Today, it is hard to write about business without any mention of technology companies.

From Apple to Amazon to Facebook, today’s tech giants are arguably the largest and most impactful organizations ever built.

But when it comes to understanding this broad category, I’ve found myself asking: what exactly is a technology company?

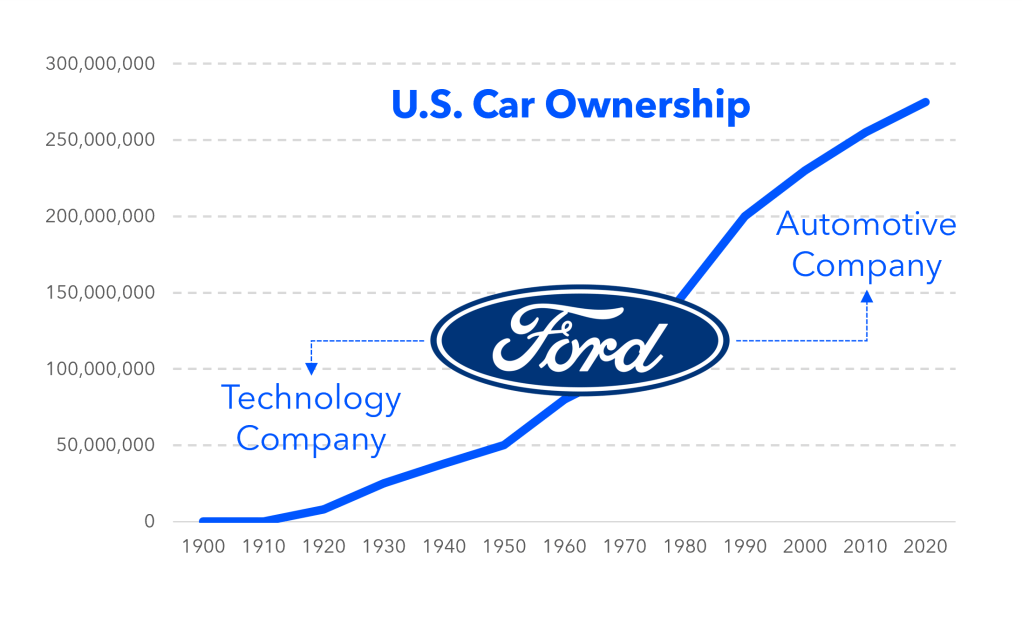

According to Investopedia, technology companies engage in the research, development, and manufacture of technologically based goods and services. Today, those ‘goods and services’ are primarily made of bits. They are information technologies. But prior to the 1970s, ‘technology’ was primarily made of atoms. For example, when the automobile first came on scene, Ford was considered to be a ‘technology company’ as were the other auto manufacturers of the time. Those firms harnessed the era’s current technology (internal combustion engines) to create a set of capabilities and performance that the horse and buggy could not match.

But Ford, along with its industry brethren, eventually shed the technology company label. When the internal combustion engine technology reached maturity and the industry reached the point saturation, they simply became part of the ‘automotive’ sector.

Once a technology hits the mainstream, the ‘technology company’ label is no longer apropos.

Alternative Investments

Like the term technology company, I’ve also found myself contemplating what exactly is an ‘alternative investment’?

