[Update: This post was originally written on November 1st, ten days before FTX filed for bankruptcy. Subsequent to the fallout, the Canadian Securities Administrators (CSA) strengthened its approach to oversight of crypto trading platforms by expanding existing requirements for platforms operating in Canada. This included strong words for unregistered trading platforms (including those located outside of Canada) that have not filed a pre-registration undertaking, expanded terms and conditions around custody and asset segregation, and a prohibition on offering margin to clients. While there will always be a balancing act between protection and innovation, for now, the pendulum has clearly swung in the direction of protecting consumers. It will now be incumbent upon industry participants to implement a compliant operating model, bear the costs of doing so, and prove that crypto is a sustainable asset class and a financial innovation worth nurturing.]

Something is brewing in Canada’s online brokerage industry… and that something, is crypto.

In my past professional life, I was a market analyst and consultant covering the online brokerage domain, so I continue to follow these developments with interest.

Crypto had been a discussion topic in industry circles going back to 2016-17. To me, crypto was captivating to watch. 2008 was the birth of a new type of asset, one that was digitally scarce, now in both fungible and non-fungible form factors, that operated outside the bounds of the traditional financial system.

An entirely new set of infrastructure had to be developed to create financial services for the crypto world. The industry that was developing literally had to build a parallel financial system. There were crypto trading venues separate from traditional equity trading venues (like the NYSE, NASDAQ, and TSX). There were crypto payment gateways separate from traditional payment gateways (like Global Payments and Stripe). There were even crypto index providers separate from traditional industry index builders (like MSCI or S&P).

The crypto world has been building itself from the ground up and has largely been kept separate from the rest of the financial services industry. However, there is evidence the two are starting to come together:

Coinsquare, Canada’s longest operating crypto asset trading platform, today announced that the Investment Industry Regulatory Organization of Canada (IIROC) has approved Coinsquare’s dealer registration and IIROC membership. This regulatory status will now position Coinsquare as the first crypto-only, IIROC registered investment dealer and marketplace member in the Canadian market across all provinces and territories.

–GlobeNewswire

This followed similar news from two weeks earlier:

Bitbuy today announced its partnership with Alpaca which will enable Bitbuy to offer its users fractional trading and investing in thousands of US stocks and exchange traded funds (ETFs), in an integrated experience within the existing Bitbuy platform. Bitbuy will utilize Alpaca’s Broker API which will provide Bitbuy customers with real-time fractional trading and instant settlement. Bitbuy stock trading will be offered in conjunction with Alpaca and brokerage services through a leading Canadian investment bank and IIROC member.

–Newsfile

Which followed a wave of postings on job boards like this:

As a Senior Business Analyst, Crypto Trading at Questrade, you will communicate with multiple stakeholders to elicit, define, analyze and document requirements for our cutting-edge crypto product development…

These are big milestones. Coinsquare has officially become a crypto-only IIROC dealer. BitBuy has partnered with a stock-trading API company to offer equity trading in 2023. Questrade is clearly exploring the option of launching crypto trading. Of course, all of these firms are building on a regulatory path paved by Wealthsimple, who became the first regulated crypto platform in Canada [in 2020] after receiving exemptive relief from certain regulatory obligations through the Canadian Securities Administrators’ (CSA’s) sandbox.

With crypto converging toward the traditional brokerage business, and online brokers moving to add crypto, the two [once separate worlds] are now on a collision course.

