At the top of the funnel in traditional consumer businesses, marketers need to hunt for attention in the right places. Digital, social, print, tv, etc. Among all of the various traction channels, the goal is to find underpriced attention in the right place order to get your product/brand/message in front of the target customer.

In the financial services business, finding attention in the right place is not sufficient for success. Instead marketers need to hunt for attention in the right place AND under the right context.

Apathy-driven Shopping: Why Context Matters

In the retail commerce world where companies like Nike and Lululemon thrive, there are two primary types of shopping: search-driven shopping and discovery-driven shopping.

- Search-driven shopping is the grocery store. It’s going to a shopping location with purchase intent and a specific need in mind, looking for the right product to fill it. Search-driven shopping is about fulfillment.

- Discovery-driven shopping is the mall. It’s wandering around, browsing, deciding what you might want to buy. Discovery-driven shopping is about serendipity.

But these two categories do not fully cover the bases in financial services. Many financial services are difficult to evaluate by ‘browsing’ (ie. it is hard to do ‘search-driven’ shopping for a financial advisor) and there likely is not much ‘discovery’ happening when it comes to commoditized financial products like unsecured loans or savings accounts.

Financial services requires its own third category: Apathy-driven shopping.

- Apathy-driven shopping is the bank. It’s there if you need it, but it often sits in the background until that need becomes urgent. Apathy-driven shopping is about attention.

Apathy Means Capturing Attention for Customer Acquisition is Not Easy!

Attention has been described as the allocation of limited cognitive processing resources—and people sure don’t like to think about their finances!

This third type of shopping is what makes customer acquisition in the financial services arena unique. People are generally apathetic toward their financial providers until some internal or external shock focuses their attention on the topic:

- People do not tend to proactively call their financial advisors, at least, until the markets are down.

- People do not tend to seek out life insurance, at least, until their first child is born and they have a family that needs protecting.

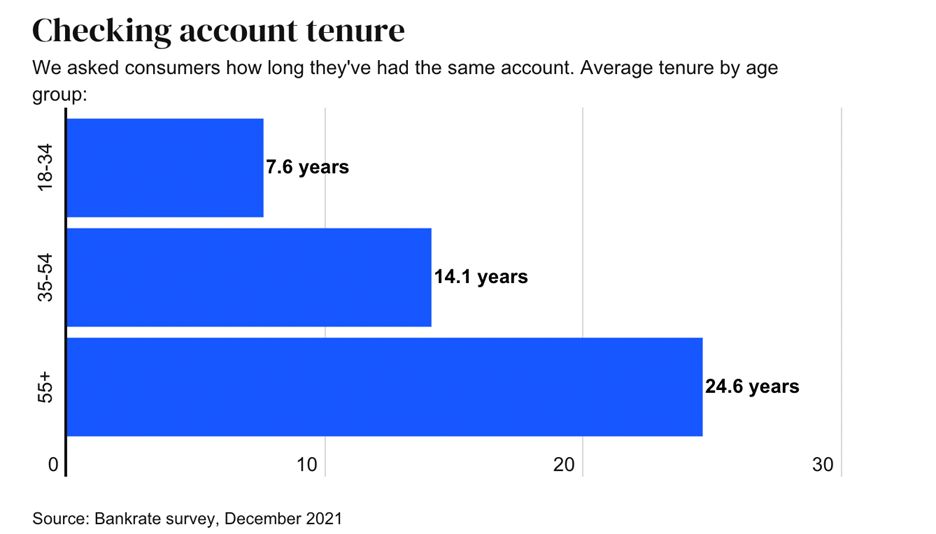

- People do not seek out new chequing accounts… in general. See the chart below:

Perhaps payroll API companies like Pinwheel will change this dynamic one day by lowering the switching cost hurdles for banking clients… but that is a topic for another post.