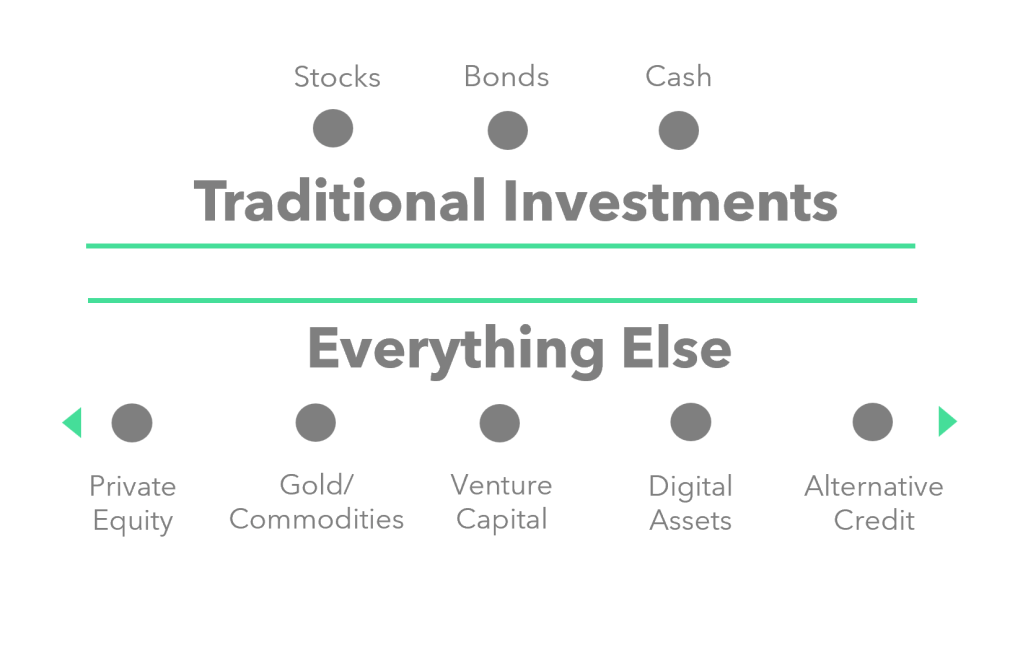

Back to Investopedia, an alternative investment is a financial asset that does not fit into the conventional categories of equity/income/cash. That is, almost any asset category that offers non-traditional (or non-mainstream) investment exposure can be considered an alternative.

Traditional investments—stocks, bonds and cash—are the basic components of the 60/40 portfolio. Alternative investments are… everything else.

For decades, this has been the taxonomy by which many investors and allocators have viewed the world. It is simple, intuitive, and stable. Things move slowly in the world of finance and the labels of ‘alternative’ and ‘traditional’ provide a nice static organizing framework.

This article is about why that framework is outdated.

Finance is not static, it is dynamic.

Regardless of the labels we put on them, investment exposures are continuously moving from alternative to mainstream.

This is the conveyor belt of finance and it is constantly at work.

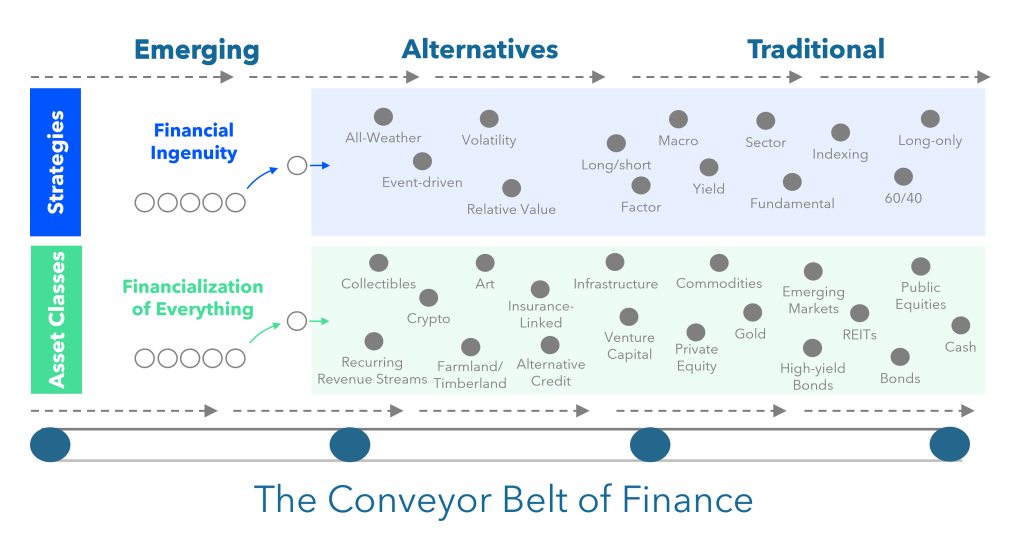

The Conveyor Belt of Finance

On the conveyor belt are two forms of investment exposure: Strategies and Asset Classes.

