ESG is one of the most discussed topics in investment management today.

If you do a tour of the industry’s largest conferences in 2023, that three letter acronym—which stands for environmental, social, and (corporate) governance, btw—is likely to appear on each event’s agenda multiple times.

Sustainable investing is #trending and almost every major asset manager has hopped on board. And why not! ESG is good for business and good for the world. It is an incredibly important lever in tackling some of the most pressing global systemic issues, it has produced above average market performance over the past decade, and it aligns with investor appetite for solutions that go beyond investment returns to positively impact the world.

ESG fund sales are ramping up as product development has accelerated across the industry over the past couple of years.

Yet, ESG investment funds still make up a very small portion of total industry assets (see below). Long-term ESG mutual fund and ETF assets in the U.S. reached $400 billion according to ISS Market Intelligence. By contrast, the investment fund industry in the U.S. totals $34.8 trillion, meaning ESG investment funds represent ~1.1% of industry assets under management (AUM). This number was slightly higher in Canada, at roughly 1.4% of total industry AUM.

Retail investors do not seem to be making major adjustments to their allocations and advisors seem to be content with the status quo as well.

Change is hard—a sentiment anyone in the business of responsible investing will likely echo.

But change is coming. ESG is currently caught in the crosshairs of a broader shift taking place in investment management: A regime change that displaces the profit- and return-maximization of the ‘shareholder era’, and opts for the personalization and preference maximization of the ‘stakeholder era’.

This essay aims to explain the change that is taking place and ESG investing’s role within it. First, however, we need to begin the discussion with why the case for responsible investing is perceived to be so compelling.

Also note that while there are admittedly differences, the terms ‘ESG investing‘, ‘Sustainable Investing‘ and ‘Responsible Investing‘ will be used interchangeably throughout the discussion.

The Case for ESG Investing

If you need a reminder ‘why’ ESG investing should be considered as part of your portfolio, simply turn on the news. Spend an hour with a six o’clock newscast, and you’ll receive a stark reminder of the major global challenges we face: war, famine, inequality, climate change, biodiversity, human rights, and good ol’ fashioned fraud (thanks for the reminder FTX). These issues create the collective obstacle we face as a society in building better futures for ourselves and for the generations that come after us.

Yet, there are a number of different levers society has to combat these issues, from politics to philanthropy to simple education. One lever stands out as particularly important: capital.

