This past summer, Canada celebrated its 155th birthday. It was all the way back in 1867 that Ontario, Quebec, Nova Scotia and New Brunswick were officially tied together under the British North America Act that proclaimed Canadian Confederation and independence from the British. A full fifty years prior, in 1817, the Montreal Bank (now known as the Bank of Montreal or BMO) was founded as (arguably) the region’s first bank.

Given that the banking system in Canada pre-dates the entire history of the country itself (at least, in its current form factor), it is safe to call the financial services business a mature industry. Like other areas of the economy that reach the ‘maturity’ stage of the industry lifecycle, the financial services industry in Canada can be diagnosed as such based on some of its key characteristics:

- The presence of large established and very profitable companies: five big banks, three big insurers

- Intense head-to-head competition reflected in everything from feature copying to price gouging

- Industry consolidation as M&A becomes one of the only viable paths to growth: the reason why Canadian banks have developed a recent appetite for U.S. regional banks and wealth management companies

- Product commoditization as the cross-competitor product/feature set trends toward a common middle: In Canada, this has resulted in a lack of differentiation across the core financial service value propositions

As a mature industry, the factors that firms compete on have started to become those common to other commoditized businesses, namely: price, cost and distribution. Competitive and targeted interest rates, flat or reduced service fees, streamlined and increasingly digital operations, and a fulsome brand/channel presence have been at the center of the strategic playbooks of most financial institutions for the past decade(s).

At the same time, recognizing that the symptoms of a commoditized market eventually lead to shrinking profit pools, many FIs have also looked for ways to compete on non-commodity factors. This includes venturing horizontally into business lines like investing, insurance and alternative lending; and, venturing outward to compete on the experience layer, building out digital channels and revamped branches.

But the one area that nearly all large integrated financial institutions have gravitated toward over the past five years ties together both the horizontal and outward expansion factors: Financial Advice. From goals, to planning, to just talking about life, to differentiate away from the underlying commodity-like products, financial services firms have placed ‘advice’ squarely in the middle of their positioning in the market.

- Scotiabank is currently guiding people through a world of bad advice. They are doing so with the most prominent positioning around advice with ScotiaAdvice+.

- BMO is in the market positioned as a purveyor of peace of mind. The firm also has adviceDirect, an advice hub, and the recently launched and heavily promoted BMO WealthPath tool.

- TD is “giving back and leading in the advice space”, doubling down on its digital access points and tools. The advice hub, TD Ready Advice, gives customers a centralized access point to cover a variety of financial topics.

- CIBC’s idea of Ambitions Made Real embodies a commitment to helping customers set and reach financial goals. CIBC’s hub, CIBC Smart Advice, offers up a variety of tools, how-to’s, and guides.

- And RBC is covering all of the bases from MyAdvisor to NOMI to the beyond banking services supported by RBC Ventures.

Advice is the new norm. It is viewed as the differentiator, separating brands in the minds of clients. It is viewed as the relationship consolidator, tying together clients’ financial lives and encouraging them to bring over business from other institutions. It is viewed as the value creator, helping clients make progress toward their goals and stay on the right financial track.

But for everything that has been built around advice, what has been lacking is a definition of what exactly ‘advice’ is. What specifically are all these firms differentiating on? It seems like many of them are playing high stakes poker, and have all placed their bets without first seeing their cards.

What is needed is a definition. Here’s what I could dig up on Law Insider:

A) Financial advice means the process of engaging in the business of advising others with respect to the planning and/or the execution of advice in respect of selecting, purchasing, or selling financial products.

B) Financial advice means providing an ongoing, customer-centric service in terms of which financial customers’ financial circumstances, as measured against their lifestyle goals, needs and priorities are assessed that culminates in delivering financial solutions and/or Financial Product Advice which is implemented, monitored, and adjusted from time to time;

C) Financial advice means any written advice, analysis or report in regard to one’s financial circumstances.

The first definition is the most general: it is guidance offered with regard to prudent future action. There is nothing about what qualifies someone to provide advice, nothing about the ingredients required to formulate the guidance, and nothing about implementing the advice after the fact. It is purely a recommendation tied to action.

The second definition is more specific to financial advice. It aligns best to what most financial institutions would recognize in the market today. Advice should take into account factors from a client’s life (personal and financial), analyze and assess them, and deliver a recommendation and potential solution set [which today, are often the institution’s own products]. Advice is a recommendation as well as a process to come to that recommendation.

The third definition is the most tangible: advice is the proof of work done to assess and recommend. It is not just analysis and guidance, it is physical or digital evidence. Of all the clients of a financial advisor that are asked if they receive ‘advice’, those that are most likely to say yes are those that have a physical printed financial plan (likely collecting dust or stowed away in a cabinet drawer) that they can point to as evidence.

The three definitions above are empirically based, and those first three were just skimming the surface. What becomes apparent is that there is no singular definition of financial advice. Finance is too deep of a domain and advice is too broad of a concept to come together nicely. But this presents a problem (or maybe an opportunity?). If the industry is placing a lot of chips on the table betting on ‘advice’, then being more specific about what that means is both strategically important for financial institutions AND potentially beneficial for the clients they serve.

