There is only one free lunch in investing… and that is diversification.

It is one of the only known ways to consistently improve the risk-reward equation of a portfolio.

In today’s equity-centric world, bonds have typically been relied upon as the primary offset, providing diversification benefits to the everyday investor. This is particularly true when equity markets hit a rough patch. Just look at the performance of fixed-income asset classes through the last several periods of market volatility:

In the above chart, the negative correlation that is typically present between stocks and bonds is quite prevalent. Stocks go down, bonds go up. Diversification works!

Unfortunately, an assumption investors often make is that these relationships remain constant over time. Correlations often depend on both the timeframe of measurement and the specific drivers of the relationship. In the short-term, bonds often act as a fantastic diversifier for equities due to their perceived ‘safety’. When markets crash, investors sell their equities and head for the safety of the bond market to wait out the storm. This relationship has held true over extended periods of time.

On longer-term timeframes, however, the negative correlation between stocks and bonds is less consistent. Last year, for example, U.S. stocks and bonds fell 18% and 13% respectively, a positive correlation, which was a real cramp in the side of 60/40 investors. Using a rolling 24-month window over the past century of returns, we can see that there are extended periods of time where stocks and bonds are positively correlated, the opposite of the commonly held perception.

Because correlations tend to shift over time, we cannot assume things that provided diversification in the past will provide the same benefit in the future. This is why exploring the Conveyor Belt of Finance (alternative investments) is so important. We must diversify our diversifiers!

