I was recently listening to Michael Kitces (Financial Advice Industry Guru) talk to Joe Duran (Head of Goldman Sachs Personal Financial Management) about the competitive dynamic in the financial advice industry and how it had shifted over the past few years. Joe provided commentary on three big predictions he had made that have started to play out:

- In an independent advice industry that has largely been comprised of regional firms and lifestyle businesses, a true national wealth and advisory player would emerge

- Big wirehouses and Wall Street firms would start to see the allure of new client acquisition pipelines and be lured into the corporate marketplace (ie. the acquisition of stock plan administration companies like Morgan Stanley’s acquisition of Solium)

- The industry would start providing more comprehensive services to the end client by expanding their suites to include: tax prep, estate planning, private banking products, and niche advisory services / special situations (like planning for a child with a disability). And the kicker: they would do it all for the same 1% advisory fee that has been a staple of the business going back decades.

While points #1 and #2 are noteworthy on their own, point #3 had me thinking. Maybe it is the constant talk of inflation on every news channel that keeps pricing top-of-mind, but the pricing dynamics in the financial advice business are hard to find a parallel to.

When reflecting on the throughlines of industry content over the past several years, the idea that the price of financial advice would fall was a constant point being made. Conferences, industry publications and twitter conversations—everyone was saying the same thing: the price of advice was bound to fall thanks to rising levels of competition and the commodification of the construction and maintenance of a diversified portfolio (from funds-of-funds to robo-advice).

But the price has not budged. As Joe said, the 1% advisory fee holds, but advisors are now doing a lot more for clients to earn those dollars. This is somewhat akin to the dynamics present in the smartphone market, particularly around iPhones. The recently launched iPhone 14 model starts at $799, not much more than the price of the iPhone 4 at launch, which was $599. Sure, there’s a little inflation in there, but think how much more value people get out of their iPhones today than in 2010 when the iPhone 4 came out (just take a look at screentime alone). There was certainly no Tiktok, Uber, or Robinhood to keep us occupied in those days. Consequently, the increase in value is much greater than the increase in price.

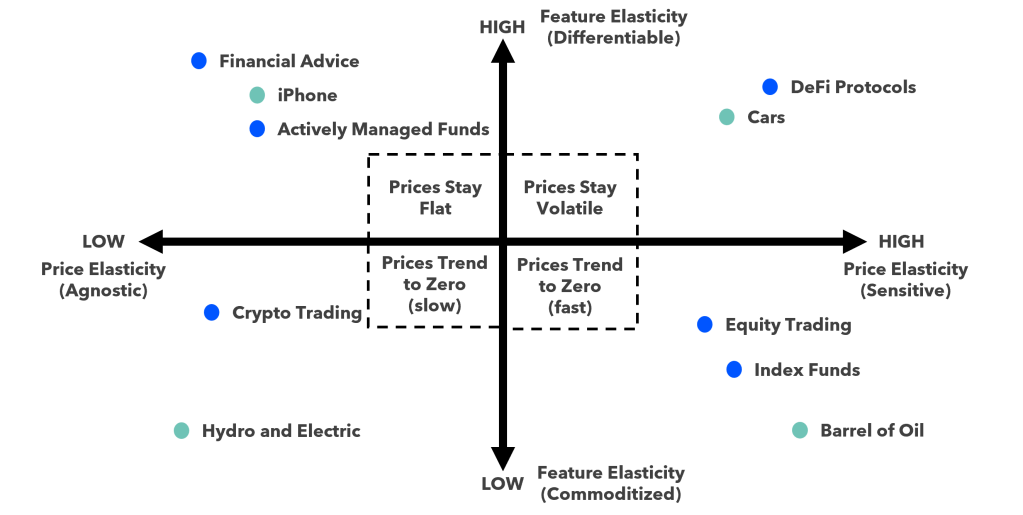

I’m taking a long time to get to the punchline here, which is that financial advice falls uniquely into a place on the Feature-Price-Elasticity Matrix below.