Strategies are applied methodologies that aim to consistently capture distinct risk premia. They can exist across asset classes, from public and liquid equity markets to private and illiquid credit markets. Strategies often start as forms of financial ingenuity aimed at generating alpha. Some unique market insight, information advantage, or analytical framework is applied to an asset class in a new way. Success typically begets copycats. As more people apply the strategy, the once present alpha is harvested away, leaving behind new forms of alternative beta for the market to access. The long-short equity strategy that coincided with the birth of the hedge fund in 1949 followed this cycle, where the novelty of buying stocks and hedging the positions with short sales eventually wore off as the strategy’s popularity grew, leading to today where alpha generation in the world of public equities has shrunk as these strategies have reached maturity.

Asset classes are groups of financial instruments that have similar investment characteristics. They often begin life through financialization which is the process of standardization and market formation that facilitates the exchange of an asset class. Financialization is a journey. For public equities, this financialization process took place over centuries where the first stock exchange (credited to the Amsterdam Stock Exchange in the 17th century) created the first centralized access point to trade secondary financial interests in large companies. Fast forward to today, almost anyone can access public equity markets through an app on their phone, with little to no cost, trading global securities, in any quantity (even fractions), during extended market hours. While public equities have matured in their financialization journey, other asset classes are still at varying points when it comes to their accessibility, liquidity and tradability.

Propelling both strategies and asset classes forward on the conveyor belt is the pursuit of the benefits of alternative investments, namely, enhanced returns (or risk-return profiles) and broader diversification. This is complemented by industry dynamics including: advancements in technology, the need for differentiation in asset management and wealth management, and growing investor acceptance.

• The Pursuit of Enhanced or Uncorrelated Returns: The ultimate goal of most alternative investments is to improve the risk-return profile of investor portfolios. This generally begins with the pursuit of alpha, particularly when it comes to strategies (ie. equity market neutral or convertible arbitrage). With asset classes, alpha can be found in early adoption, getting to the asset class ahead of the masses as it shifts from alternative to mainstream (ie. crypto or fine art). There is also a sub-category of asset classes that is simply about uncovering or exposing new betas where adoption does not play a role. The asset class currently exists in private hands which is transferred into new hands as access opens up, keeping supply and demand relatively balanced (ie. reinsurance or infrastructure). Delivering on the promise of enhanced or uncorrelated returns is what pushes continual progress on the alternative investments shelf.

• Advancements in Technology: The changing technology landscape pushes the boundaries of every industry. For alternatives, particularly emerging alternatives, technology has enhanced most of the ingredients necessary for financialization to take place. Marketplaces have formed (ie. for private securities like on CartaX or for fine wine like on Vinovest), data has improved, distribution channels have opened up (thanks to firms like iCapital and CAIS), and infrastructure/services around the ecosystem (like Passthrough) are all accelerating discovery, maturation and adoption.

• Differentiation in Asset Management: It is safe to say, asset management is a mature industry. The primary characteristic of mature industries is intense competition. In domains where betas have been commoditized (most long-only equity or fixed-income strategies), differentiation becomes a challenge. For asset managers looking to step out of these beta-laden red oceans they have been swimming in for too long, alternatives provide an attractive new blue ocean to explore.

• Differentiation in Wealth Management: Over the bull market of the past decade, the rise of index funds was driven by the advisor community who brought a value proposition to their clients that read like this: I can substitute your portfolio of pricey actively managed mutual funds for my tactically managed portfolio of low-cost index funds. During the bull-market, these fairly vanilla 60/40 portfolios did well. Since the inflation-driven turn in the markets in 2021, a similar narrative may help advisors drive the adoption of alternative investments: I can substitute your portfolio of low-cost index funds for the enhanced risk-adjusted returns of a portfolio that includes alternatives (which is now possible as new channels of access open up, track records become established, and advisor comfort levels grow).

• Growing Investor Acceptance of Alternatives: Finally, there may also be a push toward alts from the consumer side. Whether we like it or not, our portfolios are signaling vehicles that say a lot about who we are. Owning bitcoin says something about you just like having your money with a certain hedge fund manager might have back in the 1990s. Culture has become finance and finance has become culture and alternative investments offer specific ways to express yourself through your portfolio.