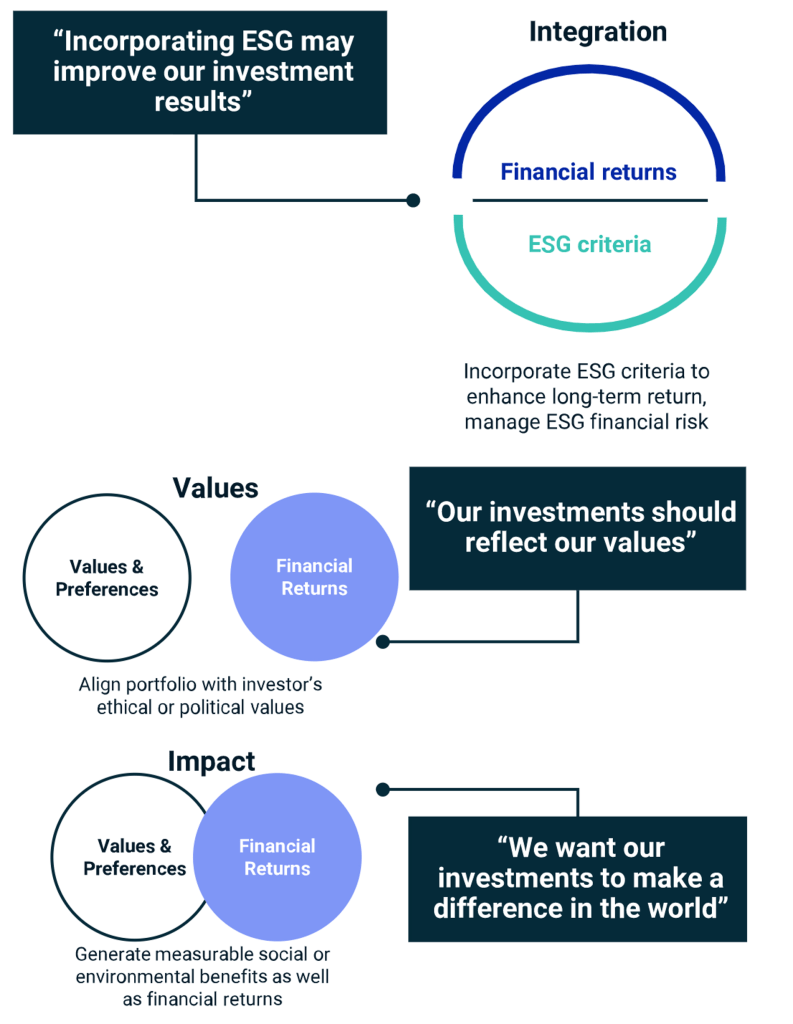

The discipline of investing is about the allocation of capital in the economy. Responsible investing is about how ESG factors can come together with financial factors to create an investment process that can drive both positive financial and societal outcomes. The best of both worlds!

The primary drivers in this narrative are:

Collective Influence through the Cost of Capital: The logic that drives ESG investing is simple: allocate capital to projects that have positive financial and societal impacts and away from projects that may not. It is hard to see the direct impact of an individual investment here, but like voting in an election, it is the collective voice that has power. Investors vote with their dollars to influence the cost of capital for individual companies. The more demand for a project, the cheaper the cost of financing and the more likely it is to move ahead. On the other hand, should investors limit the dollars flowing to a company/project, even in the secondary market, share prices can fall, driving up the cost of capital for any new financing. This is how ESG makes an impact through the invisible hand of the market, and although it is hardest to see, it is collectively the most powerful.

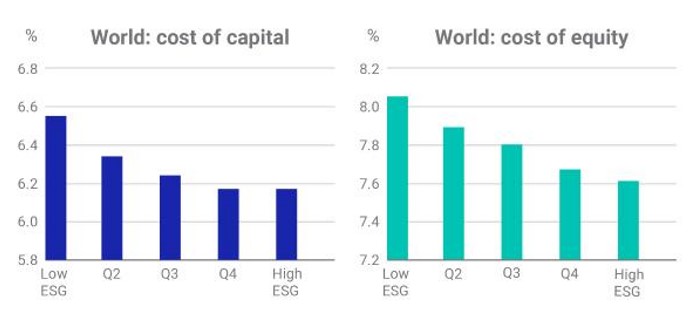

Enhancing Long-Term Risk-adjusted Returns: There is a common myth that in responsible investing, there is a trade off between impact and performance. That is, those who invest responsibly are sacrificing investment returns for the greater good. Of course, this myth is as unproven as the idea that responsible investing will produce outperformance through the systematic inclusion of ESG risks and opportunities into a portfolio. The truth is, we probably do not have enough [good] data to say one way or the other (we’re still trying to figure out the value factor for heaven’s sake). However, thanks to a heavy lean to the technology sector, most ESG funds have performed relatively well against non-ESG peers over the past five years. In addition, an increasing number of investors and asset managers are looking at societal issues as investment-specific risks. For example, Larry Fink kicked this off by making the case in his 2020 Letter to CEOs that climate risks ARE investment risks and that they will lead to a profound reassessment of asset values in the years ahead. Whether underperforming or outperforming, taking ESG factors into account is an active management decision, and like all decisions in the pursuit of higher returns, there appears to be a growing crowd looking at responsible investing as an opportunity to outperform.

Personal Values Alignment: Perhaps the most straight forward driver is the fact that people want to feel good about the decisions they make. They want alignment with their moral values and beliefs. Just like how most people will choose to throw an empty bottle in a blue recycle bin over black trash can for sustainability reasons, most people would prefer to say they invest in renewable energy companies over fossil fuels, or organic food stocks over tobacco companies, all based on the externalities they create in the world.