Drawing Industry Boundaries

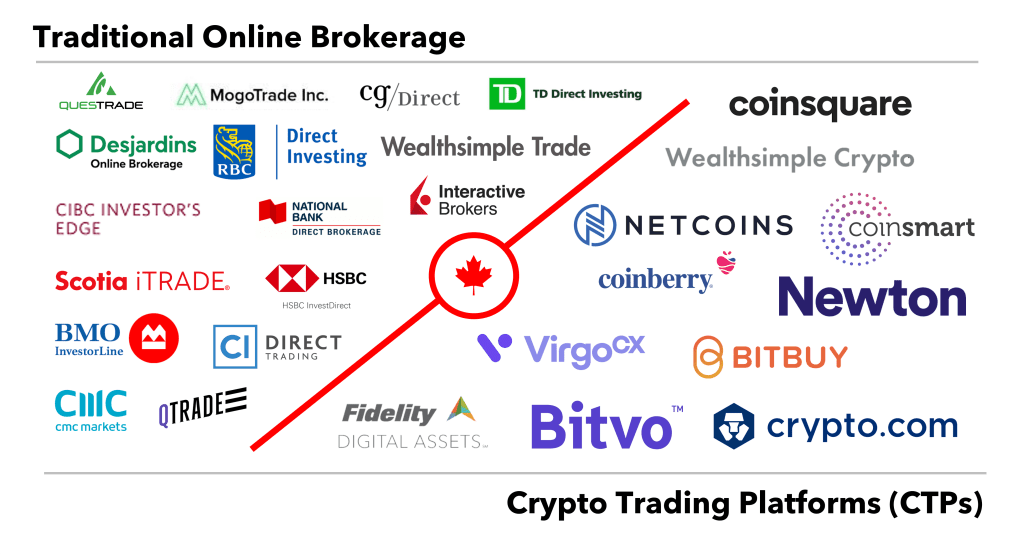

What defines the online brokerage industry? Canadian regulators might argue that it is a dealer’s order execution only exemptive (OEO) relief from suitability requirements. Given that criteria, there are about ~16 retail facing dealers in Canada that currently operate under this exemption (see below).

A less formal and more product-centric definition would suggest the business is defined by the ability to offer customers access to securities markets, the opportunity to invest or speculate in those markets, and safe custody of assets held and traded.

In this definition, crypto would in fact be a part of the online brokerage world based on guidance provided in a 2021 paper released by the CSA. Unlike the U.S. market, where there is heated debate over which cryptoassets constitute securities, in Canada, the guidance is much clearer. The regulators assume that when you trade cryptoassets on an exchange, you are not trading the asset itself, but rather a claim to that asset that constitutes a ‘crypto contract’. This ‘contract’ is considered a security under Canadian regulations, even if the underlying cryptoasset is not.

*A short disclaimer here that I am NOT a lawyer and none of this is legal advice, just a casual observer’s impressions of industry developments.

Without being comprehensive, roughly a dozen companies in Canada appear to actively and openly serve Canadians with crypto trading services (see below).

Given that most crypto trading platforms that have emerged in Canada follow the product-centric definition above—they provide access to crypto markets, the opportunity to invest or speculate in crypto, and act (or find a third party to act) as custodian—it is little wonder the two previously separate industries are merging together.

Path Dependency

With crypto teed up as the next step in the online brokerage industry’s evolution, the result will be a shift in the competitive dynamic.

To understand how, it is helpful to recognize an enduring truth about the evolution of industries: the way an industry evolves is path-dependent. That is, history matters: What has occurred in the past will influence what is to occur in the future.

The online brokerage industry’s evolution was heavily influenced by:

- industry structure which pitted big banks against monoline independent firms

- shifts in the macroenvironment including market booms that attracted waves of retail traders, and market busts that scared them all away

- the decisions of individual industry participants which included strategic M&A and product development trial-and-error.

Those three factors created a web of complexity that knocked industry dynamics around and created a high degree of uncertainty in plotting expected strategic outcomes. As crypto looms, understanding the road the online brokerage industry has taken to get to this point is informative for understanding what comes next.

Lessons from History

The online brokerage business grew out of the former discount brokerage industry, which was popular in the 1980s as a telephone-based alternative to more expensive full-service options. As the 1990s rolled around, the internet came on the scene and slowly shifted discount brokerage businesses online. Then came the tech bubble, the introduction of social media, the 2008 financial crisis, the explosion of mobile phones, the pandemic trading boom… and before you knew it, there were over 10 million online brokerage accounts in Canada.

1-Canada is a Unique Market… and It is Hard to Compete with the Big Six Banks

Depending on how you measure the industry, the Big Six banks in Canada hold roughly 60% of Canadian retail investable assets. This figure is actually much higher in the online brokerage world, where market shares are concentrated in the bank-owned platforms: BMO InvestorLine, CIBC Investor’s Edge, National Bank Direct Brokerage, Scotia iTRADE, RBC Direct Investing, and TD Direct Investing.

Their competitive advantage comes down to brand and customer acquisition funnels. To state it simply, Canadian banks earned a lot of goodwill by managing risk well during the 2008 financial crisis, and they have not stumbled much since. There is a high degree of trust built up in each of their brands and they have earned the default position in the wallets of most Canadians.

Even more challenging to contend with, the banks are able to service nearly all financial needs across the spend-save-borrow-invest-protect continuum of products. Each of those individual product areas act as their own marketing funnel, bringing new clients to the bank. From there, the banks are relationship-deepening experts, from traditional cross-selling methods to powerful incentives that sway people toward the convenience of having a ‘one-stop shop’ for all their financial needs.