Side note: I am quite sure many people have defined financial advice before (there were many more Law Insider definitions than the three above), but a multi-faceted view of the advice provided by large integrated financial institutions does not appear to be common, at least not based on my Google searches. What comes next is one person’s taxonomy of what financial advice could entail.

Diving Deeper into Defining Financial Advice

To start, this problem can be approached from a designer’s point of view by first trying to understand what the design space looks like. First, let’s break the words down one-by-one: financial, then advice.

Financial Surface Area

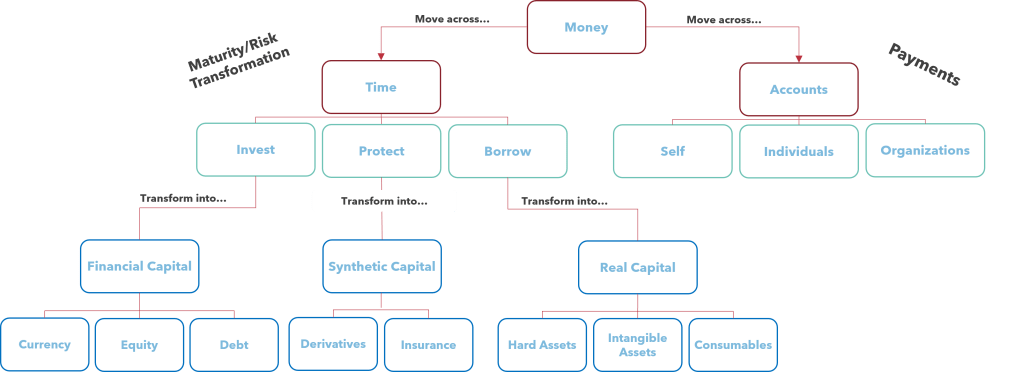

Finance is an incredibly broad industry which ultimately exists as the circulatory system for the economy. It is a facilitator of economic activity, and for consumers (which the focus is limited to for this discussion), that economic activity is best described as their ‘lifestyle’. Finance facilitates modern life. It helps us accrue, store and transact the value we create in the world. At this high level, financial services have two primary functions: help people move money across A) time or B) space. This is the surface area of personal finance.

Moving money across time is equivalent to enabling people to borrow or invest. You borrow money from the future and bring it into the present when you take out a loan and purchase a new car. You take money from the present and bring it into the future when you park a percentage of your salary each month in a pension plan or 401k. The third tangential function aside from helping people ‘invest’ and ‘borrow’ is to help them ‘protect’. This is primarily executed through insurance or other derivative contracts that provide guarantees in exchange for a fee.

Moving money across space entails moving money between entities. From a personal finance perspective, that means enabling transactions to and from your accounts. Credit cards, Venmo, ATMs, wire transfers, and all the many other payment systems that exist today support these activities.

That is it. The surface area of finance. And in defining the ‘financial’ in financial advice, the definition should extend across the entire surface area since each of these components is ultimately important in facilitating the lives of the consumers with which it interacts.

Life Surface Area

As complex as the financial surface area is, life surface area is much more so. It is less concrete and harder to break into specifics. To simplify things, we’ll refer to the ‘life surface area’ as lifestyle from here and look at lifestyle through three lenses: time, needs and capital.

Lifestyle defined by time is how you allocate your most precious resource across a variety of domains. This image below from the OECD consolidates information from time diaries across the world. While comparing things like the amount of time spent on sleep vs education (wow, South Korea appears to be sacrificing shuteye to cram for exams), what we’re after here are the categories.

People spend most of their time on sleep, work, leisure, personal care and education. Day-to-day, that’s what makes up a lifestyle.

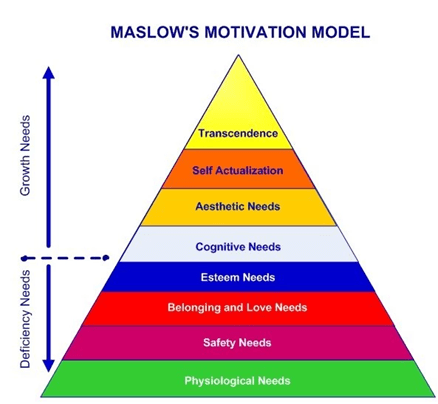

But time spent tells us nothing about the quality of a lifestyle. What about the things that matter? In defining what matters, although it arguably has some flaws, the classic theory of motivation showcased through Maslow’s Hierarchy of needs provides a useful framework.

In it, Maslow breaks down needs into two buckets: growth needs and deficiency needs.

- Deficiency needs: social, safety and physiological. If they are not met, deprivation causes deficiency and sparks motivation to fill the need. These are the basic needs of all humans and they must be met before someone can adequately pursue higher-level growth needs.

- Growth needs: cognition, beauty, success and spirituality. These are the pursuits of meaning. In the book The Power of Meaning journalist Emily Esfahani Smith suggests people find meaning in life through four pillars:

- Belonging. When we are understood, recognized, and affirmed by friends, family members, partners, colleagues, and even strangers, we feel we belong to a community.