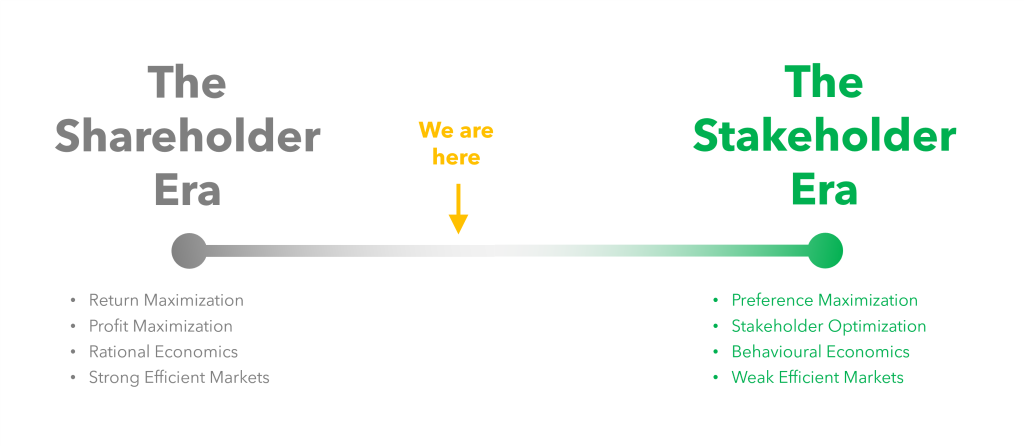

A Regime Change is Underway

Responsible investing is one of the first ways non-financial factors are beginning to be included alongside financial factors when making investment decisions. ESG is leading the way through a broader shift taking place in markets. We can refer to this as a shift from the rational profit-maximizing approach that characterized the ‘Shareholder Era’ to the personalized preference maximization that characterizes the ‘Stakeholder Era’.

All that mattered in the Shareholder Era was returns. Profit maximization ruled the day and its pursuit was supported by widely accepted, yet somewhat dated, economic theories:

- Shareholder theory (1970s): Suggests the only duty of a corporation is to maximize the profits accruing to its shareholders.

- Efficient markets hypothesis—strong form (1960s): All public and private information is completely accounted for in current stock prices suggesting investors will be challenged to obtain returns on investments that exceed normal market returns.

- Classical economic theory and the rational economic man (1800s): The assumption of perfect information and rationality in the decisions of economic agents (consumers and corporations) upon which most of classical economic theory is based.

Tying the theories together you can see that economic decisions were assumed to be made with perfect rationality, so capital will be allocated to projects that have the greatest financial returns, and markets operate with near perfect efficiency leaving no reason to deviate from a portfolio that is along the efficient frontier of risk-reward. Non-financial factors like ESG had no business finding their way into investment decisions in this era—they did not make sense against the era’s prevailing economic theories. But that is changing…

Where the shareholder era focused on return maximization, the Stakeholder Era focuses on preference maximization. It is the era of personalization and it is largely complemented by a more modern set of economic ideas:

- Stakeholder theory: Suggests a company is only successful when it delivers value to its stakeholders (shareholders, employees, customers, communities, etc.), and those values can come in many forms beyond tangible or financial benefits.

- Efficient markets hypothesis—weak form: Today’s stock prices reflect all the data of past prices, but above average returns can be found through the information advantages obtained through fundamental analysis.

- Behavioral economics and recognizing irrationality in decision-making: The effects of psychological, cognitive, emotional, cultural and social factors limit the bounds of rational decision making for economic actors like consumers and corporations.

Bringing the theories together, one could see that individuals are not rational profit maximizers, but rather human beings that are subject to numerous non-quantitative and non-financial influences in their decision making. In this domain, stepping outside the traditional bounds of rationality to include non-financial factors in investment analysis makes complete sense. Furthermore, these theories allow for the possibility that pockets of mispricing may still exist. Therefore, bringing ESG factors into the investment decision-making process not only offers a way to benefit all stakeholder groups (beyond just shareholders), but also offers a potential path to achieve robust risk-adjusted returns.

Pushing Toward Personalization

ESG is the first big step toward incorporating personal values, a non-financial factor, into asset management decisions.