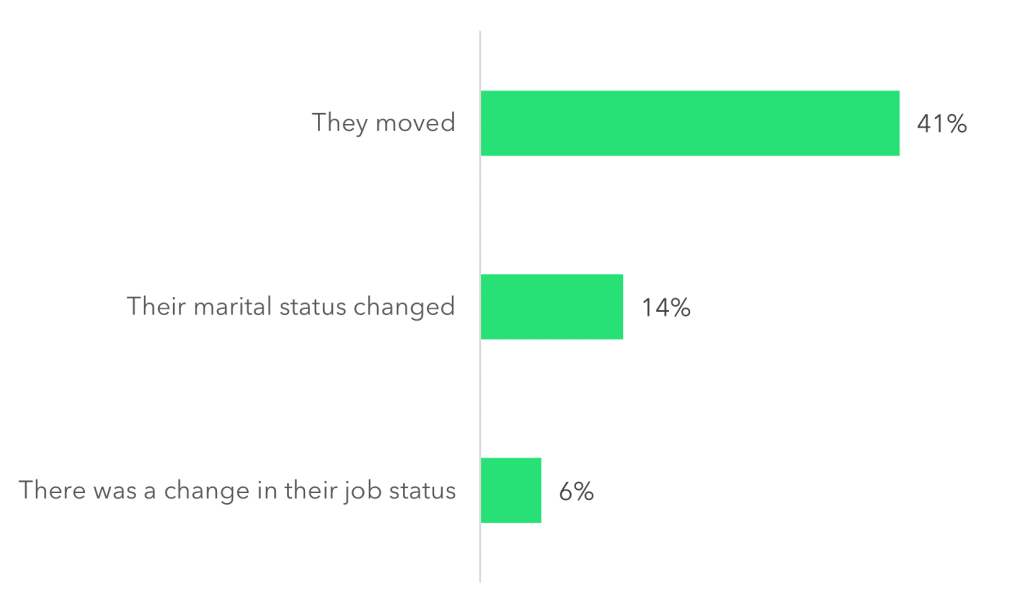

Why do people switch banks? Here are the top three reasons from a Bank Clarity survey:

They all relate to life events. Ranking sixth on this list, only 3.5% said they were attracted to their new bank’s products. Yikes! That means pushing products on prospects and customers is an unlikely path to success (even with free toasters, or today’s modern versions of a new iPad or $400 cash).

Funny enough, checking accounts have it relatively easy compared to financial advice and investment management.

People break up with their banks on occasion, which is a relationship they have with a brand. People break up with their financial advisors rarely, which is a relationship they have with a person. It takes a lot to win new dollars as a financial advisor, particularly with average client relationships lasting decades.

The Correct Context

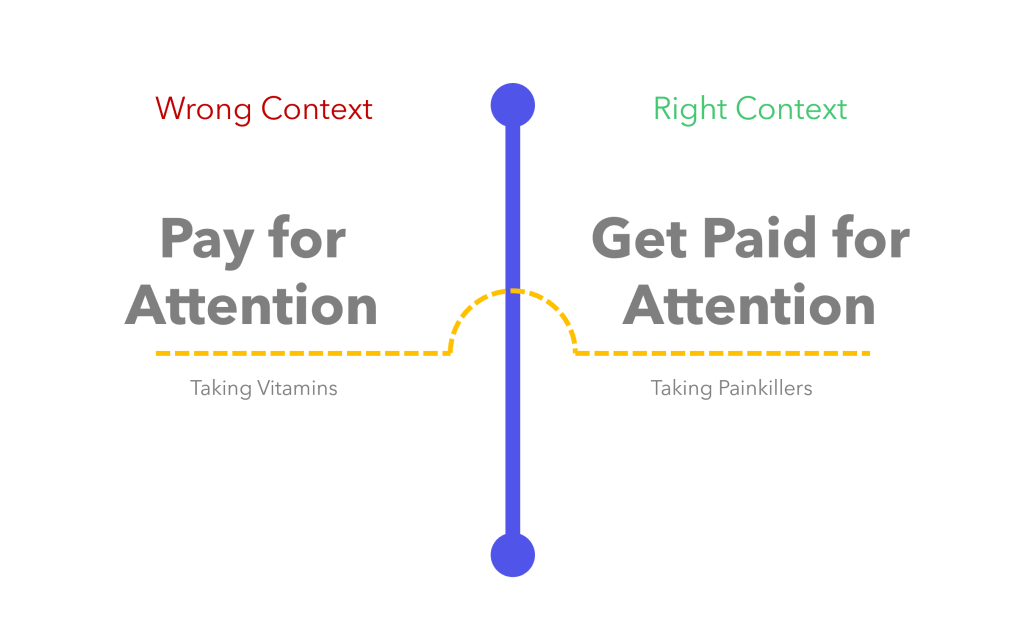

When it comes to apathy-driven shopping, attention is a prerequisite before making a sale. If a customer isn’t searching for the service, or browsing for discovery, then the context must be right in order for a consumer to consider a relationship with a new financial brand.