- Purpose. When we have long-term goals in life that reflect our values and serve the greater good, we tend to imbue our activities with more meaning.

- Storytelling. When it comes to finding meaning, it helps to try to pull particularly relevant experiences in our lives into a coherent narrative that defines our identity.

- Transcendence. Experiences that fill us with awe or wonder.

In defining lifestyle through needs, we can map the degree to which growth and deficiency needs are being adequately met.

So if lifestyle presented as an equation, it can be looked at as time spent times the quality of what that time is used to pursue.

Lifestyle = (Time Spent x Needs Met)

Translating that into something more tangible for the financial services industry, most people have goals and objectives about how specifically they would like to spend that time or what needs they would like to be met. This means that:

Financial Goals = E(Time Spent x Needs Met)

Bridging the Financial and Life Surface Areas

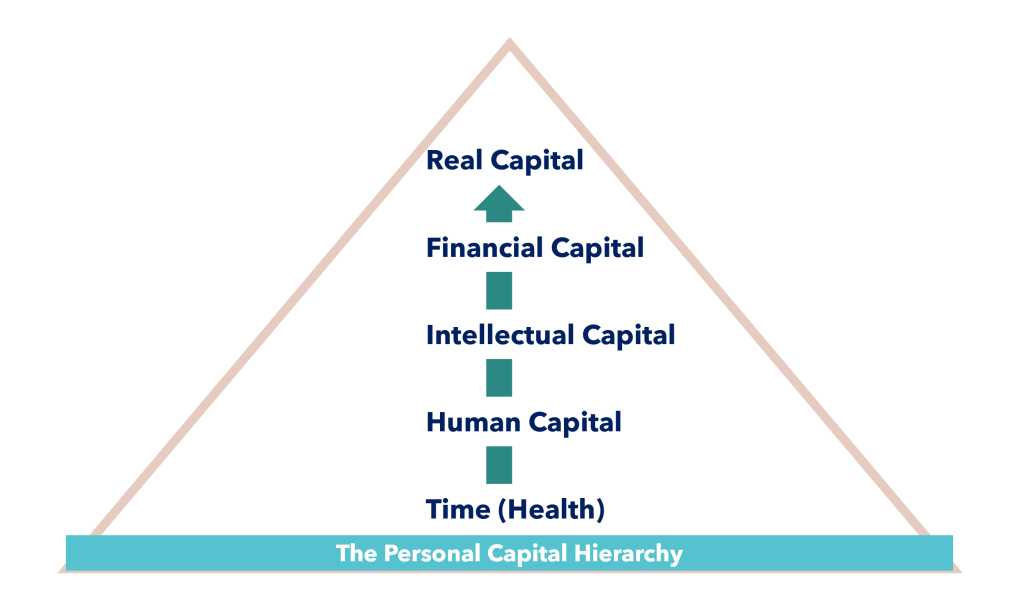

In attempting to tie together the complexity of someone’s lifestyle with the massive financial surface area that exists in the world, we’re going to introduce a new concept: the Personal Capital Hierarchy.

Personal Capital is simply how lifestyle (aka, time and needs and the goals we set around them) produces assets that accrue to the individual.

We are all endowed with similar form of basic capital from birth: time. There is a caveat here that health has such a bearing over how that time is spent, it must be included as part of the basic input. This forms the base of the Personal Capital Hierarchy. We spend that time in pursuit of the aforementioned needs. The product of which can be thought of as different forms of capital (see exhibit).

Each form of capital can transition into the next. Time can be spent building human capital: our education, skills and social capital. Human capital can be spent on building intellectual capital: actions (know-how) and ideas (intellectual property). That intellectual capital can be translated into financial capital: cash, debt, equity. And finally, that financial capital can translate into real capital through our purchases and investments: physical property/assets, real estate, consumables. Note that there is typically a flow in this transition of capital, much like Maslow’s hierarchy. Assets start at the base (time) and flow upwards in the stack toward real capital.

So, in attempting to summarize the bridge between financial and life surface areas in one sentence:

Our time is spent pursuing various needs, the products and by-products of which are different forms of capital that eventually form our financial capital.

To date, most financial advice focuses on managing and moving Financial Capital. But if finance is ultimately a facilitator for people’s lives, then it is influenced by the entire Personal Capital Hierarchy. Advice must consider all of what’s encompassed across an individual’s time, needs and capital. To point out the obvious, this is a massive undertaking!

Simplifying through Financial Health

To simplify things, another closely related concept useful to bring into the conversation is the idea of financial health. Financial health generally refers to the state of one’s monetary affairs. It is how your overall financial standing is perceived relative to your expectations. Is your financial health positive or negative, good or bad, AAA or BBB-. Regardless of how the assessment is made, your financial health is what ties all of your financial affairs together and the decisions made across the surface area of finance—and indirectly, the surface area of life—all have a direct impact on its standing. Made a late payment because you lost your job because your skillset (human capital) was outdated? It impacts your financial health. Made a smart investment thanks to the friend (social capital) who gave you a good stock tip? It impacts your financial health. Bought a home and chose a variable rate mortgage over a fixed rate? It impacts your financial health.