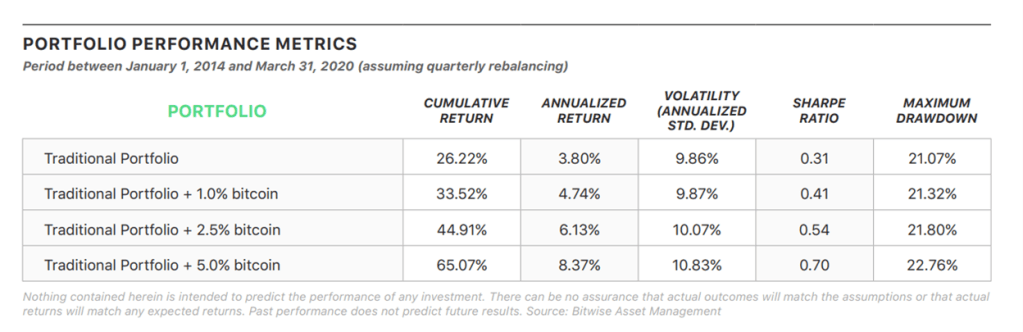

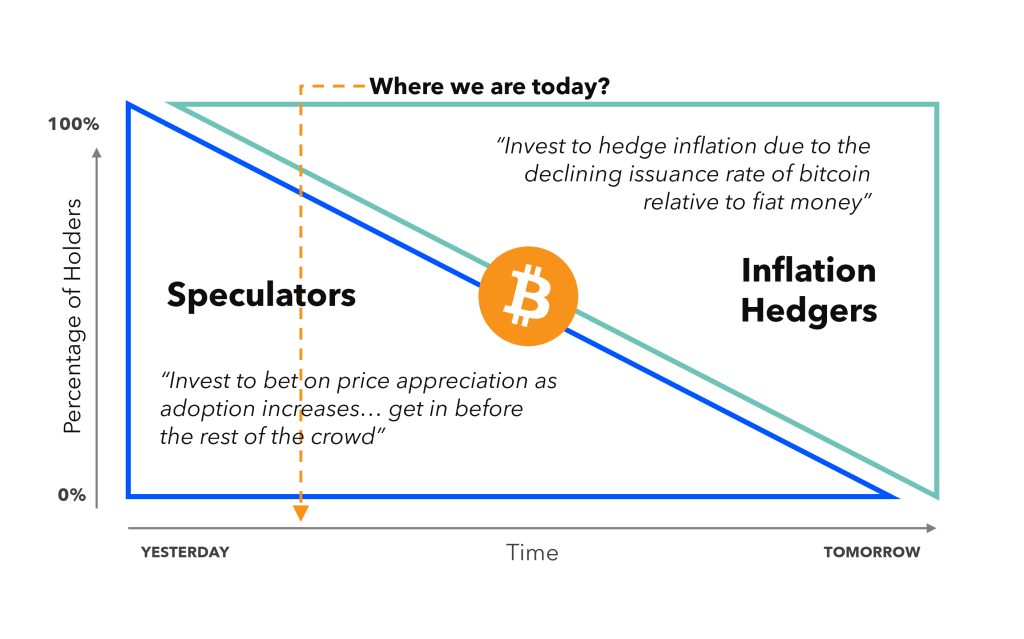

One of the newest portfolio diversifiers on scene are the assets sprouting from the crypto industry. Bitcoin in particular, has received a lot of attention from both retail and institutional investors looking to improve the risk-adjusted returns of their portfolios. The theory goes: Allocating a few percentage points of a portfolio to bitcoin can give Sharpe Ratios a boost. A recent study by Bitwise seems to suggest that theory has some substance.

Assuming quarterly rebalancing, adding between 1% and 2.5% Bitcoin (BTC) to a portfolio of 60% stocks and 40% bonds from 2014 to March 2020 added 1% to 2.3% to annual returns without a significant increase in portfolio volatility or drawdown.

Of course, there is a lot of point sensitivity in studies like this and the results are heavily dependent on the timeframe chosen (as was noted above regarding stocks and bonds). But crypto is a unique asset class with a unique set of influences impacting its price. It is also multi-dimensional, offering both price appreciation and yield as a potential source of returns. There’s more to the crypto-diversification story than just adding bitcoin to a 60/40 portfolio. In fact, there are four correlation narratives that are proving this to be true.

1/ Uncorrelated Risk Premia from Equities

If you have listened to any podcasts featuring Mr. Wonderful lately, you will know Kevin O’Leary often says (and tweets) that “crypto will become the 12th sector of the S&P 500.” The suggestion that crypto could integrate well into an index full of the world’s largest companies highlights the fact that there are parallels and similarities between crypto and corporations.

Modern companies are:

- financed by a capital stack (often consisting of debt, equity and everything in between)

- governed by a corporate charter

- operated through distinct legal structures (ie.LLCs)

- comprised of a variety of people and stakeholders

- stand as an incredible example of people coordinating at scale around a shared objective.

Looking at Layer 1 protocols (L1s) as a comparison, each protocol is:

- anchored by a capital stack (tokens)

- governed by a white paper or set of on-chain or off-chain processes

- operated through distinct structures (companies, foundations, DAOs)

- comprised of a community of stakeholders

- stand as an incredible example of people coordinating at scale around a shared objective.

This similarity would suggest that L1 tokens (using ETH as a proxy) should have a high degree of correlation with the stock market. In the same way that investing in a stock is a bet on the future cash flows and demand for a company’s product, investing in a token is a bet on future adoption and potential cashflows associated with staking or participation.

While ETH-S&P500 went through a period of low positive correlation between 2017-2021, the risk-off environment that has persisted through 2022 and 2023 has brought correlations higher toward the 0.50 level.

This tightening makes a lot of sense. Although token holders have a different set of rights than equity holders, the success of each of the projects they are dependent on is subject to a similar set of risks: operating risk, financial risk, governance risk, legal/regulatory risk, etc.

These risks band together to form both an equity risk premium and a token risk premium, and while we won’t get into defining those here, suffice to say that it is the similarities between the two risk premia that bring correlations closer to 1.0 and it is the differences in the risk premia that move them in the other direction.