This customer acquisition funnel is hard to compete with as a monoline online brokerage business. It is much easier to mine a large database of banking customers for new clients and convert warm leads than it is to approach prospective clients from a cold start.

The Canadian market has been notoriously challenging for foreign competition to enter as well. For example, U.S. behemoth Schwab, without exaggeration, ‘invented’ the online brokerage industry in the 1980s (chronicled well here in Charles Schwab’s biography, Invested: Changing Forever the Way Americans Invest). Likely unknown to most Canadians, Schwab also had a Canadian arm, but was unable to keep it afloat, selling it in 2002 to Scotiabank. E*TRADE, now owned by Morgan Stanley, also had a Canadian arm. The E*TRADE baby commercials once graced Canadian television. But even the genius marketing was not enough, as E*TRADE Canada was sold to Scotiabank in 2008. Other U.S. giants never really tried to get in the door. Fidelity chose to service institutional clients with Fidelity Clearing Canada, but stayed away from the more formidable retail side of the industry. Interactive Brokers was perhaps the only firm to successfully stick the landing in Canada, thanks to their advanced trading features that were unmatched by most others in the market.

Start-ups have also had a challenging time penetrating the bank’s armour. Questrade, Qtrade, and VirtualBrokers (now CI Direct Trading) can hardly be called start-ups at this point with operating histories stretching back nearly 20 years. Their strategies have typically leaned toward price-leadership, with commission rates well below the industry average, and product-leadership in the features and support built into their trading platforms. While they have collectively gathered client assets in the $10’s of billions, it still falls an order of magnitude short of the $100s of billions held at the Big Six. To give credit where credit is due, the launch and subsequent success of Wealthsimple Trade has been one of the first examples of anyone in the space outcompeting the Big Six in recent memory.

Lesson 1: To beat the banks, be distinct from the banks

Given that many have tried and failed, the more you look like the banks, the less chance you have to compete with them.

A start-up in this space is like David taking on six Goliaths. Ironically, the chink in the armour of the banks is what has kept them on top for all these years: strong risk management and heightened risk aversion. While the standard risks of a financial institution (credit, liquidity, operational) are par for the course, there is one type of risk that most firms will not bear: reputational risk. Anything that threatens the trust and goodwill built into the Big Six brands over the preceding decades will not be tolerated, and crypto, arguably still falls in that bucket.

Unfortunately, Overton Windows tend to shift, and eventually the ability to gain investment exposure to cryptoassets will fall into mainstream public acceptance. In fact, you could argue certain cryptoassets, Bitcoin and Ether, are practically there already. In other words, they have become (or will soon become) strategic beta and there is little doubt that the largest online brokerage players today will eventually add crypto trading to their platforms.

To be different in this industry, firms must find strategic alpha, which by definition means embracing ideas that are off the rational strategic path. They need to stay on the leading edge of the crypto Overton Window and double down on the things that separate crypto from the traditional industry. In general, those stem from the characteristics of cryptoassets themselves: liquid, decentralized, permissionless, composable, and digitally scarce.

Composability, in particular, is a key characteristic of crypto networks that has allowed for a variety of financial innovation to occur. Beyond the Overton Window lies staking, yield products, access to the DeFi ecosystem, collectibles, gaming, and still-to-be-discovered use cases. Staying at the edge of the window will allow firms to remain distinct from their formidable bank competitors (who are too risk-averse to go there) and will continue to drive new web3 products and services safely [under a regulated banner] into the hands of Canadians.

2-The Industry is Cyclical, so Find Revenue Streams that are NOT

Most people would be surprised to learn that commissions are NOT the primary revenue generator for Canadian online brokerages. People from the U.S. would be even more surprised that the controversial practice of receiving payment for order flow (PFOF) is also a relative non-contributor. In fact, PFOF is almost non-existent in the Canadian landscape thanks to structural differences in our equity markets.

The primary money maker for Canadian online brokers is the interest income they earn on the cash balances clients keep with them. Net interest income (spread on cash plus margin lending) makes up over half of the revenue generated in the industry. Commission revenue comes in second place. Foreign exchange commissions and service fees round out the rest of the podium.

While the proportion of each revenue category may be unexpected, the absence of certain revenue lines that are present in other geographies may be even more surprising.