Since financial health ties everything for an individual together in one score, we will select it here to represent an objective measure of ‘financial’ in ‘financial advice’.

The definition of our first word is complete:

Financial = the facilitation of one’s lifestyle through the financial system, covering the entire surface area of finance, and measured by the state of one’s financial health.

Examining Advice

Believe it or not, as hard as it is to put boundaries around the topic of personal finance, it is even harder to put boundaries around the word ‘advice’. As pulled together earlier, advice is simply guidance offered with regard to future action. But what does that guidance specifically cover? There are a couple major variables that go into the consideration set:

- General and/or Specific: Advice can be general, rules-of-thumb with wide application that can be suited to a number of people in a range of different circumstances (eg. diversification is the only free lunch in investing, so make sure to put your [nest]eggs in more than one basket). On the other hand, advice can be specific, tailored one-to-one to suit a specific person at a specific time with a specific need (eg. You have a high degree of risk exposure through your employment at a technology startup, so we’re going to ensure your portfolio balances that out by overweighting investments in other sectors).

- Continuous and/or Asynchronous: Advice can be continuous and proactive, provided on an ongoing basis or in a steady stream as is the case through the annual check-ins most financial advisors perform. Advice can be asynchronous and reactive, provided on an ad hoc basis as the need arises. These needs often arise during life events: graduations, marriages, new jobs.

- Deep and/or wide.Advice can be deep, truly focused on one topic (my insurance specialist would agree). But advice can also be wide, stretching across multiple domains (my financial planner would also agree).

Advice has many characteristics, and hence, comes in many different forms. But what dictates which ones are expressed given a particular situation depends largely on the inputs available to the advice giver and the advice taker’s circumstance. While we’ve discussed the advice taker’s circumstances at length (covered by the surface area of finance and the surface area of life), there are several other important ingredients to advice that must be considered in its definition.

Inputs to Financial Advice: Needs/Wants, Trust and Data

For adequate advice delivery, certain inputs are required for the advice giver to be effective. The three primary inputs are: needs/wants, trust and data.

Needs/Wants: For advice to be given and received, there must first be an identified need for advice. Often, the obvious need comes from some sort of known information gap that the advice taker is looking to fill by consulting an advice giver. A simple example is the family doctor: I don’t have sufficient knowledge in the medical field to diagnose myself when I feel under the weather (nor do I have the time to gather all of the necessary knowledge on my own) so I seek advice from someone I deem as qualified to provide it. Outside of the aforementioned information gap, in the financial domain, advice needs arise for a number of reasons:

- Optimize the outcome: Seeking advice to increase the probability of a positive financial outcome.

- Outsource decision-making: The ability to take the stress of financial decision-making off one’s shoulders or the ability to outsource the time and effort required to make and implement decisions (not everyone wants to spend hours doing their own investment research)

- Optimize trade-offs: The ability for a more knowledgeable third party to help weigh the pros and cons of decisions with trade-offs (eg. risk vs reward, consumption today vs saving for tomorrow, etc.)

- An external lens: The ability to tap into a [hopefully] unbiased third-party opinion on one’s affairs, either for feedback or an alternative perspective.

- Implementation support: Not everyone knows of, or has access to, the means to implement financial recommendations, in which case, the advice giver is also a provider of tools/solutions. For example, this is true of advice around protecting human capital, the solution to which typically comes from an insurance product shelf that can typically only be accessed through a licensed broker.

- A catalyst for action: Sometimes people do not know how to (or don’t want to) take action in their financial lives and an advisor can be the catalyst to get things moving.

As a side note: not everyone needs financial advice! Many people are well equipped or have the preference to take control of their own finances and that is perfectly okay. Advice is not suited to everyone, but it is typically relied upon to satisfy one of the needs mentioned above.

Trust: Another required ingredient for advice is trust in the advice giver. One general framework (and I can’t remember the source) described trust as a simple equation:

Trust = Confidence + Competence

Confidence requires two things. The first is integrity, the perception that the trustee adheres to a set of principles that the trustor finds acceptable. A moral compass, a code of ethics, a set of corporate values, a regulatory requirement—all of these translate into increased integrity.

The second requirement is a belief in benevolence, that the advice giver has your best intentions in mind. This is in the eye of the beholder, a perception that the principles will be upheld and aligned with the interests of the trustor.

Competence, on the other hand, speaks to the expertise of the trustee. What credentials create the perception of competence in the mind of a trustor? In the financial world, a few are often relied upon:

- Professional credentials: CPA, CFA, MBA, CBV, CFP… the list goes on, but these are often displayed prominently by most industry participants to signal competence

- Brands: A brand accrues reputation, both good and bad. It can also accrue signals of competence. Does the company have a strong reputation, does it have high standards, is it well-resourced?

- Referrals and word of mouth: Often, competence is hard to assess on your own, so that assessment is often outsourced to others.

Data: The final ingredient necessary for advice is the requisite data from the two other categories to make a recommendation.

The first set of data is about the needs/wants: does the advice giver have enough data to offer informed guidance? Does the investment advisor have your risk tolerance and risk appetite handy before making an investment decision? Does the mortgage advisor have the appraisal value of your property and your income tax returns for the past several years?