A Tour Across the Conveyor Belt

New asset classes and strategies are born everyday. A select few manage to climb the S-curve of adoption. Fewer still manage to mature into portfolio staples. This pathway describes the three stages an investment category will move through as it sits atop the conveyor belt.

Emergence: The Birth of a New Investment Category

Feeding the conveyor belt are two powerful forms of innovation: financial ingenuity and the financialization of everything.

Financial Ingenuity describes the explosion of investment strategies that have found their way into portfolios over the preceding decades. As long as financial markets exist, there will be people seeking to discover and test trading strategies in the hope of generating alpha or discovering a new beta (because doing so successfully can be a path to creating immense piles of wealth).

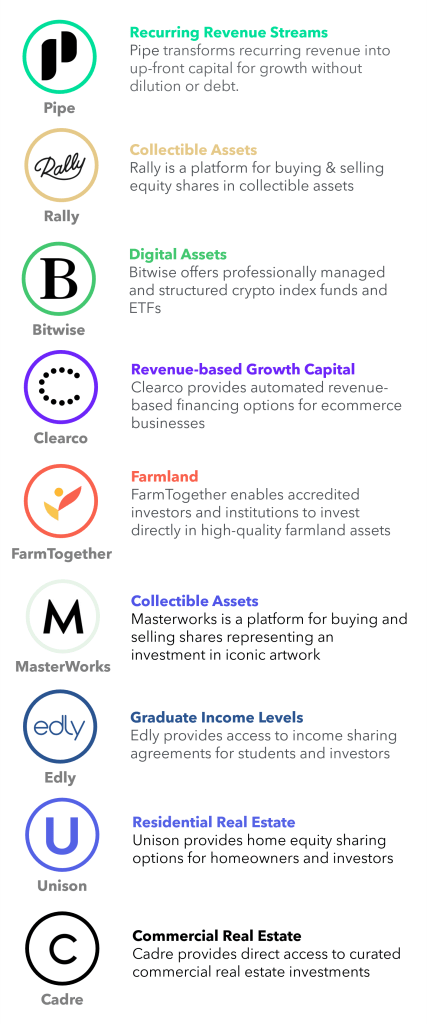

The Financialization of Everything refers to the idea that new asset classes are born everyday as start-ups and innovative companies create investable opportunities out of previously uninvestable areas. Crypto, collectibles, and recurring revenue streams are all examples of things that have burst into the investable universe in the past several years (see below).

Alternatives: Climbing the S-Curve of Adoption

Once a new investment category has burst onto the scene, it starts out on the path to reaching ‘traditional’ status. To get there, it must climb an S-curve of adoption which involves solving some of the primary issues new investment exposures face:

- Cost – from crypto trading fees to the 2/20 model used by many hedge funds and private equity firms, alternative investments often have higher cost models either due to a lack of scale or a heightened ability for managers to capture more of the economic value created.

- Illiquidity – most alternatives tend to be less liquid than traditional investments. Sometimes it is by design (like the longer lock-up periods that accompany certain strategies, or the low turnover rates that accompany asset classes like Infrastructure or Farmland), and sometimes it is due to the lack of a liquid marketplace (ie. shares in privately held companies – although firms like Carta and the NASDAQ are trying to change this).

- Minimums – because of the lack of liquidity, higher costs, or regulation, alternative investments often have higher minimum investment levels.

- Regulation and LSD (leverage, shorting, derivatives): Regulation may also limit access to certain investor categories because of the perceived higher risk nature of certain investment instruments. For example, only recently have some regulators (like the CSA in Canada) relaxed restrictions on retail investor access to some alternative investment strategies.

- Access/Distribution – awareness, perception and reach are often the biggest things standing in the way of broader alternative investment adoption. Developing new and existing distribution channels (from direct-to-investor to advisor-wholesale) is often a sign an alternative investment category is picking up momentum.

Removing some of these barriers can help move an alternative further into traditional territory. Of course, beyond the underpinning and characteristics of the asset class or strategy, is investor comfort and behavior. Changing perceptions and behavior can take time, which can often act as a limiter on the rate of adoption. This is where seemingly mundane things like reporting, industry data, track records and marketing messaging can all become material contributors to the moving the industry forward. Each campaign and platform launch strengthens the cause.

