A product or service is simply an aggregation of its various features.

Features can be ‘stackable’, where each layer of the stack adds to the overall value of the product.

A checking account is great on its own. Adding free transactions makes it even better. Adding a personal financial management tool improves it even more. Each layer of the stack adds to the overall value of the product.

Features can also be ‘compounding’, where the combination of features creates new forms of value for the customer.

A credit card is a good product on its own. So is a rewards platform. The two are made even better when they are brought together in a way that makes the whole greater than the sum of its parts. In this case, by offering bulk airline and purchase discounts to credit card customers that are only made possible by the scale those customers bring.

Features can also be ‘subtractive’, where the addition of more features takes away from the overall product experience.

Instagram was once a great photo editing and sharing app, but the addition of Stories, Reels, Commerce, and Chat has turned it into an everything app that has become less useful for its original function.

Features can also be a ‘multiply by zero’.

The Zero Property of Multiplication states that any number multiplied by zero will be zero.

For products, this means the addition of (or lack of) a specific feature will remove a product entirely from a customer’s consideration set.

- For health-conscious consumers, the use of sugar or specific artificial sweeteners may be a multiply by zero, where a customer will not even consider sugar-sweetened soft drinks as part of their beverage consideration set.

- For travelers in foreign countries, the lack of an in-car navigation system in a rental car may be a multiply by zero where customers will not accept a vehicle that cannot tell them where to go.

- For young banking clients, a lack of peer-to-peer transfer options (or even the presence of a fee for accessing those options) may be a multiply by zero since it can act as a barrier to one of the customer’s most frequent uses of the product.

- For ALL banking clients, trust is a multiply by zero.

Banking is a simple business:

- Protect and move money, a service which has a cost to operate. Yet, most depositors don’t pay for these services (and actually get paid in the form of interest).

- Perform maturity transformation, borrowing short to lend long, which also bears a cost in the form of risk. Taking deposits and turning them into loans (mortgages, car loans, credit cards, etc.) is a valuable function in the economy. Without the provision of credit, our world would be a much different place.

As a result of these functions, banks operate on confidence, and whether explicitly stated or not, trust is a feature built into every banking product.

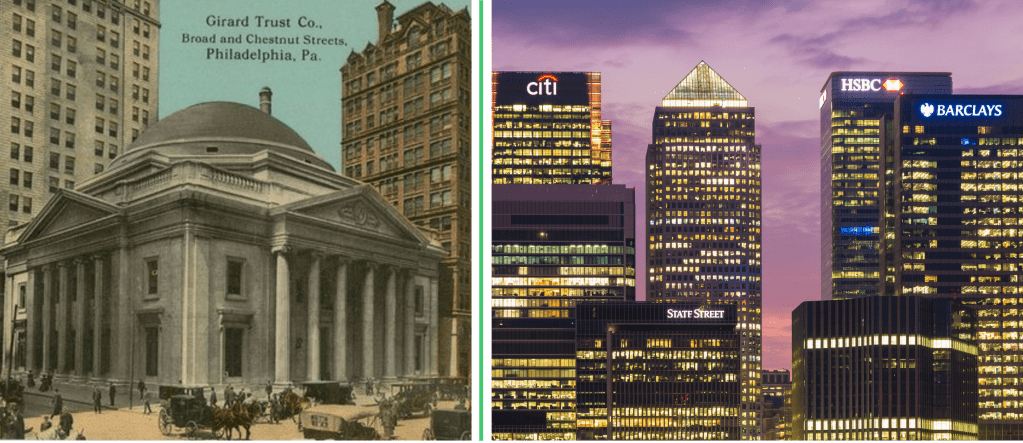

This was more recognizable in pre-modern banking, where local financial institutions would spend gratuitously on the construction of fortress-like bank branches to signal their safety and security [and in modern times, is likely why bank logos dot the skylines on top of office towers of all major urban centers]. A bank that invests so heavily in its physical presence likely is not going anywhere anytime soon.

We also saw trust elevated in financial services marketing and messaging coming out of the 2008 financial crisis. With the collapse of Bear Stearns and Lehman Brothers, bank failures mentally shifted in the public mind from ‘not in our lifetime’ to ‘omg, this a real-world possibility’. Frozen credit markets and government bailouts only added to the fear, which slowly subsided as equity markets recovered, new regulations were installed, and importantly, no more banks failed.

That is, until last week. Silvergate. Silicon Valley Bank. Signature. If your financial institution begins with the letter ‘S’, watch out! Of course, having an ‘s’ in the name is not a ‘multiply by zero’, but losing the trust of your customers certainly is.

There has been a lot of ink spilled already about the panic that set in on Thursday after news of SVB’s $500M equity raise caused their depositors to flee. I’d recommend Marc Rubenstein’s coverage here, Alex Johnson’s thoughts here, or anything that Matt Levine writes on the topic.

What becomes evident in all the analysis is that despite all of the potential causes for liquidity issues at a financial institution (eg. serving crypto companies that have fallen on hard times, taking too much duration risk on the asset side of the balance sheet, shoddy ALM or risk management practices, etc.), there is only one ingredient necessary to cause a bank run: People.

…and when people lose their confidence in an organization, trust collapses. It is the ultimate ‘multiply by zero’ feature in the banking industry. Without it, customers (prospective or existing) will remove the bank from their consideration set.

Yet, trust often does not stand on its own as a useful feature.

If you ask a depositor ‘what job are you hiring this banking product to do‘, you’ll likely get an answer back that relates to their life, business or finances, not the feeling of safety and security.

But after this week, perhaps this will change.

Safety and security will likely be elevated in bank branding and messaging in the near future and people may even be willing to pay a premium to hold their dollars in an institution that instills confidence. Of course, this stands to benefit banks that already have longstanding trust built into their brands either because they are ‘too big to fail’ or because of their established size, scale and market presence (which is an unfortunate outcome for start-ups and smaller institutions looking to do right by their customers).

Like the economy, credit and liquidity conditions tend to move in cycles. Unfortunately, we’re currently venturing into unknown territory thanks to the hockey stick shape in the graph below.

But if anything, the past week has been a reminder that ‘trust’ is one of the most important features that banks offer their clientele.

Without it, the product is zero.