In addition to the aforementioned absence of PFOF, securities lending revenue is also AWOL in Canada with only a few firms offering programs that let clients lend out the securities they hold (mostly to short sellers that want to borrow) in order to share in some extra interest revenue. Managed asset fees, a major contributor in the U.S. to the bottom lines of industry leaders like Schwab and Fidelity, are also non-existent in Canada thanks to the strict separation of online brokerage and advice as a result of the OEO structure. One exception to the rule is BMO InvestorLine’s adviceDirect program and the separate and distinct robo-advice entities (from RBC InvestEase to Wealthsimple Invest) that pair up with their corresponding online brokerage businesses. It is also noteworthy to mention the industry recently lost one of its major revenue sources after investment fund trailer fees were banned by the CSA for OEO dealers.

What becomes clear from the above is that the revenue mix in the Canadian landscape is diverse. However, things were not always this way… As the industry evolved throughout the 1990s and 2000s, commission revenue was the primary revenue driver. This was partially due to the fact that other revenue streams were underdeveloped, but was more so the result of high commission rates, upwards of $20-$50 per trade.

Through that period, while revenue was flowing and the times seemed good, under the surface, it was anything but. The industry was largely captive to the moods of Mr. Market. When he was happy, like during the 1990s bubble in technology stocks, bottom-lines widened, dollars were reinvested back into product development, and the industry expanded. But when Mr. Market turned sour, margins thinned, dollars and product development dried up, and the industry contracted. This was a volatile way to live, and it put a lot of jobs and even some start-up ventures at risk.

The volatility was a direct result of the revenue mix in the industry, which can be categorized into two big buckets:

- Transaction-driven revenue: Commissions, Foreign Exchange Fees, Service Fees, PFOF

- Relationship-driven revenue: Net Interest Income, Account Fees, Managed Asset Fees

Transaction-driven revenue is tied to activity levels in the industry. If investors stop trading or turn away from markets, these revenue streams tend to dry up. Relationship-driven revenue on the other hand, is much stickier. It tends to persist through market downdrafts, although it is impacted by a separate set of influences.

Over time, as a result of both price competition and some deliberate posturing, the proportion of transaction-driven revenue decreased and the proportion of relationship-driven revenue grew. This had the impact of both diversifying the industry’s risk exposures and stabilizing the revenue base, making the business much more sustainable over the long-term.

Lesson Two: Revenue diversity is key to staying afloat in an incredibly volatile industry

It is true, placing a bet on transaction-driven revenue will make the highs feel higher… but it will also make the lows feel MUCH lower. Diversifying revenue streams can be a deliberate act. Other times, firms will have no choice but to accept the industry default.

As crypto enters the online brokerage arena, there are a variety of formats through which firms currently make money, but nearly all of which today fall into the transaction-driven revenue category.

Commissions are often priced as a percentage of dollar trading volume (eg. 0.1%-2.0% fee per transaction) versus the flat dollar amount (eg. $9.95) that is common in the retail equities business. That fact should make a lot of online brokerage industry executives jealous since it a much more profitable commission format. That pricing will eventually come down, just as price competition has driven equity commission rates toward the $0 threshold. Although it may take longer than expected.

As that happens, other revenue streams will become more important, something that start-ups in the space would be wise to consider ahead of time. DeFi and Solana summers may be fun, but revenue diversification is what will help firms survive the crypto winters ahead.

3-There is Little Product Differentiation if Your Product is a Trading Platform

Online trading platforms started to emerge in the 1990s as online brokerage became the primary form factor for discount brokers. Since then, 30+ years of evolution has significantly elevated the trading experience for retail investors. Today’s modern trading platforms have taken the tools and information once available only to institutional investors and have brought them into the retail sphere. One click order entry, high functioning watchlists, extensive charting tools and capabilities, order book analytics, voluminous market data/news/research, and all of it often wrapped in a customizable user interface.

While there is continuous work trying to keep the platform modern and up-to-date, the product development train has started to slow with most of the obvious features now table stakes in most online brokerage offerings. This is an early sign that the industry as a whole is starting to approach the ‘mature’ stage of the industry lifecycle. In this phase, price competition tends to rule above all else as product features become commodified.

This was most evident in the flight to $0 commissions that swept the U.S. online brokerage market in 2019. Schwab kicked off the price war, reducing $4.95 commissions to zero, eventually forcing the hands of TD Ameritrade, Fidelity and E*TRADE to follow suit. This was also a bold move by Schwab, who knocked billions of dollars of market cap off the industry that week, only to swoop in and scoop up TD Ameritrade in a blockbuster acquisition for $26 billion.