The second set of data is about trust, competence in particular: does the advice giver have enough expertise to make the best recommendation, or do they require more? Does the lawyer have the case law handy to suggest a course of action, or do they need to have an Associate scour their library of resources to look it up?

Data is an often overlooked, but key ingredient to advice. In many cases, and particularly with financial advice, the outputs are only as good as the inputs will allow.

To summarize, tying everything together in a definition:

Advice = needs-based guidance, in all its forms, pertaining to future action(s), backed by the requisite trust and data

That was a general way of saying advice: can be general and/or specific, continuous and/or asynchronous, deep and/or wide; and it requires a need for advice, trust in the advice giver, and data to make recommendations.

Combining the two definitions, we are left with:

Financial Advice = needs-based guidance, pertaining to the facilitation of one’s lifestyle through the financial system, covering the entire surface area of finance, measured by the state of one’s financial health, backed by the requisite trust and data

Goals and Implementation

What is defined above is the broadest definition of financial advice possible. It leaves open all angles and all doors. It also leaves out two topics that most people familiar with financial advice would expect to see, and that’s the role of (A) goal setting and (B) implementation.

The reason both topics have been left until now is because they are more about ‘how’ advice gets delivered, rather than ‘what’ advice is itself. They are the tactics and this piece is about strategy.

That said, goal setting is perhaps the most common (and important) form of financial advice today, particularly after a goal-based advice wave swept the industry over the past few years. It is the primary activity in tying life to finance. The advisor is the technical expert, the client is an expert on their own life, and goal setting is how the two can be brought together. It is clearly a vital and well-employed component of most financial advice today.

Another component that is equally, if not more important, but is far less employed in practice is advice implementation. While a doctor can offer a diagnosis and prescribe a course of action and medication, it is still up to the patient to follow their recommendations, fill their prescriptions and take their meds on time and in the right amounts.

Implementation is tricky since it is typically left up to the client to fulfill. Yet, as was pointed out in the excellent book by Moira Somers, Advice That Sticks, the professional has a role to play in ensuring successful follow-through. Case and point is in the medical industry (as paraphrased by Michael Kitces):

Doctors give advice and recommendations (from new eating habits and exercise regimens, to prescription drugs and physical therapy) but patients don’t necessarily follow through – a phenomenon called non-compliance… And what the medical profession has learned over several decades of research since the phenomenon was first recognized is that a patient’s non-compliance with their doctor’s recommendations can sometimes be as much a problem with the doctor giving the advice than the patient (failing to) take it. In other words, there really is such a thing as “good advice, badly given.”

The skill of the advice giver in actually delivering the advice sets the stage for successful implementation. In addition, with today’s technology landscape, advice givers also have more means to play a direct role. From a higher degree of accessibility through today’s growing digital communication channels to purpose-built software for advice implementation (check out Knudge!), implementation is key to advice efficacy and impact.

Competing on Advice

Wow that was a long path to get here! But with a working definition of advice, we can discuss what it means to truly compete on advice and put it at the center of a financial institution’s strategy.

For big banks and other players in the market showcased as examples at the top of this piece, the crux of the pursuit of the ‘advice strategy’ is to encourage deeper relationships with existing clients and fight off the ills of product commoditization. With little differentiation at the financial product level, the pursuit of differentiation must move to the services level.

What has been done so far in the industry, is mapping existing activities that touch ‘advice’ and calling them out as part of the strategy. What this leaves is partial coverage of the surface area of finance and only touches the financial capital sliver of the personal capital hierarchy.

Competing on advice requires a playbook. According to Richard Rumelt’s book, Good Strategy Bad Strategy, strategy is the art of designing a way to deal with a specific challenge. So, to compete requires first a deliberate identification of the challenge to be overcome. With today’s advice landscape, those challenges are often internally focused: We need to be differentiated and we’ll do so through our services; We need to find growth and deepening relationships with clients can be an expected outcome of providing advice; We need to improve our sales effectiveness; etc.

While these are fine pursuits in the spirit of competition, advice is viewed more as a pawn in the corporate chess game, moving it around the board to temporarily ward off various problems, rather than as a gameplan.

To make a true impact, I’d argue advice strategy design first starts at the client level and works its way outward. This, however, presents a problem!