DAOs, improvement proposals, tokenomics, protocol architecture, developer enablement, community formation, app development, etc. all bring an element of uniqueness to crypto protocols that does not exist same form in traditional corporations. That uniqueness will likely continue to provide some separation from equity markets, keep correlations low, and provide a strong case for crypto as an equity portfolio diversification tool.

2/ Uncorrelated Yield from Fixed Income

For a long time, crypto assets were thought to be a non-productive asset. That is, they did not generate a meaningful stream of cashflows like stocks or bonds. While Charlie Munger still thinks this is the case, the birth of proof-of-stake consensus mechanisms in 2012, the explosion of activity surrounding “DeFi summer” in 2020, and the successful merge in 2022 between Ethereum’s Mainnet and Beacon Chain to transition the protocol to proof-of-stake would all suggest crypto assets are trending in the direction of ‘productive’.

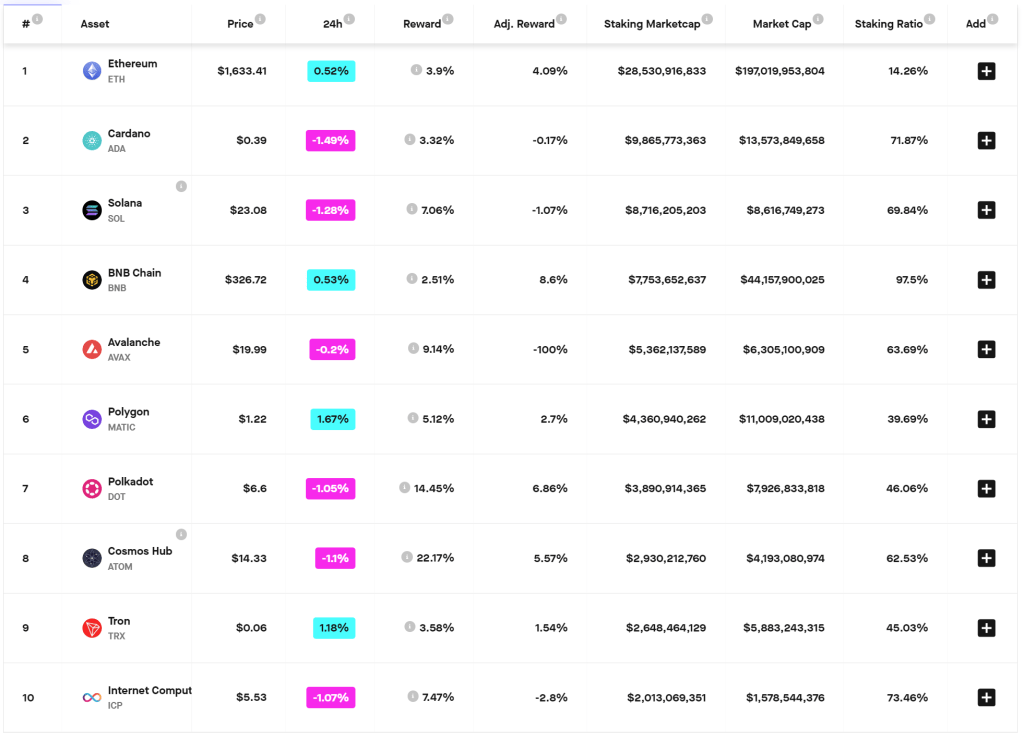

The current staking reward for running an Ethereum validator is currently 3.90%, a number that is expected to increase following the Shanghai upgrade (providing liquidity to staked ETH) later this year. Other protocols, while potentially higher risk, have even greater staking yields (see Polkadot and Cosmos at 14.45% and 22.17% respectively).

Staking, as noted here in Why Staking Matters, makes assets directly productive:

Staking uses capital to complete the financial labor of running and securing a financial system (aka blockchain) akin to the manual labor in the traditional financial system that used to be handled by banks, payment rails and clearing houses. It is a way to make idle assets ‘productive’ by having them participate in the execution of financial tasks in order to earn a return.