Price competition can be fickle. It is typically a zero-sum game for the industry where the client is the one that comes out ahead. Those who put pricing front and center in their value propositions in the past often only attracted the industry’s most price sensitive customers. While a short-term client acquisition boost was typically the result, it usually would not last long. If a client came for the price, they were just as likely to leave for a better price when one inevitably came along.

Feature competition in the industry also followed a similar logic. As incremental features were released by one competitor, if deemed material, they were immediately copied and integrated by the rest of the field. Consequently, the platforms and features of most online brokers eventually converged together, to a useful, albeit undifferentiated, middle.

Lesson Three: Features will only get you so far. Sustaining advantages will not be found in the trading platforms themselves, but rather in building an early lead and maintaining it over time.

If a firm is planning on differentiating through their trading platform, it will not be a long-term competitive advantage. All of the low hanging fruit will be quickly plucked and eventually any sustaining innovation will be copy and pasted by everyone else in the industry. As already mentioned, product differentiators will come from outside the Overton Window, along with the recognition that they will ultimately be copied further down the road.

However, the discussion about the long-term must be separated from the short-term.

The most important lesson industry history can teach us is that building an early lead can be translated into a sustaining advantage through branding and switching costs as the industry matures (as per Hamilton Helmer’s 7 Powers framework).

In fact, today’s industry leader, TD Direct Investing, built their lead in the 1990s and 2000s by allocating more investment and attention into their online brokerage business than anyone else in the industry. In the early 2000s, when most of the other Big Six firms were busy focusing on making acquisitions, building out their full-service brokerage arms and expanding their in-branch financial planning businesses, TD was busy investing in its online platform. For a lengthy period, TD was the only firm to direct clients in their branches to invest online. At the other Big Six, you would be kindly triaged into either their planning, full-service brokerage, or private investment counsel channels. Directing clients to online channels was seen as taboo, counter to the belief that the branch is what anchored client relationships. This allowed TD to build up a lead that they have yet to relinquish and it has been sustained by continued trust in the TD brand as well as the wall of switching costs that currently sit in front of existing customers.

Back to today, the market for crypto investment exposure continues to grow as general public awareness and comfort increase. This is industry white space and there is a ‘land grab’ about to take place. Those who are fastest in this race may gain an advantage in the long-term, much like TD did back in the 1990s.

To gain the lead is one thing, to not let it go is another. Those who are successful in the current wave of crypto customer acquisition will be wise to think about how to maintain their lead, either through branding or switching costs. One of the other 7 Powers, network effects, also presents an opportunity that has yet to be explored in the online brokerage space. Effective networks have been built by adjacent firms like StockTwits and are being worked on by start-ups like Blossom Social, but none have ever been successfully embedded in a platform. Given that crypto is comprised of a variety of networks already, lifting and shifting some of those ideas around community interaction/participation may be a new form of sustaining advantage that is ripe for exploration.

Looking Back to Look Ahead

The lessons from history offer some useful guiding principles for how the years ahead might play out for crypto trading platforms in Canada. The question then shifts to what comes next?

Looking back at the traditional online brokerage industry, its growth came in three primary phases that tie together through what we can call the Competitive Dynamic Cycle:

- The Cultivation Phase: Building the market. Every E*TRADE baby commercial did not just help E*TRADE expand its brand awareness, it helped the entire industry register on the radars of millions of potential new customers. The online brokerage business had to grow its own market from scratch, convincing an entire generation of new investors that they could “do-it-themselves” online. Actions in this phase were executed by individual companies, but worked collectively in aggregate to grow the size of the pie for everyone involved.

- The Planting Phase: Seeding as many relationships as possible. As the market expands, there is more ground to be gained by convincing non-investors to join the industry than there is to convince existing clients of other brokers to make a switch. This is when the ‘land grab’ takes place and is where TD Direct Investing built up their aforementioned lead.

- The Farming Phase: Nurturing and expanding relationships over time. Unfortunately, all good things must come to an end. Markets will not expand forever, the flow of new clients into the industry will slow and the size of the pie will stop growing. This turning point forces a change in the competitive landscape, where competition becomes zero-sum and price/feature competition make value propositions converge. At this point, existing client relationships become sacred and the path to growth comes from expanding existing relationships rather than trying to grow new ones.

The traditional online brokerage game has of course become one of farming. Crypto trading, on the other hand, is still [arguably] in the cultivation phase.

*While Planting and Farming are activities that are too far in the future to discuss, the remainder of this article will focus on the art of Cultivation.