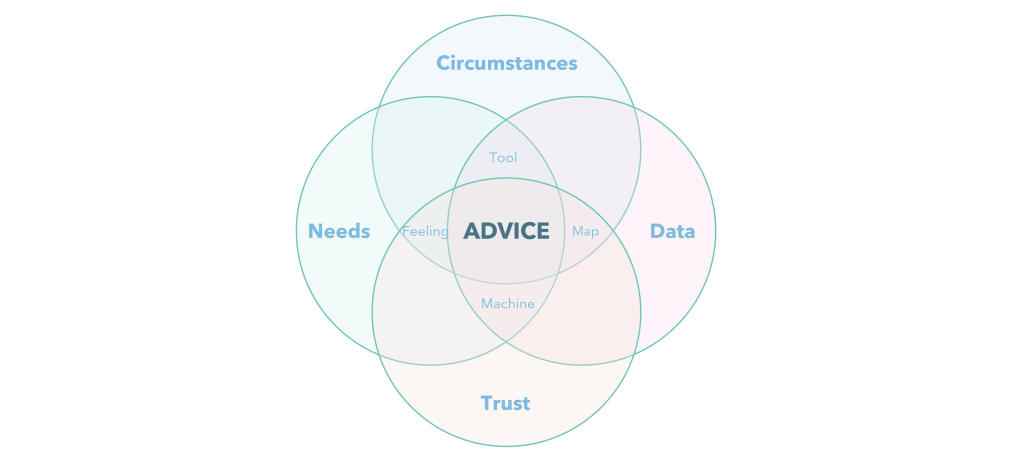

The challenge with clients is that they are each unique. Not only are their personal and financial circumstances unique, but so are their needs for advice, their general degree of trust in advice givers and the available data to inform the advisor. These four areas (circumstances, needs, trust, data) present domains of uniqueness. But where strategy can be built is not on the diversity within, but on the commonality of the categories themselves.

Below is a discussion of the four components that make up the financial advice definition with the objective of providing a framework of ‘how’ to think about each area, rather than a recommendation or specific strategies/tactics. Much of what follows also makes the assumption that to compete on advice, an organization needs to deliver more effective advice or create new value for the client. Without that lens, competing on advice becomes company-centric and counter to the ethos of pursing a strategy that makes the world a better place.

Competing on Surface Area: Advice as a Map

People’s lives are complex, so to is the financial system. Providing a bridge between the two, a map for clients to achieve their objectives, and the means to follow through on implementation are all value-creating activities for people/companies providing financial advice. So, what makes an effective map? First is an understanding of the territory. The advice giver must have adequate knowledge of both the client’s life and the financial system, or at least the particular area they specialize in.

This starts with an effective discovery process. The inputs matter and coaxing them out can be more art than science. In comprehensive financial planning, inputs are both quantitative (account information, tax information, etc.) and qualitative (risk tolerance, goals and objectives, etc.). Building strong information funnels can be a core advantage when aiming to compete on advice.

Quantitative Map Building

The quantitative side of input gathering is typically about building the map of a clients life across the surface area of finance: bank accounts, outstanding debt, creditworthiness, insurance coverage, investment holdings, tax liabilities/assets, real estate values, and so on.

Thanks to technology, a great degree of client information can be made available digitally, instead of just sending over a box of papers and envelopes. That improves efficiency. Beyond that, the progression of open banking and a slow but steady improvement in the rails for permissioned access to client financial information may soon make this even more efficient, and in some cases, real-time. Even today, that is one of the major advantages a large integrated financial institution should have in providing advice: a comprehensive and real-time view of all financial products a client has with that institution and the data exhaust they create. The spend categories in my chequing account say a lot about me, so to does the credit report pulled as part of the way the lending team monitors my account. Gathering, centralizing and making sense of all this information is important and can lead to better advice.

Similarly, as technology continues to progress, one trend that should result in more powerful advice over time is the continuous improvement in financial legibility for other parts of the personal capital stack. Right now, Financial Capital is the primary area of focus for advice because it is the most visible and quantifiable source of information. But progress is being made on unearthing a view in three key areas:

- Real assets: What is the current value of your home? A decade ago, that question would be hard to answer. Today, a quick check on Zillow or HonestDoor (or even better, plugging into their APIs) can surface that information accurately and efficiently. This is increasingly true for other hard asset categories as well, from cars to collectibles.

- Non-traditional financial assets: What is the current value of your private business? The question is very hard to answer without the expertise of an accountant or Chartered Business Valuator (CBV). Similar to real assets, companies like Inter-val are making valuation information available and digestible to those who use their software.

- Human capital assets: What is the value of your earning potential? That is something that has long been quantified as part of insurance needs analysis. It is also becoming more legible through increasingly transparent and available career and salary information from companies like Glassdoor.

As the examples above indicate, there is a trend toward improved financial legibility, a trend that can be leveraged in building more effective maps of a client’s financial life. Making inputs more efficient also makes advice more scalable, potentially extending reach to some clients who may not have had access to quality advice in the past.

Qualitative Map Building

This is where soft skills matter. Qualitative map building is about understanding the client’s life: how they spend their time, what they value most, and what their goals and ambitions are. This domain, to date, is less influenced by technology and is typically best done through a person-to-person interaction. This is true because of several roles the advice giver must play that technology cannot yet replicate:

- Tour Guide: Similar to how a tour guide will help you navigate the streets of a new city and point out relevant and interesting things along the way, a good advisor can help a client navigate the surface area of life, showing them the territory and guiding them to the points that matter most.

- Therapist: To guide effectively, you have to have a good understanding of the client in the first place. While the financial mapping can help put together the financial picture, having a more general conversation about life can be the first step in understanding what matters most to the client: how they spend their time, who are their close family and friends, what do they hope to achieve in life, etc.

- Coach: After guiding and gaining an understanding of internal motivators, the advisor can also play the role of coach, offering up the guardrails, tools and support a client needs across the qualitative map.