Because of its function, staking yield will likely have a different set of influences than other financial products with fixed income-like return profiles which are heavily dependent on the price of money in the economy.

Staking can also be a gateway into the world of DeFi, which offers token holders a variety of other opportunities to repeat that increasingly familiar behaviour of locking up assets in exchange for yield.

Liquidity pools, lending, derivatives, and maturity transformation all offer ways to earn yield by pledging your assets to a protocol for productive ‘secure’ use. The fact that these yields have a variety of influences mean that correlation with other assets will likely be well below 1.0, but will also be volatile as the assets and their ownership groups mature.

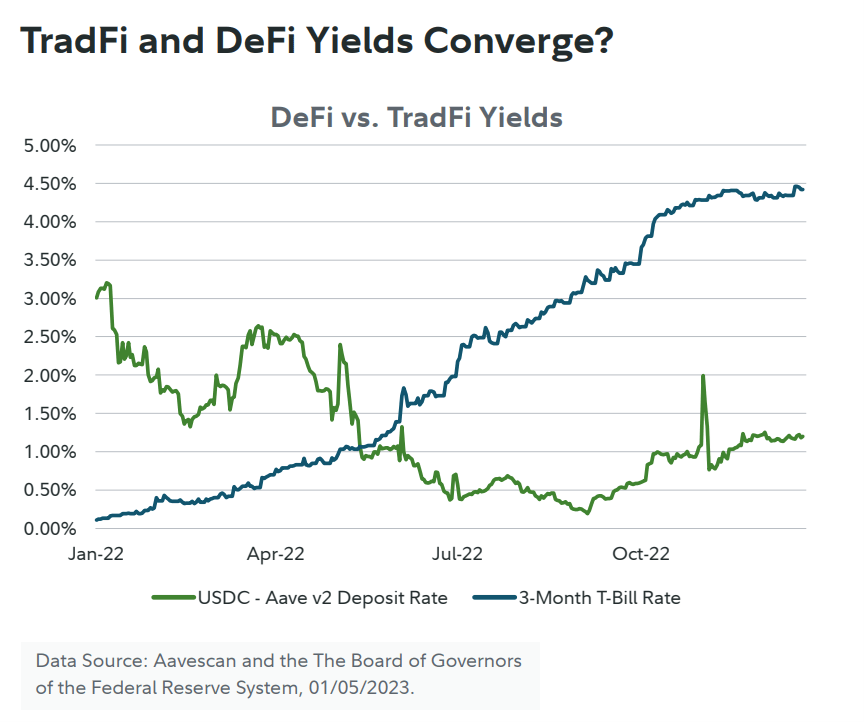

Sometimes this lack of correlation works in an investor’s favour. Other times, like in the present day, not so much. DeFi yields are much more dependent on risk appetite in the market, while traditional fixed-income yields are much more central bank dependent. Consequently, DeFi yields have fallen over the past year, while TradFi yields have risen.

Gone are the days that the crypto community could poke fun at the measly 0.05% rates most large financial institutions were offering on their savings account (currently, these are closer to 1.50%-2.00%). However, things will ebb-and-flow, and at some point in the future, DeFi will be back on top. The point here is that because DeFi and Staking yields have a separate set of influences from traditional finance, their yields will likely remain uncorrelated or even negatively correlated to the price of money in the economy. For fixed-income investors, the fact that on-chain assets are becoming productive means that fixed-income portfolios have an opportunity to diversify their yield exposure even further.