When the context is wrong (ie. when a prospect’s attention is not already on their finances), brands have to pay for attention through traditional advertising.

When the context is right (ie. when a prospect’s attention is squarely on their finances), customers tend to have the activation energy required to seek out new brands (or at least be more receptive to their messaging).

That means financial services marketers must be good at hunting for attention.

The question is: where to hunt?

Finding Pools of Attention

Attention tends to cluster around specific topics.

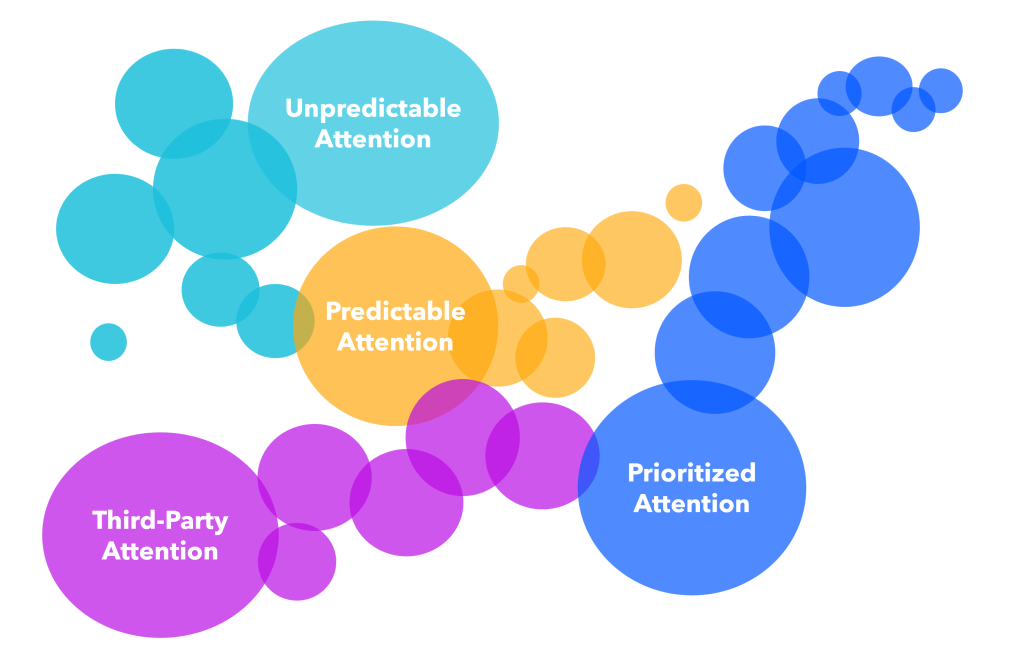

There are four primary pools in which context makes consumers more open to new financial relationships:

Unpredictable Attention Pools: Arise when the right context is created by random and/or unexpected events. These can be both intrinsic and extrinsic.

- Extrinsic: Macroenvironmental changes like equity markets crashing, inflation rates rising, or a global pandemic create headlines and financial challenges that bring personal financial topics into the spotlight. When markets are down, consumers are much more likely to be receptive to messaging from new financial advisors. When a global pandemic sets in, people are much more likely to have time on their hands to do some self-directed investing. When both events occur at the same time, opportunity abounds for those that can react fast enough to take advantage.

- Intrinsic: Sudden life changes like a death in the family or an unexpected job opportunity can create situations where income and/or assets may be on the move.

Customer acquisition activities around these pools must be reactive and take advantage of fleeting situations.

Predictable Attention Pools: Arise when the right context is created by events or developments that can be known ahead of time. These attention pools can also be both intrinsic and extrinsic.

- Extrinsic: These are commonly observed economic patterns. The annual RRSP contribution deadline is perhaps the most ‘well-known’ of these cycles, at least in Canada. Every February, the entire financial industry prepares for ‘RRSP Season’ when consumers know it is their last chance to contribute dollars to their registered retirement accounts in order to reduce their tax liability from the previous year. The economic and business cycle also produce a variety of predictable extrinsic examples.

- Intrinsic: These are commonly observed life patterns. The household lifecycle is likely the most commonly cited taxonomy, where the predictable events occur through the typical stages of life: dependent child, independent adult, married adult, family formation, retirement, etc. Each of these life stages have a variety of financial changes/challenges that need to be addressed and create the perfect context for consumers to focus on their financial situation.

Customer acquisition activities around these pools must be proactive, with resources planned well in advance to target prospects when the time comes.