Individual companies are also spearheading this effort. Since 2014, Yieldstreet has pushed its mission of expanding access to private market investment products through its product development efforts as well as its cultural presence, hiring actor Kal Penn as the front man in a nationwide ‘Private Market Investing 101’ campaign.

North of the border in Canada, while still pre-launch, Toronto-based Obsiido appears to be on a similar path, embarking on a mission to bring access to high quality alternative investments to individual investors.

NOTE: For some strategy-based alternatives, adoption presents a paradoxical situation. In some cases, size will be the enemy of performance. The more managers chasing a specific source of alpha or risk premia, the more likely it is to disappear. So for some alternatives, lack of adoption is not necessarily a bad thing.

Traditional: Reaching Maturity and Portfolio Staple Status

If the asset class or strategy is ultimately successful in its endeavor to extend its investor base, it may reach a point where it ceases to be an alternative any longer.

Traditional investments like stocks and bonds tend to be low-cost, liquid, broadly distributed, and widely accessible. In addition to these staples, other categories like REITs, gold, commodities and high yield bonds (which all used to fall in the alternatives bucket) have arguably reached a point of adoption, infrastructure development, liquidity and cost where they now fit the bill of ‘traditional’ investment status.

Today, the majority of savers in the economy use these traditional investment categories as the core of their portfolios: a diversified mix of stocks and bonds known as the 60/40 portfolio. Most investors live in this dual-asset class world and it has served them well over the past several decades. Unfortunately, there is reason to believe that the 60/40’s best days may be behind us.

Why Alternatives are Needed: The Case for Moving Down the Conveyor Belt

60/40 Structural Challenges

The growth of the 60/40 portfolio has come during a time of continuously falling interest rates. This has steadily driven bond prices higher while subsequently pushing investors further out on the risk curve producing great returns for both asset classes, but shrinking expected risk premia in the process.

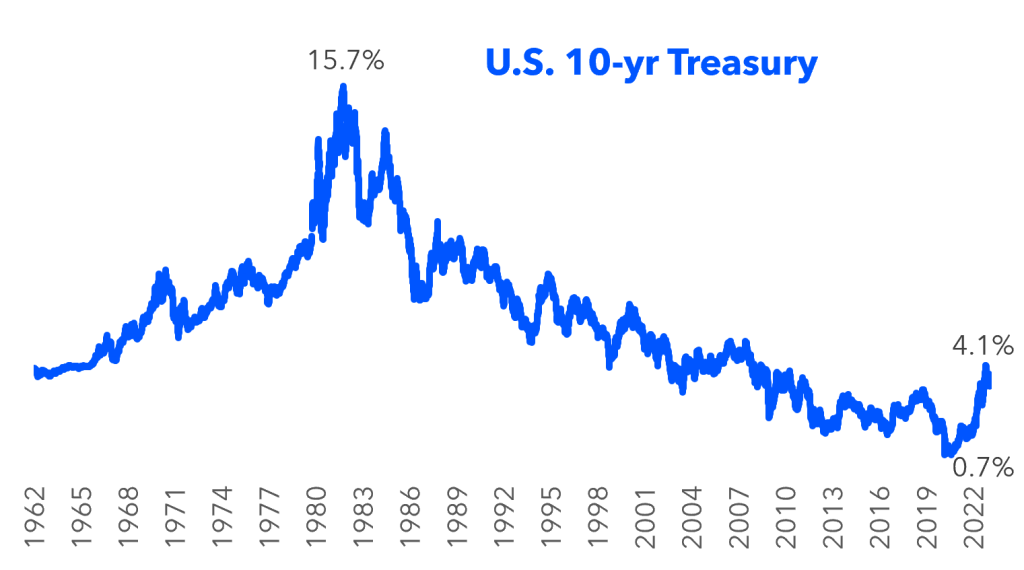

In addition, the bout of inflation we have been fighting since the onset of the pandemic has also potentially shifted the 60/40 dynamic. Elevated inflation can be a structurally challenging environment for stocks and bonds to thrive in, and what’s worse, inflation can potentially raise the correlation between the two asset classes, eliminating some of the strategy’s highly touted diversification benefits. There are no hard rules that say stocks and bonds must be uncorrelated. In fact, there have been several extended periods in history where the correlation between the two asset classes was positive (particularly during the inflation-ridden decade of the 1970s – see below).

