve my behaviour.

These firms have taken something that was knowable but difficult to access/understand and made it legible for the broader public in a way that benefits ‘the people’.

In essence, they have enhanced financial legibility.

Finding a Formula

These early credit scoring pioneers are tapping into a strategic formula that exists across industries. As the world moves online, our actions generate more and more data and our ability to capture, manage and store that data improves at the speed of Moore’s law.

The world is becoming more ‘machine-readable’, which in turn, creates new forms of legibility and accessibility.

The smartphone, for example, has made our personal location more legible. We likely would not have Uber, Waze, Pokemon Go, and a variety of other incredibly valuable apps without it.

Apple Watches are making some of our personal health metrics more machine-readable. Without it, we would not have digital healthcare apps that rely on the continuous stream of real-time health information, or to bring this back to financial services, we would miss out on things like Manulife’s Vitality program which rewards its life insurance customers for living healthier lifestyles.

Businesses can be built off the back of enhancing legibility. Of course, we could look to the smartphone and smartwatch manufacturers as obvious examples of capitalizing on this idea. But the leader in this field is actually found outside those domains.

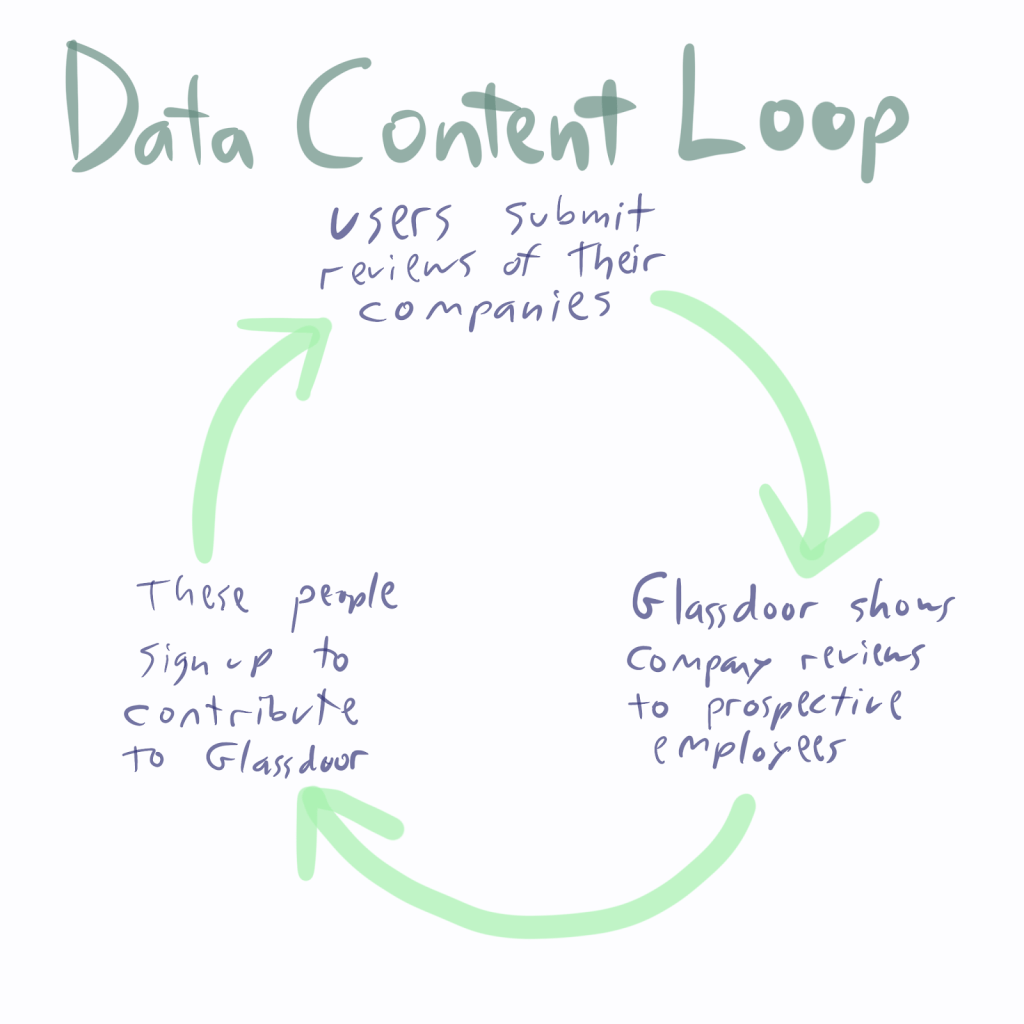

Rich Barton is a serial entrepreneur best known for founding Expedia, Glassdoor and Zillow. While those businesses covered very different industries, there is a common thread running through each. They made information more legible to the general public by building data content loops (see image below) that unearthed information that was previously hard to access or controlled by a middleman:

- Expedia: Prices for flights and hotels that before you’d have to get from travel agent

- Zillow: Zestimate of what your house is likely worth that before you’d have to get from broker

- Glassdoor: Reviews from employees about what a company is like that before you’d have to get from a recruiter or the company itself

As thoroughly explained by Kevin Kwok in “Making Uncommon Knowledge Common” (that I am borrowing from heavily here and I highly recommend you read his piece), the Rich Barton Playbook involves ‘giving power to the people’.

His companies take power from the incumbents and give it to consumers. Instead of trying to hoard information, they are on the side of consumers and giving them more data transparency… Glassdoor revealed how employees really felt about companies. Zillow shed light on what any house was worth. Expedia let people see the prices and availability of flights and hotels without talking to an agent… Rich Barton took these whispered conversations and made them public for everyone to see.