3/ Uncorrelated Stability from Other Currencies

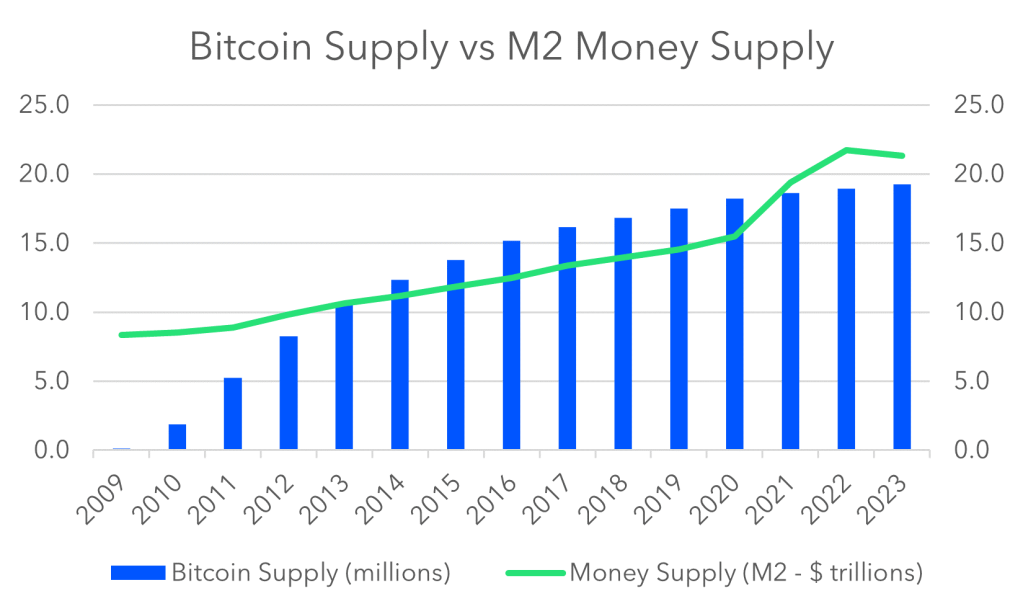

Looking at crypto in its namesake form, as a currency, there are also some nuances to look at in terms of correlation. Bitcoin is the OG cryptocurrency and arguably functions very closely to sound money (although, ultra sound money theorists would disagree, so to would stablecoin aficionados).

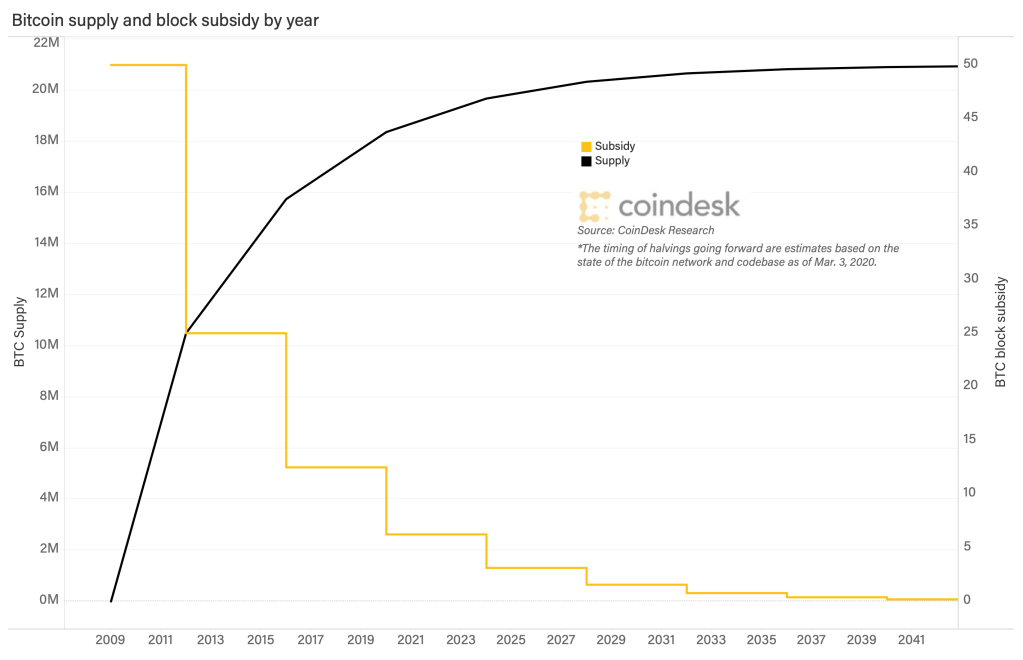

The reason bitcoin functions as sound money is because of its stable monetary base. Bitcoin has a known supply schedule, one that is embedded in the code of the protocol.