In this new environment, a fresh source of diversification is needed, and this presents an incredible opportunity for alternative investments to shine.

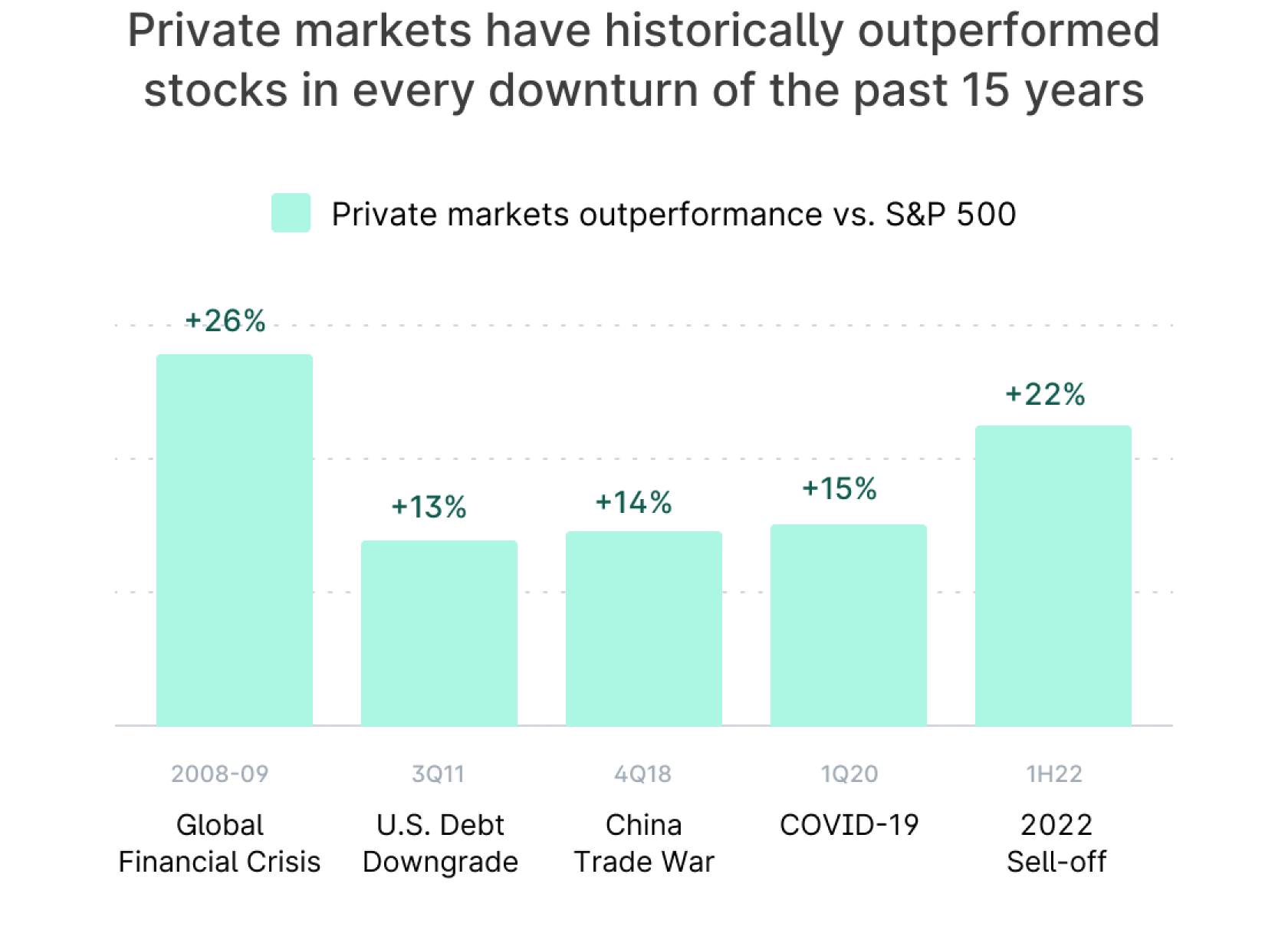

Returns Have Shifted to Private Markets

Outside of the macroenvironmental factors, there are other good reasons for thinking alternative investments may be on the precipice of broader adoption. For example, there is some evidence to support the idea that returns in recent decades have shifted from public markets to private markets, access to which continues to be out-of-reach for your average saver or mutual fund manager.

Airbnb went public last year, finishing its first day of trading a $86 billion valuation. That is $86 billion that accrued to those who invested while the company was private before public investors even had a chance to participate. Airbnb waited until it was a large mature company before considering an IPO: a trend many other large private companies seem to have followed.

While perhaps a little biased, our friends at Yieldstreet also showcase the benefits of private market investing on their homepage in the chart below:

A 2021 study by McKinsey also seems to confirm this to be the case:

On a pooled basis, private equity has produced a 14.3% annualized return over the trailing ten-year period, beating the S&P 500 return of 13.8% by 50 basis points.

With more returns accruing to areas outside of the reach of the 60/40, access to private markets and other alternative categories will be important for the average saver to keep pace.

Retirement Burdens Have Shifted to the Individual

With the disappearance of defined benefit pension plans and underfunded social savings/retirement programs in developed markets, the burden of saving for retirement has shifted from institutions to the individual. With individuals more responsible than ever for their own financial security, the fact that your average saver still does not have easy access to the return profiles of most alternative investments is an issue (if that is indeed where all the returns are).

We also tend to shield non-accredited and non-qualified individual investors from certain illiquid alternative investment opportunities. While that may be great from a consumer protection perspective, it also keeps the average investor away from earning a liquidity risk premium. But why? Illiquidity (and the associated long holding period) is duration matched to their retirement objectives. We don’t want people touching those assets anyway. Ironically, illiquid assets could be great products for retirement accounts, they just need the right packaging and protections in place.