Cultivation: Building the Market from the Ground Up

Before a plant can grow, it requires the right environment: sunlight, proper temperature, moisture, air, and nutrients all need to align.

Similarly, before a market can grow, it needs to have alignment between external and internal conditions. External conditions come from the macroenvironment (regulation, technology, demographics, social trends, etc.), whereas internal conditions are under the control of the companies themselves (marketing, product development, collaboration).

Building the market involves understanding the external conditions in order to maneuver appropriately and align them with internal conditions that will bring new potential clients into the industry.

Understanding External Conditions

There are two primary external conditions that will play an important role in the crypto industry’s near-term evolution: regulation and demographics.

Regulation:

The regulatory path is relatively clear for Canadian crypto trading platforms (CTPs).

In March 2021, the CSA and IIROC published a joint staff notice entitled: Guidance for Crypto-Asset Trading Platforms: Compliance with Regulatory Requirements. In it, the regulators spelled out their expectations for how securities legislation applies to CTPs. With some consultation and study, it was determined that CTPs operate in some cases as a dealer, in other cases as a marketplace, and in many cases, they operate as both. Consequently, the existing securities legislation governing both sets of activities should apply.

Here, we have to pause for a second and give some kudos to the Canadian securities regulatory bodies. Relative to other less crypto-friendly global regulators (we’re looking at you SEC), the Canadian regulators appear to be much more consultative in their approach and have kept open lines of communication with the industry. As a result, there is now a clear path for CTPs to become regulated entities. All CTPs in Canada will have to register with the applicable regulatory body, but will be given up to a two year period to transition to a long-term regulatory framework (ie. as an investment dealer or marketplace).

At the same time, we need to recognize that the industry is only at the beginning of the regulatory path. Existing securities laws have been interpreted for crypto, but no new crypto-specific legislation has been passed. In addition, there are also certain conditions imposed on platforms in the interim period that vary depending on the type of exemptive relief they are seeking. Some of these may create challenges (eg. the $30,000 investment limit for non-eligible crypto investors imposed on some CTPs) and others may hamper the speed of product development in the near-term.

While those costs are rather steep, the benefit of working with the regulators derives from increased clarity/confidence and having a clear set of rules/guidelines to operate within. There are 11 CTPs that have now started down the path of becoming a regulated Canadian entity with this assurance at their back. This clarity has also forced some international firms operating in Canada to withdraw, either voluntarily or through enforcement actions like those levied by the OSC against Poloniex, OKEx, Bybit and KuCoin.

An additional result of this clarity will also mean more traditional online brokerage firms will likely enter the space. It will be one or two at first (ie. probably smaller independent firms like Questrade), but once the idea has been de-risked enough, more will follow. I suspect this will be after cultivation is complete and the planting phase begins.

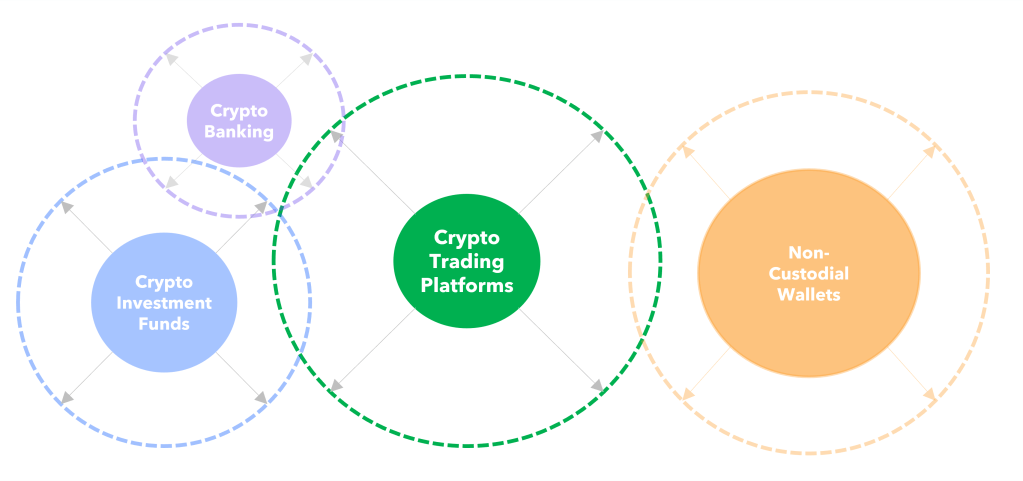

From this point forward, it will be important for firms to continue to monitor developments on this front. Regulatory change will impact how the industry in Canada develops, not just for CTPs, but for all adjacencies in the financial services arena:

- Investment Funds and Other Substitutes: Outside of crypto trading platforms, Canadians may have other paths to gain exposure to crypto investments. In Canada, only 20% of households have a self-directed investment account, the remainder tend to rely on financial advisors to manage their capital markets exposures. Therefore, other areas of securities legislation, like the laws that govern investment funds and structured products will influence the size of the market available to CTPs. Similarly, other access points in the financial system like deposit-takers themselves may eventually open up. Guidance from banking regulators like OSFI and provincial credit union regulatory bodies may also require monitoring.