Being effective at each of these roles is a very tall task requiring a wide-ranging skillset. While competing on mapping financial inputs was more about technology, competing on mapping life-related inputs is clearly more about people. The ‘soft skills’ required to be an effective map building advisor are often underestimated, but many financial planners I know will tell you the biggest part of their job is in these domains. While the technical training is table stakes, the ability to communicate and interact with people is key to delivering effective and impactful advice.

That said, competing on this front is about people development and organizational structure. Locating people who can act as tour guide, therapist and coach or building these skills in existing staff can create more effective advice delivery. Similarly, given the multiple hats that have to be worn by an advisor, a team-based approach may be more effective where people with specialized skillsets can come together to create a whole that is greater than the sum of its parts.

To summarize, advice as a map involves both quantitative and the qualitative aspects. While doing both well could be a game changer, progress on any of these fronts is an improvement. In the case of map building, referring back to the definitions above, advice is likely to be general, continuous and wide. General because the financial principles applied matter more than specifics, wide because the effective maps cover multiple financial and life-related domains, and continuous because the map of someone’s life and financial circumstances often changes and requires adaptation.

Broad and continuous advice, however, is only one form found in the financial industry today, often in the form of financial planning. But, advice can also be the opposite: deep, specific and asynchronous. This form is also common, advice delivered at a specific time and fulfilling a specific need, in which case, advice is more akin to a tool in a toolkit rather than an ongoing relationship-based endeavour.

Competing on Need: Advice as a Tool

As covered previously, clients have a variety of needs for advice: optimizing outcomes, outsourcing decision-making, optimizing trade-offs, handling or supporting implementation, or catalyzing action. Needs typically arise as a result of two things: events that occur throughout the household lifecycle; and, periodically through clients with preferences for advice-seeking behaviour.

- Events occurring through the household lifecycle: While ‘averages’ are often a poor representation of a diverse reality, I’m going to use the word here: The average person goes through different stages in their life. Often that starts with birth, early development, education, graduation, entering the workforce, entering a relationship, starting a family, getting promoted, accumulating assets, settling down, retiring, and so on. The beginning, end, or occurrence of one of the variety of major life events is often marked by a financial transition as well, one that often surfaces a need for advice.

- Periodic needs from clients with preferences for advice-seeking behaviour: Some people want more experts in their lives. They have a high degree of trust in people, or conversely, a low degree of confidence in themselves. Whatever the case, people who fall on this spectrum will actively seek advice when faced with any type of decision. What supplements should I take? What neighbourhood should I live in? What investments should I choose?

In both of these cases, expertise is relied upon whenever a major decision arises, and advice is drawn out like an arrow from a quiver to help facilitate. Here, advice is like a tool in a toolkit, dormant for long periods and called to action when the time is right.

The common model for administering advice in these circumstances is in a continuous and well-mapped relationship. Expected milestones are often a part of the map and built into goals and objectives to prepare the client ahead of time. The better the mapping, the better the preparation, the higher likelihood of a positive action and outcome. Similarly, unexpected milestones occur frequently as well. But those with the surety of an established advice-relationship know where to turn first.

But financial institutions interact with client life events on a more granular level. For example, millions of people have come through the doors of our largest lenders over the past decades, seeking to take on a major life and financial milestone: purchasing their first home. For most, this is an incredibly complex transaction that has a lot of high stakes decisions, requires the involvement of a number of parties (realtor, banker, lawyer) and also entails a great deal of preparation on the part of the prospective homeowner.

Given that 23% of millennials said that they have or plan to work with a financial advisor (at least, according to Northwestern survey research), there are a great deal of people coming through the lenders’ funnel without access to continuous advice. This is where we introduce the concept of point-of-sale advice, which can be an important differentiator.

Point-of-sale advice, or asynchronous advice delivered as part of an event/transaction-driven experience, is one of the most prevalent forms of advice in the financial industry today. Yet, it is often not touted as such. Every time a new chequing account is opened, loan is adjudicated, or insurance policy is underwritten, an opportunity for advice arises. Sticking with the lending example above, first time home buyers could have improved outcomes through advice that focuses on:

- Product selection and features: fixed or variable rate, open or closed, 2-year or 10-year term, 20-year or 30-year amortization, insured or non-insured, etc.

- Process: who do I talk to next, what paper work do I need to complete, can you recommend a good lawyer, etc.

- Education/information: why do you require my credit score, how does income factor into the amount I’m pre-approved for, how much of my total life savings should I be putting into my initial down payment, etc.

- Mapping: what do all of these variables mean for me and my lifestyle?

This is a lot to take on, but those that are good at providing point-of-sale advice are able to specialize and simplify things to create a positive experience that lead to the right decision for the customer. It is a microcosm of the macro mapping exercise that takes place in a typical financial planning discussion.

Why does specialization matter? Because it helps develop trust (confidence and competence) which is key to advice. Confidence in that I am dealing with someone who has helped thousands of people in my exact situation before rather than the generalist who handles a few of these situations per year. Competence in that the advice giver develops a skillset, network and set of case studies over time that can help guide the client toward the highest probability of a positive outcome.