Opportunities like helping retirement-oriented investors capture a liquidity risk premium are arising everywhere across the alternative investment landscape. Many are due to structural issues that can now be alleviated through the right technology/approach. Others are emerging due to constantly evolving industry dynamics. Whatever the case, there has never been a better time to take a look into the world that exists beyond stocks and bonds.

That is not to say that 100% allocation to alternative investments is a good idea. Somewhere between that and the 0% allocation in most 60/40 portfolios lies a sweet spot where the benefits of capturing uncorrelated risk premia can accrue to the average investor.

Is Alternative Still the Right Term?

New investment exposures are born every day. Some will make it to wear the alternatives label. Fewer still will make it into the mainstream. But what this tells us is that there is movement in finance. The industry is not static, it is dynamic, with a pace of change that appears to be accelerating everyday.

Like technology companies shedding the ‘technology company’ label, once an alternative investment becomes mainstream, the ‘alternative investment’ label may no longer be appropriate. We can thank the conveyor belt of finance for this.

6 responses to “The Conveyor Belt of Finance and the Evolution of Alternative Investments”

[…] diversification in the past will provide the same benefit in the future. This is why exploring the Conveyor Belt of Finance (alternative investments) is so important. We must diversify our […]

LikeLike

[…] dimension (except human behavior). One aspect of that is nicely visualized by Brett McDonald in a posting on his site, Paper & Blocks. What is “emerging” today may someday become […]

LikeLike

[…] fintech financialization forces are what make the conveyor belt of finance churn, transporting asset classes through a maturity cycle from emerging to […]

LikeLike

[…] fintech financialization forces are what make the conveyor belt of finance churn, transporting asset classes through a maturity cycle from emerging to […]

LikeLike

[…] fintech financialization forces are what make the conveyor belt of finance churn, transporting asset classes through a maturity cycle from emerging to […]

LikeLike

[…] fintech financialization forces are what make the conveyor belt of finance churn, transporting asset classes through a maturity cycle from emerging to […]

LikeLike