- Non-Custodial Wallets: Non-custodial wallets allow the user to have sole control over their private keys. They allow individuals to be ‘self-sovereign’, becoming their own bank, taking on the unique benefits and risks of self-custody. Metamask, Coinbase Wallet, and Phantom are all non-custodial wallets that have millions of users and are globally accessible. Non-custodial wallets can be considered both complements and substitutes to CTPs. To the extent non-custodial wallets enable individuals to invest outside of CTPs, they can be considered competitive and the rules governing payment on-ramps and off-ramps (ie. Proceeds of Crime and Terrorist Financing Act) will play a role in enabling this set of activities. To the extent that wallets play a complementary role in the ecosystem where assets may be sent after being purchased on CTPs, the degree to which an individual is empowered to operate in a self-sovereign way is influenced by things like the interpretation, application and enforcement of Canadian tax law.

- Other areas to watch: Additional interpretation of securities law will continue to take place, specifically around the definition and categorization of various cryptoassets like stablecoins, DeFi protocols, and NFTs. These areas of interest will determine how Canadians are able to access these opportunities and to what degree CTPs will participate. Accounting standards (eg. FASB’s recommendations) will also have an impact on the industry, with most digital assets treated as indefinite-lived intangible assets (that only require reporting once a year) as opposed to being treated as traditional financial assets that can use fair-value accounting methods. Among other things, developments on this front could help build institutional comfort and adoption with the asset class.

Cultivation will mean expanding the CTP bubble as well as each of the other domains. The key point here is that regulation will be a factor that helps build the market, rather than limit it. There is also the opportunity to help influence how these areas will evolve by engaging in consultation and allowing the industry to have a voice at the table.

Demographics:

According to a study recently conducted by the OSC/IPSOS, Canadian crypto clientele tend to be young, male and relatively high-income compared to the general population.

This cohort (young, male, high earners) are the early adopters and will likely continue to be the dominant profile in the industry’s client base.

From a cultivation perspective, that means other demographic areas present opportunities to expand the industry. That requires more gender balance by growing female participation, more age balance by engaging older cohorts, and more equality across income levels by ensuring lower-income earners have the same access to opportunities as high-income earners.

Encouraging more gender balance in participation is an ongoing opportunity in Canada. Interestingly, the 67%/33% male/female split is not far from that of the traditional online brokerage industry which is only slightly more balanced (but not quite 50/50). Yet, for both CTPs and the traditional online brokerage world, there is an opportunity to encourage and enable greater female participation. In Canada, there are some fantastic organizations like CryptoChicks and The Canadian Blockchain Association for Women that are already executing on this mission.

Engaging older cohorts is the largest opportunity for cultivation. However, study after study shows that older generations show a reduced degree of awareness, familiarity and interest in cryptoassets. That’s not a surprise, given that the adopters of most new technologies tend to be younger in age and less set in their ways. Increased adoption on this front will likely come from blending crypto into more established online brokerages whose clientele actually tend to skew more baby boomer than millennial (largely a result of the traditional online brokerage industry coming of age during the 1990s and 2000s at the same time that the baby boomers were reaching their peak wealth accumulation years).

Encouraging an even playing field across the income continuum is the most challenging of the three opportunities. There is a chicken-and-egg conundrum here in that lower-income Canadians first need to have assets to invest before being able to participate. Outside of trying to address broader societal issues of income inequality, the crypto industry has the opportunity to at least offer lower-income earners the same access to opportunities as high-income earners along with adequate protections and education. Insomuch as that remains true, this area of the market will continue to expand.

Internal Conditions for Growth

There are three primary internal conditions that can play an important role in the industry’s near-term evolution: marketing, product development and collaboration.

Marketing: Expanding the top of the funnel.