This does not just happen at a large scale with technology companies. I have experienced it firsthand in a business-to-business context. Financial services industry data and market share information was not readily available in Canada in 1992, that is, until Investor Economics (IE) was founded. The company built a ‘data content loop’ (again, read Kevin’s article), where the companies that comprised an industry (say Canadian full-service brokerage firms) would provide their private financial/KPI information to IE who would then aggregate that data creating legible industry totals for the individual firms to use in calculating their market share. BrightScope, a sister company in the U.S. founded by Mike and Ryan Alfred, followed a similar path for some of their products. As per RIABiz “they took the dusty records related to holdings of plan sponsors held in a government warehouse and put them online in useable form”.

Directional Arrows of Progress

Legibility can create entrepreneurial magic.

My takeaway: If there’s demand for information that is useful but hard to find, there is opportunity to make it legible and build a business around it.

This idea is a directional arrow of progress: a secular trend that dictates where progress is headed for a specific industry (a concept borrowed from Josh Wolfe at Lux Capital).

As a simple example, observe the arrow of progress around computers: Each generation was getting more powerful, smaller, and closer to our bodies. Wolfe and Lux have used that insight to predict that brain-machine interfaces will be a significant part of the future and have begun investing in the space.

Making this more specific, financial legibility is also an undeniable directional arrow of progress.

Financial Legibility

Financial legibility is simply making financial data more easily accessed, read, deciphered or understood.

What does this look like today? Without being comprehensive, legibility exists on a continuum from things that are already fully accessible and machine-readable at most financial institutions (like your account balance or transaction history) to things that are incredibly opaque pieces of financial information that are hard to locate, hard to understand, or both.

Legible:

- Account balances (first-party)

- Transaction histories and schedules (first-party)

- Investment performance

- Insurance coverage

Nearing Legibility

- Account balances + Transaction histories and schedules (third-party – thanks, open banking)

- Credit scores and reports

- Retirement planning and simple financial goals

- Insurance policies

Illegible:

- Income/payroll

- Shares in private businesses

- Tax assets/liabilities

- Insurance underwriting criteria

- Real estate values

- Hard asset values

- Human capital

Legibility Matters

What happens when we lack financial legibility? Well, for those that remember the time, try to figure out your financial position with an unbalanced chequebook.

Today, we have fantastic tools available to us that have made our personal financial circumstances more machine-readable which in turn has made our financial position easier to track, manage and understand. But as noted above, there is still a lot of room to improve.