This also highlights ESG’s biggest challenge. Personal values are exactly that: PERSONAL. They differ for every individual.

When we ask people to align their investment portfolios with their personal values, that could mean any number of things. Some people care explicitly about climate change while others wish to abolish societal inequalities. Some people wish to abstain from investing in vice stocks like alcohol or gambling while others build those activities into their lifestyles and have no problem with them in their portfolios. Just look at the variety contained within the UN’s Sustainable Development Goals and the challenge of prioritization and focus becomes clear.

Given that personal values are varied, every investor is going to have a slightly different set of wants and needs when it comes to building these non-financial factors into their portfolios. If the investment account is going to become an effective tool to create societal change, then it needs to overcome a major structural hurdle which is the idea of serving ‘personal needs’ through ‘standardized’ vehicles.

The dominant investment vehicle serving individual investors today is the investment fund. Whether structured as a mutual fund, ETF, or some other alternative, funds have been an effective way to pool investor capital together to get the benefits of scale needed to hire professional managers to make decisions on the investors’ behalf. The challenge with funds, however, is that they can only go so far in meeting personal needs. They are fantastic as a starting point, but they are likely not the end game.

Thanks to the relentless pace of technology and innovation, personalization comes for every industry, and now, it is asset management’s turn. Netflix knows what shows you want to watch. Amazon knows what items you want to buy. And soon, your asset manager will know what securities you want to invest in.

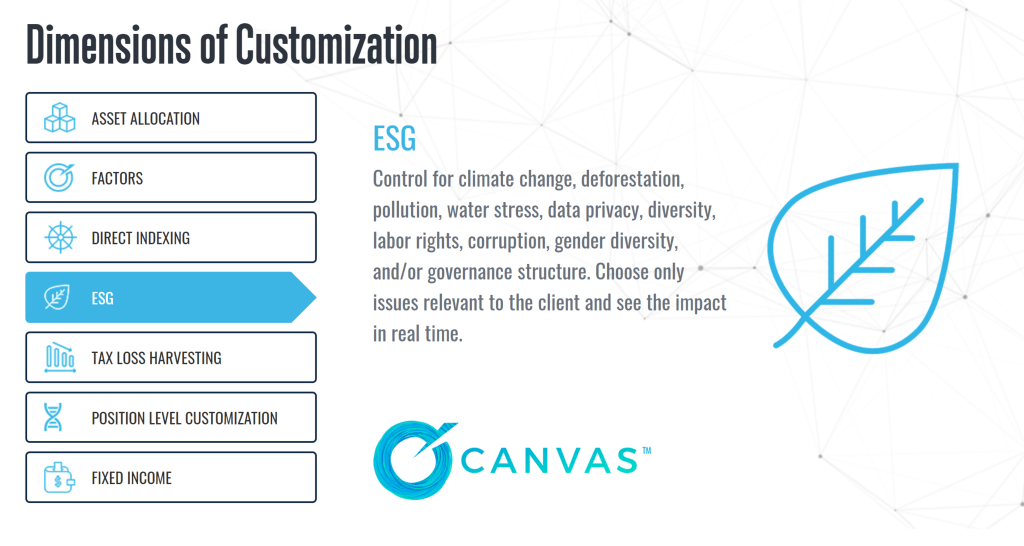

Powered by fractional shares, rapidly declining trading costs, and discretionary managed account structures, the future of personalization in asset management likely looks somewhat like OSAM’s Canvas platform. The platform can incorporate a variety of individual factors that include: asset allocation, taxes, concentrated security positions, sector preferences, and a bevy of ESG factors as in the image below.

It’s Not All Sunshine and Rainbows

Personalized separately managed accounts are an ESG investors dream. They provide the flexibility required to meet individual investor needs in the stakeholder era.

But this brings up a counterpoint: not every investor wants to incorporate ESG factors into their personal portfolio. In fact, a variety of valid criticisms exist when it comes to the current ESG investment landscape.

- Greenwashing: Companies who spend more resources on communicating and marketing their ESG good deeds, instead of actually making an impact.

- One-size fits all approach: The current approach and investment vehicles are overly broad (particularly negative screening strategies) which water down their impact.