While nothing can expand interest and awareness for crypto like a good old fashioned bull market, outside of “number-go-up”, the collective marketing efforts of crypto companies across the country (and beyond) will play a role in continuing to generate awareness, familiarity, and legitimacy in the public domain. From Crypto.com banners floating above Formula1 race tracks to Kyle Lowry showing up on Bitbuy commercials encouraging people not to “miss their opportunities”, every piece of exposure counts. Although companies are acting individually to grab their share of the pie, they are also acting collectively to expand the market as a whole. Everything these companies do create the aggregate brand of ‘crypto’ in Canada, which both directly and indirectly helps to cultivate the industry.

Product Development: Expanding the base of the funnel.

As mentioned earlier, a CTP’s differentiator will not be its trading platform if it hopes to retain a long-term competitive advantage. On traditional crypto trading platforms, buying and selling is the only function you can perform. That places an invisible asymptote on the growth of the industry. Accordingly, product development requires firms to stay at the edge of the Overton Window and expand the market by introducing new crypto products and use cases. With each new use case introduced, the market expands and the invisible asymptote lifts higher.

Buying/Selling: Today, trading is the primary product offered by CTPs.

Staking: The ability to lock up your assets to earn yield by helping to secure proof-of-stake networks is likely the next addition to the platforms of CTPs. In fact, Wealthsimple became the first in Canada to allow regulated access to staking, recently opening up the ability to stake both ETH and SOL. Bitbuy has also expressed their intent to add staking to their platform in the year ahead.

Providing Liquidity: One step further from staking is being able to lock up assets in other ways. The most promising opportunities lie in the DeFi arena, providing liquidity to facilitate different financial functions. Automated market makers, decentralized lending protocols and derivatives liquidity protocols are all examples of areas that investors can tap into to directly earn yield on their existing cryptoassets. It is becoming clear that anyone holding cryptoassets and willing to bear some additional risk would be open to the expanding option-set DeFi participation can provide.

Participation in Web3: Collect (NFTs), Permit (NFTs), Play (Gaming), Participate (Governance), etc. Participation in Web3 today is largely done through non-custodial wallets. The challenge with non-custodial approaches is that they expose the user to the risks that come along with self-custody. Solving for custodial access executed through a regulated platform will not be easy, but would go a long way in opening up CTPs to use cases that go well beyond simply buying and selling assets.

In addition to expanding the pie, each of these avenues provide paths toward more continuous engagement, rather than the boom-and-bust-driven cycles that are tied to the transactional nature of online brokerage.

For today’s CTPs that do not currently offer equities trading, adding traditional stocks and bonds to the platform provides another avenue of expansion. However, since this market is already well-served and saturated, it does not contribute [as much] to cultivation and building the market.

Collaborative Efforts: Altering Macroenvironmental Conditions

The beautiful thing about the cultivation phase is that competition is not as intense as in later stages of industry development. Everyone has the same goal of expanding the industry, rather than fighting over each others’ existing customers.

The opportunity to develop the market can be approached through individual actions that sum collectively, or it can be approached collaboratively through various industry initiatives. The Canadian Web3 Council is a good example where resources can be pooled in order to advocate for responsible public policy and regulation in the space.

Outside of presenting a united front to working with regulators and lawmakers, most macroenvironmental opportunities for cultivation can be approached through a collaborative lens. Supporting organizational efforts to encourage financial inclusion, build gender parity in participation, or expose new generations to cryptoassets are all on the table.

In addition, there are certain industry best practices that can be shared to avoid duplication of effort in order to move the industry forward. For example, there are a number of different unique cybersecurity and fraud risks that are present for anyone participating in the crypto ecosystem. Given that security breaches and frauds will damage the reputation of the industry as a whole, the extent to which best practices can be developed and propagated to all will go a long way toward cultivating a larger market.

Summing up

This is only one person’s opinion on the path the industry will follow in the years ahead. Crypto is currently at the start of the competitive dynamic cycle and is about to go through the cultivation stage in Canada. Firms will continue to engage with regulators, encourage broader demographic participation, collectively contribute marketing dollars to build the collective crypto brand, add additional crypto products to expand engagement beyond buying/selling/investing and promote a collaborative approach to market development through a variety of different avenues.

That said, as the Planting and Farming stages approach in the distance, lessons from the online brokerage industry’s past should be kept in mind. It is inevitable that the crypto market will go through a similar cycle where competition with the Big Six banks, finding a long-term sustainable revenue model, and identifying ways to differentiate beyond the trading platform are all bridges that will have to be crossed.

Until then, it is time to cultivate!