Price elasticity is a familiar concept: it is the sensitivity of demand to changes in price. For things that are highly price elastic, as I raise the price, I’d expect an offsetting drop in demand. People would flee the supermarket if they started offering $10 avocados, but they would rush back if they dropped the price to $0.25.

But what is feature elasticity? I’m sure there is some concept in an economics textbook that captures this already, but to me, feature elasticity is the same thing as above, just applied to the features a product or service offers. More specifically, feature elasticity is the sensitivity of demand to changes in the quantity or quality of a product’s differentiable features.

For things that are highly feature elastic, as I increase the number of differentiable features, I’d expect an offsetting increase in demand. People seemed to Cash App as an easy way to send money peer to peer, but demand certainly shot up after they added features like Spend (a debit card linked to the app) and Invest (easily buy stocks and bitcoin in the app). Cash App’s value proposition was highly feature elastic.

But wait… this sounds a lot like product development, adding features, and improving a product/service over time. And the answer to that question is, yes, it is. But what makes feature elasticity distinct is whether or not those features are able to marginally differentiate the product/service. Things that are highly feature elastic are by definition, differentiable, or in other words, a not commoditized. It is hard to add features to a barrel of oil. It is a commodity and thereby, not feature-elastic. It is hard to add new features to a savings account. It is a mature product line and thereby, not feature-elastic. It is much easier to add features to a peer-to-peer payment service as noted above, which is less commoditized and allows the service to be differentiated in the minds of users.

When you combine price elasticity and feature elasticity, you get a Feature-Price-Elasticity Matrix which illustrates some interesting competitive dynamics.

The matrix produces four quadrants, which each have their own pricing dynamic:

- In the upper left quadrant, with high feature-elasticity and low-price elasticity, prices tend to stay flat. Price competition does not impact these markets as consumers are relatively agnostic to price levels, so producers are forced to compete on other factors (ie. the quality and quantity of the features they offer). This is how iPhones manage to keep pricing [relatively] stable while delivering so much more value to users.

- In the upper right quadrant, with high feature-elasticity and high-price elasticity, prices will go through cycles and volatility. Producers compete on feature innovation, raising prices alongside new releases, but then quickly see that pricing/feature advantage competed away. Cars follow this dynamic, with new features released every year: blind-spot monitoring, heated seats, Apple CarPlay, back-up cameras, accent lighting, etc. Each feature release initially commands a premium, but one which quickly disappears as other manufacturers catch-up and consumer expectations ratchet higher.

- In the lower right quadrant, with low feature-elasticity and high-price elasticity, prices tend to trend to zero quickly. These are tried and true commodities like the aforementioned barrel of oil where differentiation is not possible and pricing becomes [almost] all that matters.

- In the lower left quadrant, with low feature-elasticity and low-price elasticity, prices tend to trend to zero slowly. This occurs when there is little ability to differentiate, but the consumer is unable or unwilling to drive the price lower. Hydro, electric and other utilities fall into this bucket thanks to high switching costs and little consumer choice.

Now let’s add financial services examples into the mix:

Financial Advice: As mentioned before, financial advice is a difficult service to make tangible to the consumer. It is hard to define, and therefore, hard to put a price on. So for financial advisors to standout, they typically have to rely on differentiation which typically means going deep (specializing in a specific niche like Canadian ex-pats) or going broad (adding more services to the mix). Add in the fact that most financial advice is paid for through fees based on assets under management (which is out-of-sight and deducted from an account rather than invoiced) and the result is a consumer group that is not price sensitive, and a producer group (advisors) who are always striving to add more value, which leaves the competitive dynamic in place Joe Duran mentioned at the outset of this piece.