- Lack of a consistent definition: While some standards exist, like SASB’s Materiality Map, a common definition for ESG, sustainable and/or responsible investing is hard to find, creating both consumer confusion and brand dilution.

- Unproven risk-return profile: Lacking definition and data, it has also been challenging to establish a track-record for the ESG space as a whole and consequently has been challenging to prove over or underperformance.

- Higher cost perception: There is a perception that ESG strategies tend to be higher cost. You can find studies that support that idea, like this one linked here which say ESG Funds are 40% more expensive than their traditional counterparts. You can find data to support the opposite conclusion. Using data from Morningstar, as of Dec. 31, 2021, average management expense ratios for sustainable funds were lower in the equity and fixed-income categories than for non-sustainable funds.

- Skewed investor incentive structures: Investors may be more likely to hold on to underperforming investments because of the perception that they are still doing good in the world.

More recently, the issue has also been politicized as a way to pushback against the ‘woke agenda’. The most recent example comes from Florida Governor Ron DeSantis who released new details about his plan to require state and local government investments only be guided on potential returns, requiring the state’s asset managers to stop using ESG investing strategies if they want to keep overseeing Florida’s money. This has proven to be a broad issue in the U.S., now spanning multiple states (see below).

Change is Hard

One of the other challenges in the responsible investing world that has also been plaguing market researchers for decades is something known as the intention-behaviour gap.

The intention-behaviour gap is the reason we fall short of the things we are meaning to do: saving money, staying fit, and getting out to vote are all good examples of paths people wish to take, but end up failing to perform the necessary actions.

When it comes to socially responsible investing, an intention-behaviour gap also exists:

According to the most recent Responsible Investment Association (RIA) Investor Opinion Survey, 73% of Canadian investors are interested in responsible investing, but only 31% of respondents said they own investments that account for environmental, social and governance (ESG) factors.

This is not all attributable to the end investor. Also from the RIA survey, when asked has your financial advisor or financial institution ever asked if you are interested in responsible investments that are aligned with your values, only 27% of respondents said “yes”. This suggests a ‘service gap’ also exists in the ESG investment industry, where advisors and/or the companies that employ them are not bringing responsible investment products to the forefront of client conversations. The reasons are varied (as per this Investment Executive article):

- “It’s great, but I still feel like it’s a fad”

- “I wait for [clients] to bring it up because I see my job as making them money”

- “Clients are asking about it, but the options aren’t as good as I’d like them to be”

- “A lot of my clients are older and they don’t care quite as much. But as I onboard the kids, it’s becoming more important”

- “Product mandates and terminology are “confusing” and ESG products charge higher management fees”

Bridging the ESG Gap

Closing the gap will require some heavy lifting from the investment industry. The COM-B Model, a popular behaviour change framework, provides a nice organizing framework for potential paths to progress:

Although there are many things to be done that can help create some urgency around the topic, the biggest factor in making progress on the ESG front is simply TIME. There is an incredible amount of inertia in the asset management industry and major changes happen at a slow pace (just look at how long it has taken ETFs to reach the levels they are at today, which still puts them well under half the size of mutual fund AUM). The best we can do is introduce the concepts to investors and advisors in the near-term; continue to develop the infrastructure and narratives required to support responsible investing; and continue to build, launch, and evolve products to incorporate ESG factors into their decision-making processes.

One Step at a Time

The fact that there is disagreement and discourse around ESG only serves to drive home the point that personal values are indeed varied and personal. Platforms like Canvas give people a way to either opt-in or opt-out. Unfortunately, personalized separately managed accounts for all investors is not going to be a reality anytime soon.

Change isn’t easy. Baby steps are required before any major leaps can take place.

For ESG investing, in the Stakeholder Era, on the path to personalization, introducing responsible investment funds to a broader set of the population is the best first step.

We might not be able to perfectly align everyone’s personal values to their portfolios overnight, but building comfort with the idea that capital is one of the primary tools we have to tackle society’s biggest challenges is a worthy point of progress to make in an industry that has been rooted in past ideals for perhaps a little too long.

It appears the shift from Shareholder to Stakeholder is well underway!