Traditional currencies, however, have a less stable issuance rate. The result has been a contrast in the supply of traditional money with that of crypto money.

Again, with a different set of influences and owners, cryptocurrency is likely to remain uncorrelated from traditional currency when it comes to its supply. That is also true when it comes to demand. However, demand for crypto is strongly synchronized with demand for other risk-assets. That fact is very evident in the data over the last several years, where bitcoin correlations with U.S. equity markets have risen up to 0.4.

While these demand characteristics will likely dominate the price action in the near-term, as the crypto industry matures, the demand factors will likely fade away as ownership groups (those who own traditional assets and those who own cryptoassets) start to blur even further. What will be left are the supply factors, where bitcoin’s role as a potential inflation hedge may eventually be realized. Should it ever come close to fulfilling that goal, bitcoin will also begin to prove that it is a powerful diversifier when it comes to a basket of currencies.

4/ Uncorrelated Signal from Cultural Noise

Beyond the financial industry are the other areas of the economy where crypto is beginning to expand. Under the guise of Web3, crypto is beginning to enter the cultural arena by giving us new on-chain signalling vehicles in the form of both NFTs and fungible tokens.

As individuals, each of us is comprised of a mosaic of signals. We use them to tell the world who we are through the clothes we wear, the things we buy and the communities we belong to. Often the choices we make about the signals we send are aimed at the objective of catching the latest cultural wave or showcasing some deeply held values.

For many people, particularly those with wealth, signalling is often done through a portfolio of owned items and collectibles. Most wealthy people I know have a wine cellar in their basement, fine art on their walls, and classic cars in their garage. For this crowd, NFTs are culturally uncorrelated from their traditional signalling mechanisms. Web3 offers a way to diversify one’s personal identity portfolio through a new type of ownership and signalling vehicle. After all, the NOUNS you use as your profile picture and the 75 FWB tokens in your wallet say a lot about who you are, both online and increasingly offline.

While it may eventually fade, today, crypto provides an uncorrelated form of culture that stands out from the mainstream, which is also a diversification opportunity for those who only have exposure to plain vanilla cultural items.

Correlated Conclusions

The uncorrelated nature of crypto extends beyond its parallels with the equity market, which makes it useful in a variety of other contexts in bringing forward the benefits of diversification. Unfortunately, in the crypto community, diversification is often overshadowed by another force: conviction. Many people are true crypto believers with factions that tend toward maximalism—an all-or-nothing approach that functions as both a belief system and a portfolio structure.

These ‘maxis’ will likely never be the beneficiaries of the perks of diversification discussed above. Those are reserved for people who take a portfolio-based approach to their investments, their income, and their social signals… which is the majority of mainstream investors today.

Broader adoption and use of crypto assets in portfolios will likely come alongside one of the four correlation narratives discussed in this essay. Diversification is a simple and trusted narrative to bring an edge case into the mainstream.

Ironically, as crypto begins to cross the chasm, the benefits of diversification will likely shrink. One of the reasons correlations tend to converge over time is because the two assets being measured share a growing ownership base and therefore respond to a similar set of influences. While crypto enjoyed a strong retail investor bias early on, institutional capital is beginning to play a larger role in the ecosystem and as that has occurred, crypto correlations have slowly trended closer to traditional assets.

For now, however, crypto provides diversification-as-a-service. Simply sprinkle a portion on a portfolio and wait for the magic to occur.