Active Investment Management: Active management follows a similar pattern to financial advice. The value of active management can be hard to put a finger on and define (my alpha-producing thesis could work out at any minute), but has tons of avenues to differentiate (if you ignore some of the closet indexing taking place out there). The pricing—for consumers, that is—of truly actively managed funds also has not shifted much over the years, thanks to price agnosticism and perhaps a lack of ability or motivation to interpret the value-price trade-off. Given these characteristics, the pricing of true alpha-chasing active management will also likely stay stable over time.

Passive Investment Management: Passive management has followed the path of commoditization: there are few ways to differentiate beta. While some consumers are price sensitive when it comes to their investment funds (often those who are self-directed or use a financial advisor for validation), others are not (those who outsource completely). The reason index funds are highly price elastic has more to do with how they are distributed: advisors are now able to construct low-cost passive portfolios for their clients at an incredibly low price—and when acting for their clients, many advisors like to be quite price sensitive on their behalf.

Equity Trading: Plain ol’ equity trading has largely been commoditized in the financial services arena today with industry stalwarts like Schwab and Fidelity having millions of users on their platforms and embedded investing services like DriveWealth and Apex starting to plug access to brokerage accounts into other large financial services giants. The pricing game has largely played out here already (things in this quadrant move quickly), with commission prices now at zero across the [U.S.] industry. The question of when firms start competing on the rates they offer on their cash sweeps might be the next ‘price’ that the industry aims to compete on.

Crypto Trading: Crypto trading is similar to trading stocks in many ways, but it differs in one major way: people are still willing to pay much higher commission rates and spreads then they are in the world of equities. While this will slowly go away over time, at present, crypto trading enjoys a surprisingly sticky novelty premium where users continue to pay for a relatively commodifiable set of services. This could be chalked up to the relative inexperience of the early adopter and fast follower cohorts coming into crypto over the past few years, or it could be that people are less price-sensitive when it comes to crypto trading fees because there is such a strong belief that price appreciation will eventually squash its impact. In either case, the premium has shown some staying power, despite a plethora of competition entering the market.

DeFi Ecosystem and Web3 Wallets: Finally, pointing out a rare upper right quadrant example, with high feature-elasticity and high-price elasticity, it is the DeFi ecosystem. DeFi is a pretty wide net to cast today, with many protocols still figuring out their pricing models. However, that is what makes the space so feature-elastic. There is a high degree of innovation, trial-and-error, and feature experimentation taking place. Layer on the added crypto characteristic of open-source and easily copied / forked code, and there is a recipe for high repetition feature releases. Because of this ‘easy copy’ trait of DeFi, most protocols must opt to stay cognizant of price competition—this is particularly the case because the current set of participants in the DeFi ecosystem today are likely relatively crypto-sophisticated and may be sensitive to the fees they pay.

Remember the Nuance

This discussion about pricing brings us back to the current environment. With all the talk about inflation and price levels, the conversations often lack nuance. Our typically quoted measures of inflation (CPI, PCE, etc.) are an average of prices around the economy. The problem with averages: by measuring everything together in aggregate, they become a poor indicator about the individual components.

There are clearly a variety of pricing dynamics taking place across industries and products. Some are influenced by supply chain bottlenecks and rising energy prices, others are influenced by rising interest rates and tighter monetary conditions, and others, like the price levels in financial services, are influenced by specific industry and product characteristics. There is more room for nuance in conversations around pricing dynamics, and feature elasticity is one more factor to add into the discussion.

One response to “Feature-Elasticity: Why 1% Financial Advice Fees Are Safe, But Trading Revenue is Not”

[…] Commissions are often priced as a percentage of dollar trading volume (eg. 0.1%-2.0% fee per transaction) versus the flat dollar amount (eg. $9.95) that is common in the retail equities business. That fact should make a lot of online brokerage industry executives jealous since it a much more profitable commission format. That pricing will eventually come down, just as price competition has driven equity commission rates toward the $0 threshold. Although it may take longer than expected. […]

LikeLike