As Thoreau says, “it’s not what you look at that matters, it’s what you see”. We have done a great job at putting certain pieces of financial information online, now we need to make that information more legible to help people understand it. It is great that I can now access my credit score, but that does not mean much without the additional context of how to improve it.

There are three key arguments as to why legibility is important:

- What gets measured gets managed: Legibility makes our financial health visible, both good and bad. In either case, once it is out in the open, it can be used to identify actions that can lead to bettering one’s financial position.

- Open systems tend to out-innovate closed systems: Making more financial data machine-readable means it also becomes more sharable and [potentially] available to others on a permissioned basis. That data can be used as the building blocks and inputs into other financial services, from alternative credit scoring engines to personal financial management tools. More open data should lead to greater degrees of innovation over time.

- Power to the people: Legibility empowers people with information. Innovators in this domain have the opportunity to eliminate information asymmetry between gatekeepers and consumers and put decision-making power back in their hands.

Finding Opportunity in Opacity

So we have established two things: first, financial legibility is incredibly important; and second, not everything is currently legible. This presents an opportunity.

Taking a page out of Rich Barton’s playbook, one strategy built on top of the financial legibility idea would be to find some piece of financial data that was knowable but difficult to access/understand and make it legible for the broader public in a way that benefits ‘the people’.

Let’s look at some examples:

Small Business Valuations: It is hard to provide good financial advice if you are only able to see a small portion of your client’s overall financial picture. It would be akin to a doctor diagnosing you with the flu while only studying your knees. Over the past several years, financial planning software has started to unearth some of that picture in the form of ‘held-away’ assets (assets held at other financial institutions). With progress being made on open banking rails, saving and spending data may soon enter the picture as well. But for small business owners, most of whom are very qualified clients for financial advisors, their largest and most important financial asset is missing from the picture. In many cases, their business is their retirement plan, yet it is incredibly challenging to see or understand its current and future value. A Canadian start-up, interVal, recently set out to tackle that problem. They have built a company around making small business valuations more legible. Not only that, the platform provides measures that help business owners and their advisors better understand how to improve and grow those valuations over time. Much like opening up credit scores to the masses, small business valuations have similar potential to empower people with knowledge where there was previously information asymmetry or no information at all.

Income: If we borrow some ideas from corporate accounting and apply them to the individual, we can see that there is one big component missing. Account balances are like balance sheet information (assets/liabilities/equity), spending and payments reflect the expense side of an income statement, and the missing piece is ‘income’ which would be the revenue side of the equation. Data on payroll or income has only been visible to financial service providers in a peripheral way to date, yet it is an incredibly important indicator of financial health (or from a credit perspective, important in assessing a consumer’s spending potential or “ability to pay”). There are a number of payroll API companies that have emerged to add legibility to this area of the household balance sheet. For financial institutions, companies like Argyle have developed a suite of use cases for income data, from income/employment verification, to paycheque-linked lending, to earned wage access facilitation. For the consumer, companies like Finch power a variety of services from unlocking tax credits to facilitating employee rewards and benefits.

Real Estate: How much is your home worth today? Referring back to the household balance sheet, the largest entry in the asset column for most consumers would be their primary residence. Real estate is likely one of the biggest financial assets a person will ever own and the value of that real estate will have a significant impact on a person’s financial position. Real estate, however, has always been challenging to value in real-time and bringing that value into the light has been idea powering Zillow and their Zestimate in the U.S. and HonestDoor here in Canada. That piece of information has a variety of uses, from entertainment (looking at how much celebrity homes are worth) to negotiating leverage (used as an input when buying or selling a home) to financial planning (giving the advisor a complete picture of a person’s retirement position).

In Summary

Your financial world is more than just your bank account and mortgage, it is all of the factors that make up your financial life.

Enhanced financial legibility not only helps out the consumer by painting a more fulsome picture of their financial position, but also provides new inputs for developers to work with in creating new products and financial institutions to work with in delivering better advice.

There is incredible opportunity to unearth the currently illegible. Directional arrows of progress only move in one direction, after all…