Third-Party Attention Pools: These pools form around other companies and can be strategically siphoned by financial marketers.

- Partnering: Strategic alliances and partnerships offer a path through which one company can borrow the ‘attention’ of another in order for them both to benefit. For example, during tax filing season, consumer attention flocks to online tax filing platforms like TurboTax. That’s one of the primary motives for a recent partnership between Neo Financial and Intuit who are introducing TurboTax Cash: TurboTax Cash provides filers with the opportunity to get up to 80% of their refund amount (to a maximum of $1,000) in minutes. Filers open a Neo MoneyTM account with a Neo MoneyTM card to get a no-cost loan deposited into their account with no impact to their credit score. Neo taps into the place where attention is, in the tax return process, to solve a problem for consumers while starting new relationships and capturing new dollars.

- M&A: Beyond partnerships, some companies are willing to acquire others simply for the ‘attention’ advantage they can provide. For example, in 2019, Morgan Stanley acquired equity administration platform Solium Financial. At the time, Solium had over 3,000 stock plan clients (like Stripe, Instacart and Shopify). When one of those companies experiences a liquidity event (ie. an IPO), hundreds of millionaires are minted overnight, creating a pipeline of new wealth management clients for Morgan Stanley brokers to introduce themselves to.

- Affiliates: Third-party attention pools are also commonly tapped into through affiliate marketing. From platforms like Credit Karma and Finder to social media influencers, affiliate marketing provides a rich source of potential attention to redirect.

Prioritized Attention Pools: These are attention pools that are ‘higher priority’ than those that surround an existing product/service. Two categories include:

- Temporal Arbitrage: tapping into short-term products for long-term gain. For example, Investment funds are oriented toward the long-term. They are purchased and put away, hopefully not to be thought about by the investor until they need to be drawn upon. They have very few brand touches along the way. On the other hand, payment cards are oriented toward the short-term. They are in the customer’s hand each time a purchase is made. They have hundreds of brand touches with the customer every year. By launching a payment card, much like Acorns, Robinhood and Stash did while scaling their investment offerings, companies are able to perform temporal arbitrage, translating business from their short-term attention products into those with long-term orientations.

- Cultural Arbitrage: tapping into ‘topical’ and ‘trendy’ products. This strategy involves parlaying attention and customer relationships from ‘hot’ products into other ‘less sexy’ products. Any established consumer fintech company that entered the crypto arena over the past several years was following this path. Revolut, which recently reported their first ever annual profit, introduced the idea of crypto trading to their user base in the height of the 2017 crypto boom and quickly garnered over a million sign-ups. The addition of the ‘trendy’ product of the day helped Revolut from a positioning perspective, but also likely brought a variety of new users to the company that they could then cross-sell their prepaid MasterCard and other services.

Urgency and Activation Energy

Armed with a variety of attention pools to explore, financial marketers are then tasked with creating the urgency and activation energy required to get a new customer onboard.

This is also harder than it seems. Creating desire in commoditized markets where existing products are ‘good enough’ is a tall task (ie. Bank A’s line of credit looks and feels the same as Bank B’s and Bank C’s). Product teams can support this task by developing differentiated features. But for companies that fall into the ‘commoditized’ bucket, the customer acquisition burden tends to fall on the marketing department.

When dealing in commodities, marketing’s primary job is not to position the product correctly, or even get messaging right. It is to create the urgency needed to get the customer started. Messaging should not be ‘why this Product’, but rather ‘why this Product NOW?’. Incentives should not necessarily involve dangling a big carrot (since this tends to attract incentive-chaser and rate-shopper client profiles). Urgency, instead, should come from having the right CONTEXT in place from one of the previously mentioned attention pools. What happens if you don’t act today? What happens if you don’t start building your credit score or saving for retirement? What happens if you don’t open an RRSP for your child? What stress or pain can be relieved by making a switch?

By getting the context right, instead of marketing a vitamin, we can market a painkiller.

Attention Seekers

At the end of the day, financial marketers can make their practice more effective by becoming good attention seekers.

In a traditional sense, this means being good at finding the right traction channels that align to the target customer base.

In a less traditional sense, this means understanding how the attention of prospective customers ebbs-and-flows and pools into different places.

Knowing where to look for attention can lead to new strategic opportunities and help combat the challenges that apathy-driven shopping brings to the industry.

Since the world continues to evolve, customer acquisition tactics must also evolve to keep pace, and paying attention to attention should be a continuous step along that path.