Point-of-sale advice is everywhere you look. It is deep, specific and asynchronous making it difficult to deliver with consistency. But for those that do it well, millions of positive micro client experiences can add up to something very large for the company delivering them: a positive impact on society, a more competitive value proposition, and most importantly, a sterling reputation.

That reputation goes a long way in competing on trust where advice may be nothing more than the feeling of someone having your back when you need it.

Competing on Trust: Advice as a Feeling

This is a big topic. Advice can be intangible. It can be peace-of-mind that an expert is on standby where you need them and when you need them. But where does that peace of mind come from? In short, it comes from the trust and reputation of individual advice givers, the corporate brands they affiliate with, or both.

- Brand (practices, teams, companies, suppliers, etc.): The brand is the overarching banner under which reputation accrues. This is the sum of a company’s public presence: corporate culture, practiced values, customer experience, product positioning, service standards, talent/staff, etc.

- Individual advice givers (customer service representatives, financial planners, estate planning specialists, etc.): Looking at brand through a fractal lens, the same applies to the individual advice givers employed by the firm: public facing values, expertise, knowledge, personality and character traits all sum to the brand of the individual.

The distinction between these two is often important in financial services contexts because of this question: is your relationship with your financial advisor (Steve) or the company they work for (RBC)? In a traditional financial planning relationship, the answer is that both brands matter.

To look at another case, relationships may be purely with a brand alone: Wealthsimple, for example, although there are people on staff available to speak with clients, most people would say their trust is in the brand rather than those individuals. For purely automated robo-advisors like Wealthfront in the U.S., this is even more true.

A lot of ink has been spilled on how to compete on brand in everything from academia to Twitter and I will not attempt go into that here. Instead, I’ll keep this to two observations:

- Advice can be a feeling. Although it can be hard to attribute economic value to something as intangible as ‘peace-of-mind’, it is something consumers are willing to pay for (ie. See the premium consumer packaged goods brands are able to command over their store brand competitors)

- Although brand is the public presence, the relationship is what drives “advice as a feeling”. The brand is only the first step since there is no context specific to the client. It is the relationship (or the sum of past interactions/experience, brand included) with the client that forms the basis of trust.

Competing on trust means competing on both brand AND experience and aiming both at the objective of building peace-of-mind for the customer. This is a very human form of value delivery, something hard to replicate through technology. But there are specific areas of advice where the opposite is true and are well-suited to a machine-based approach.

Competing on Data: Advice as a Machine

Looking at advice as a machine can be a useful mental model.

A machine can be broken into three functions: it takes in inputs, analyzes or assesses them, and produces a response or output. More simply, this can mean advice can have three machine repeatable functions: data in, data analysis, data out.

There are aspects of all three that humans will be better at, which tend to be focused on qualitative inputs, applying empathy, and delivering personalized and context-informed solutions. There are also aspects of all three where technology might have a leg-up: sourcing quantitative inputs, applying logic, and delivering rules-based outcomes (see below).

*There is also arguably a fourth task in ‘implementation’ or ensuring advice follow-through. This is left to the side for this discussion since it is more about the practical application of advice, rather than its production and delivery. That said, it is incredibly impactful on client outcomes and has lacked focus in the financial services industry to-date. For more information, I’d again suggest reading Moira Somer’s work in Advice That Sticks.

Of course, in many ways, humans can do what machines do and vice versa, but it when their strengths are combined is when something powerful can be created.

Some have argued that technology-driven advice can/will outcompete traditional human-based forms of advice: self-driving money, robo-advice, and self-serve financial planning tools are all examples. But, is a pure technology-first approach ready for ‘financial advice’ primetime? Based on the success [measured by their share of market] of examples in the market to date, the answer would be no. Similarly, on the other side, traditional financial advisors relying on no technology or software in their practice today are also likely being left behind.

The sweet spot is right in between: identifying areas and situations where a human, a machine or a human + machine approach is best suited to perform across the three primary advice activities.

Wrapping up

Unfortunately, if you have made it to this point hoping for answers, you are likely disappointed. I don’t bring answers, I only bring frameworks. If advice is going to be the differentiator at the center of many strategic plans in the financial services industry, then we deserve some definition about what that will mean. To compete on advice means to compete on surface area, needs, trust and data. And as it usually does, my hope is that competition will inspire progress and creativity on all four fronts, each of which could ultimately lead to better outcomes for the clients the industry serves.

4 responses to “Competing on Advice: A Framework for Looking at the Strategy at the Center of Financial Services”

[…] As mentioned before, financial advice is a difficult service to make tangible to the consumer. It is hard to define, and therefore, hard to put a price on. So for financial advisors to standout, they typically have […]

LikeLike

[…] Advice: Funny enough, another topic that I’ve written about at length here, is also a strategy that involves heavy use of context. Companies that are differentiating through […]

LikeLike

[…] values that are subject to change). A good framework to use is the personal capital hierarchy from Competing on Advice: A Framework for Looking at the Strategy at the Center of Financial Service… (see […]

LikeLike

[…] Competing On Advice: A Framework For Looking At The Strategy At The Centre Of Financial Services […]

LikeLike